Both are stablecoins de-anchored, why did USDe survive while LUNA went to zero?

Author: MSX Research Institute

The intersection of the October 2025 unmooring event and Hayek's predictions

On October 11, 2025, panic in the crypto market caused an extreme shock to the synthetic stablecoin USDe. Amidst Bitcoin's epic crash, which saw it plummet from $117,000 to $105,900 (a 13.2% drop in a single day) and Ethereum's 16% drop in a single day, USDe briefly dipped to approximately $0.65 (a 34% drop from $1) during trading on October 11, 2025, before recovering within hours. During the same period, global crypto market liquidations soared to $19.358 billion over a 24-hour period, forcing 1.66 million traders to close their positions, setting a record for the largest single-day liquidation in history.

From the perspective of micro-market performance, the depth of the USDe-USDT liquidity pool on the decentralized exchange Uniswap was only US$3.2 million at the peak of the incident, a decrease of 89% from before the incident. As a result, a sell order of 100,000 USDe suffered a 25% discount due to slippage (the pending order was US$0.7, and the actual transaction price was US$0.62). At the same time, the six leading market makers faced the risk of liquidation due to a 40% reduction in margin value due to the use of USDe as cross-margin, further exacerbating the market liquidity black hole.

However, this "crisis" saw a key reversal within 24 hours: the price of USDe gradually rebounded to $0.98, and the third-party reserve certificate disclosed by Ethena Labs showed that its collateral ratio remained above 120%, with over-collateralization reaching $66 million; more importantly, the user redemption function was always normal, and assets such as ETH and BTC in the collateral could be cashed at any time. This feature became the core support for the restoration of market confidence.

The Maitong MSX Research Institute believes that this "plunge-recovery" curve is in sharp contrast to the ending of LUNA-UST returning to zero after decoupling in 2022, and also makes this event go beyond the scope of ordinary "stablecoin fluctuations" - it has become the first extreme stress test of Hayek's "Denationalization of Money" theory in the digital age.

In 1976, Hayek argued in "The Denationalization of Money" that "money, like other commodities, is best provided by private issuers through competition, rather than by a government monopoly." He believed that government monopoly over currency issuance "is the root of all the ills of the monetary system," and that the greatest problem with the monopoly mechanism is that it hinders the process of discovering a superior form of money. Under his envisioned competitive framework, privately issued currencies must maintain stable purchasing power, otherwise they will be eliminated from the market due to a loss of public trust; therefore, competitive currency issuers "have a strong incentive to limit their quantity or lose business."

Half a century later, the emergence of the USDe embodies the contemporary expression of this philosophy. It relies not on sovereign fiat currency reserves but on crypto-market consensus assets for its value, maintaining stability through derivatives hedging. Its credibility and circulation are entirely dependent on market selection and technical transparency. Regardless of the outcome of the unpegging and recovery in October 2025, the implementation of this mechanism can be seen as a real-world experiment in Hayek's "competition to discover the superior currency"—it not only validates the potential self-regulating power of the market in monetary stability, but also reveals the institutional resilience and evolutionary direction of digital private currencies in complex environments.

USDe's mechanism innovation

USDe's "collateral-hedge-return" trinity structure is permeated with the logic of market self-regulation in each link, rather than the mandatory constraints of centralized design. This is highly consistent with Hayek's emphasis on "market order stems from individual spontaneous action."

Collateral system: the value foundation for building market consensus

USDe's collateral selection fully adheres to the consensus of crypto market liquidity. ETH and BTC together account for over 60% of the total. These two assets are not designated by any institution, but have been recognized by global investors as "hard assets of the digital world" through over a decade of trading. Supporting liquidity staking derivatives (such as WBETH and BNSOL) are also products of the market's spontaneous emergence to improve capital efficiency, preserving staking returns without sacrificing liquidity. USDT/USDC, which accounts for 10% of the total collateral, is a market-selected "transitional stabilization tool," providing a buffer for USDe during extreme market conditions.

The entire mortgage system always maintains an excess state. When the incident occurred in October 2025, the mortgage ratio was still over 120%, and it was valued and automatically liquidated in real time by smart contracts.

