CME Plans Bitcoin Volatility Futures Launch on June 1

CME Group plans to launch Bitcoin Volatility Futures contracts on June 1, giving traders a new way to take positions on the size of Bitcoin’s price swings rather than the direction of the market itself.

What CME Plans to Launch on June 1

The derivatives exchange announced the planned launch of a new futures product built around Bitcoin volatility. The contracts are scheduled to begin trading on June 1, pending regulatory review.

Unlike standard Bitcoin futures, which rise or fall with the price of BTC, volatility futures are designed to reflect expectations about how much Bitcoin’s price will move over a given period. Traders holding these contracts profit from large swings in either direction, not from picking tops or bottoms.

The product sits alongside CME’s existing suite of Bitcoin derivatives, which already includes standard futures and options. Adding a volatility-specific contract fills a gap that has existed in the regulated crypto derivatives market for years.

Why a Volatility Product Matters for Bitcoin Markets

Volatility exposure serves a different purpose than directional trading. Institutions that hold large Bitcoin positions often need tools to hedge against sudden market swings, and a regulated volatility futures contract on CME provides exactly that.

For market makers and options desks, the product could simplify the process of pricing and managing risk. Currently, traders who want pure volatility exposure in Bitcoin typically construct it synthetically through options strategies, which can be costly and complex. A dedicated futures contract streamlines that process.

The Bitcoin Volatility Futures product page positions the contracts within the same infrastructure that institutional participants already use for equity and commodity volatility products. That familiarity could lower the barrier for traditional finance firms to participate in crypto volatility markets.

The launch comes as Bitcoin on-chain activity has recently hit multi-year lows, even as BTC has reclaimed price levels that attracted attention from institutional allocators. A volatility product may appeal to firms that want exposure to Bitcoin’s market dynamics without committing to a directional bet.

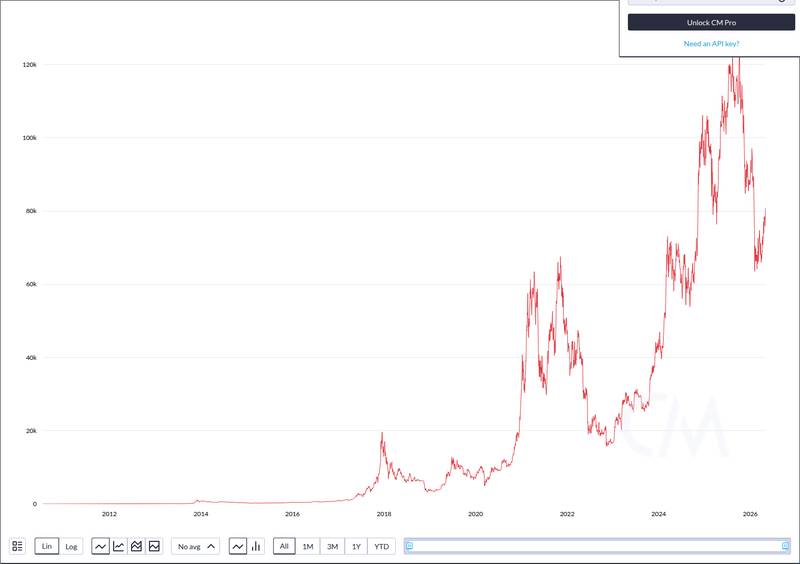

CoinMetrics blockchain-data panel highlighting the structural trend discussed for bitcoin.

CoinMetrics blockchain-data panel highlighting the structural trend discussed for bitcoin.

What to Watch After the Launch

The first days and weeks after June 1 will reveal whether the product attracts meaningful liquidity. New futures contracts often see thin order books at launch, and early participation from market makers will shape how useful the product becomes for hedging and speculation.

Open interest growth will be one of the clearest signals. If institutional desks begin building positions quickly, it would suggest that demand for regulated Bitcoin volatility exposure was already latent in the market. Slow uptake might indicate that existing synthetic strategies remain sufficient for most participants.

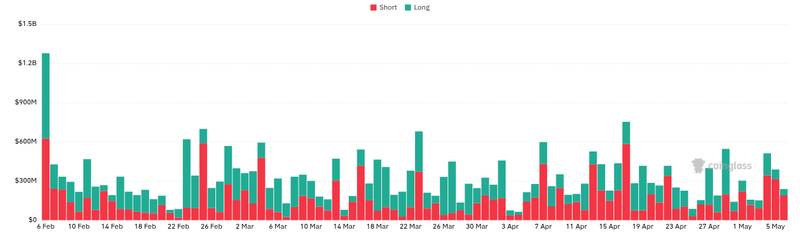

CoinGlass market-structure view used for the leverage and volatility section on bitcoin.

CoinGlass market-structure view used for the leverage and volatility section on bitcoin.

Pricing dynamics in the early sessions will also matter. How the volatility futures price compares to implied volatility derived from CME’s Bitcoin options market will show whether the new product is finding its own equilibrium or simply tracking existing instruments.

Large Bitcoin holders, including firms that have recently sold BTC under financial pressure, may find a volatility product useful for managing risk on remaining positions without liquidating further. The broader regulatory scrutiny facing digital asset promotions has also increased institutional appetite for transparent, exchange-traded products over less regulated alternatives.

Disclaimer: This article is for informational purposes only and does not constitute financial or investment advice. Cryptocurrency and digital asset markets carry significant risk. Always do your own research before making decisions.

You May Also Like

Bitcoin Exchange Binance Announces New Listings on its Futures Platform! Here Are the Details

Flex Stock Surges 35% After Earnings Beat and Cloud Spin-Off Plan