Stabilization Mechanism: Spontaneous Hedging in the Derivatives Market

The core difference between USDe and traditional fiat-collateralized stablecoins is that it doesn't rely on fiat reserves backed by national credit, but instead hedges risk through short positions in the derivatives market. This design leverages the liquidity of the global crypto derivatives market, allowing the market to absorb price fluctuations. When the price of ETH rises, profits from spot assets offset losses from short positions; when the price of ETH falls, profits from short positions offset losses from spot assets. This entire process is driven entirely by market price signals, without the intervention of any centralized institution.

When ETH plummeted 16% in October 2025, this hedging mechanism experienced a brief lag due to the sudden depletion of liquidity, but it did not fail - the short position held by Ethena Labs eventually generated $120 million in unrealized profits. These profits did not come from administrative subsidies, but from voluntary transactions between long and short parties in the derivatives market.

Revenue Mechanism: Spontaneous Incentives to Attract Market Participation

USDe's "staking income + revolving lending" model is not the "rigid redemption with high interest" of traditional finance, but rather a reasonable compensation for the risks borne by market participants. The basic 12% annualized subsidy comes from the ecosystem's voluntary investment in increasing the circulation of currency. The mechanism, which increases leverage to 3-6x through revolving lending and yields annualized returns of 40%-50%, essentially allows users to choose their own risk-reward balance. Those willing to bear higher leverage risks will receive higher returns, while those with a lower risk appetite can opt for basic staking.

Comparison of three types of stablecoin mechanisms: the distinction between market choice and administrative intervention

The truth of the market test: Why USDe can draw a clear line between itself and LUNA-UST

The unpegging event in October 2025 is often misunderstood as the "similar risk exposure" of USDe and LUNA-UST, but from the perspective of the Austrian School, the essential differences between the two were fully highlighted in this test - USDe's recovery was the success of "non-nationalized currency withstanding the market test", while the collapse of LUNA-UST was the inevitable outcome of "pseudo-innovation that is divorced from real assets."

The essential difference in value anchors: real assets vs. false expectations

USDe's value anchor is real assets such as ETH and BTC that can be redeemed at any time. Even in extreme market conditions, users can still obtain equivalent crypto assets through the redemption mechanism. During the depegging period in October 2025, USDe's redemption function always operated normally, and third-party reserve certificates showed that the over-collateralization reached 66 million US dollars. This "redeemable value commitment" is the foundation of market confidence.

LUNA-UST, however, lacks any real asset backing; its value depends entirely on user expectations of LUNA's price. When market panic erupts, UST's redemption mechanism must be met through the issuance of additional LUNA. However, this unlimited issuance of LUNA ultimately loses its value, leading to the collapse of the entire system. This "asset-free currency" violates Hayek's principle from the outset that "money must have a real value basis," and its collapse is inevitable.

Logical differences in crisis response: spontaneous market recovery vs. ineffective administrative intervention

USDe's response after depegging completely complies with market logic: Ethena Labs did not issue an "administrative order-style rescue plan", but instead sent a signal of "transparent mechanism and safe assets" to the market through public reserve proof, optimized collateral structure (reducing the proportion of liquidity pledged derivatives from 25% to 15%), and limited leverage multiples, ultimately relying on users' spontaneous trust to achieve price repair.

LUNA-UST's response to the crisis was a typical example of "administrative intervention failure": Luna Foundation Guard attempted to save the market by selling off its Bitcoin reserves, but this centralized operation was unable to counter the market's spontaneous sell-off - Bitcoin itself also fell in extreme market conditions, and the reserve assets were highly correlated with UST risks, and ultimately the rescue failed.

Differences in long-term vitality: market adaptability vs. institutional fragility

After de-anchoring, USDe not only restored its price, but also improved its long-term adaptability through mechanism optimization: limiting the leverage of circular lending to 2 times, introducing compliant treasury bond assets (USDtb) to enhance collateral stability, and dispersing hedging positions across exchanges - these adjustments did not come from administrative orders, but were spontaneous responses to market feedback, making the mechanism more in line with the market law of "risk and return matching."

LUNA-UST lacked market adaptability from the outset: its core Anchor protocol, offering a high 20% interest rate, relied on continuous subsidies from ecosystem funds, rather than actual payment needs (actual payment scenarios for UST account for less than 5%). When subsidies became unsustainable, the funding chain ruptured, and the entire system collapsed instantly. This model, relying on unsustainable administrative subsidies, was doomed to fail in the long term in the competitive market.

Mechanism Flaws and Critical Reflection: The Growth Dilemma of Non-nationalized Currency

The innovative value of USDe is undeniable, but during the stress test in October 2025 and its daily operation, its mechanism design still deviated from Hayek's concept of "complete market self-regulation", exposing potential risks that need to be vigilant. These flaws are not inherent defects that cannot be corrected, but are obstacles that must be overcome in its evolution towards a mature non-nationalized currency.

Collateral Concentration Risk: Systemic Binding of Cryptoasset Cycles

Over 60% of USDe's collateral is concentrated in ETH and BTC. While this aligns with the current consensus on crypto market liquidity, it suffers from the dilemma of being "bound to a single market cycle." The October 2025 depegging was essentially a chain reaction triggered by a unilateral decline in the crypto market. When ETH plummeted 16% in a single day, the instantaneous decline in the collateral's market value still triggered market panic, even with derivatives hedging.

Of even greater concern is the fact that current liquidity-collateralized derivatives (such as WBETH) remain embedded within the Ethereum ecosystem. Essentially, they are "secondary derivatives of crypto assets," failing to achieve true risk diversification. This "internal circulation of crypto assets" collateral structure remains fragile compared to the logic of traditional currencies, which rely on the value of the real economy.

Limitations of Hedging Mechanisms: Implicit Dependence on Centralized Exchanges

USDe's derivatives hedging is highly dependent on the liquidity of leading centralized exchanges. The brief delay in the hedging mechanism in October 2025 was due to a liquidity gap caused by the suspension of perpetual swap trading on a leading exchange. Currently, approximately 70% of USDe's short positions are concentrated on just two exchanges, making it difficult for it to completely break free from its passive acceptance of centralized platform rules.

Furthermore, the dramatic fluctuations in funding rates expose the limited nature of hedging tools. USDe currently relies solely on perpetual swaps for risk hedging, lacking a portfolio of diverse instruments like options and futures. This makes it difficult to quickly adjust hedging strategies when there is an extreme imbalance between long and short positions. This demonstrates that its mechanism design still fails to fully leverage the market's ability to price diverse risks.

RWA anchor upgrade: the advanced path of non-nationalized currency

In light of the flaws in the existing mechanism, integrating RWA assets like gold tokens and US stock tokens to optimize the anchoring system is not only a precise correction to USDe's shortcomings, but also an inevitable choice in line with the explosive growth trend of the RWA market (expected to reach $26.4 billion in 2025, a year-on-year increase of 113%). This upgrade does not deviate from the core principle of denationalization, but rather, by connecting with the value of the real economy, it makes Hayek's ideas more resilient in the digital age.

The underlying logic of RWA anchoring

Currency value should be derived from real assets with broad market consensus. RWA assets possess this property. Gold, as a millennial hard currency, has a value consensus that transcends countries and eras. US stock tokens correspond to the real economic returns of listed companies, anchored by the company's ability to create value. Treasury bond tokens rely on the tax revenue capacity of sovereign states, providing a low-volatility value benchmark. The value of these assets is not dependent on crypto market cycles, but rather on real-world production and transactions, providing a "cross-market value cushion" for the US De.

The BUIDL token (anchored to assets such as U.S. Treasury bonds) launched by BlackRock in 2024 has verified the feasibility of RWA anchoring. Its core difference from USDe is that BUIDL relies on centralized institutions for issuance, while USDe can achieve decentralized ownership and valuation of RWA assets through smart contracts, truly practicing the logic of "market spontaneous management."

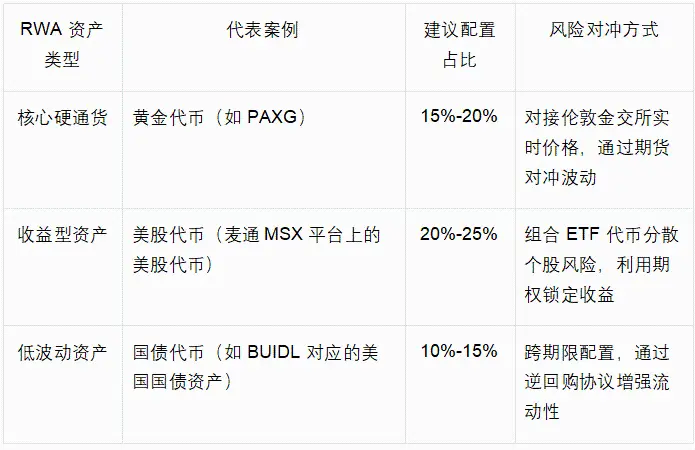

Adaptation and allocation strategy for diversified RWA assets

USDe's RWA anchor upgrade should follow the principle of "market consensus first, risk diversification and adaptation". Combined with the current maturity of RWA tokenization, a three-layer configuration system of "core-auxiliary-elasticity" can be constructed, as shown in the following table:

This configuration could reduce USDe's crypto-asset collateralization from the current 80% to 40%-50%, preserving the liquidity advantages of the crypto market while diversifying risk across markets through RWA assets. For example, gold tokens have a price correlation of only 0.2 with ETH, providing a valuable anchor during crypto market declines and preventing the panic sell-off seen in October 2025.

Re-enlightenment of the Austrian School: The Evolutionary Logic from Innovation to Maturity

USDe's flaws and RWA upgrade path further confirm the profound meaning of Hayek's "Denationalization of Money": Denationalized currency is not a static mechanism design, but a dynamic market evolution process. Only through continuous self-correction and innovation can it win in the currency competition.

The evolution of value foundation: from single market consensus to cross-domain value anchoring

USDe's current crypto-asset collateralization represents a "primary form" of non-state-owned currency in the digital age—its value consensus is limited to crypto market participants. The integration of RWA assets essentially expands this value consensus to traditional finance and the real economy, upgrading USDe's value foundation from "digital consensus" to "cross-domain real value." This evolution fully aligns with Hayek's advocacy that "the value of money should derive from the broadest market trust." When USDe is anchored to multiple assets such as crypto, gold, and US stocks, its ability to withstand the risks of a single market will be significantly enhanced, truly becoming a "value carrier that transcends sovereignty and a single market."

Improvement of regulatory mechanisms: from a single tool to multi-market coordination

The current USDe hedging mechanism relies on a single derivatives market, reflecting the "inadequate utilization of market instruments." Hayek's emphasis on "market self-healing" should be based on the synergy of multiple markets. The integration of RWA assets not only enriches the collateral pool but also creates the potential for synergistic hedging across the "crypto derivatives market + traditional financial market." For example, the volatility of US stock tokens can be hedged through traditional stock options, while gold tokens can be linked to forward contracts in the London gold market. This cross-market synergy makes the hedging mechanism more resilient and avoids reliance on the liquidity of a single market.

Conclusion: From innovation benchmark to evolutionary model

The market test of October 2025 not only validated the USDe's value as a benchmark for non-state-owned currency innovation, but also revealed its inevitable path from "primary innovation" to "mature currency." Its fundamental difference from LUNA-UST lies in its real value support and market regulation capabilities; its current institutional flaws are the inevitable cost of growth in the innovation process.

The MSX Research Institute believes that the upgrade strategy of incorporating RWA assets such as gold tokens and US stock tokens provides a clear evolutionary direction for USDe - this is not a negation of existing innovations, but a deepening and improvement guided by Hayek's ideas.

For market participants, the evolution of the USDe offers a profound lesson: the core competitiveness of non-state-owned currencies lies not only in their courage to break the monopoly of sovereign power, but also in their ability to continuously self-correct. Their value is judged not only by their short-term stable performance, but also by their long-term resilience in connecting to real value and adapting to market evolution. Once the USDe completes its RWA upgrade, it will no longer be merely an innovative experiment in the crypto market, but a truly cross-domain value carrier with the potential to challenge the traditional monetary system.

You May Also Like

Vanguard Increases Strategy Stake to $255M as MSTR Adds $2.54 Billion Bitcoin

USD/INR: RBI eases NDF curbs as Rupee stabilizes – Commerzbank