How can you tell if someone is a crypto scammer?

It condenses 2024 and 2025 authority guidance into plain steps: recognise red flags, verify addresses and identities, use available tools, and report quickly when needed. Use it as a starting point and follow primary sources for updates.

What cryptocurrency investors should know about crypto scams

Crypto scams remain a significant and evolving threat that everyday people encounter when they trade, invest, or interact with decentralised services. Industry analysis shows that the total value stolen and average loss per incident rose in 2024 and 2025, driven by larger transfers and more sophisticated laundering methods, which has practical consequences for anyone who holds digital assets Chainalysis report.

These risks matter because certain features of many crypto systems make scams more attractive to criminals: transfers are often irreversible, private wallet addresses can be hard to verify, and pseudonymous accounts let bad actors hide while they pressure targets to act quickly. Public authorities and industry reports repeatedly note these features as part of the risk picture IC3 annual report.

Advertise with FinancePolice to reach readers interested in personal finance and investing topics

Bookmark the checklist in this article and verify links and wallet addresses before you act.

Learn about FinancePolice advertising options

At the same time, some uncertainty remains about how tools that increase on-chain privacy will affect traceability and recovery efforts in 2026. Researchers and agencies continue to monitor developments, so staying updated with primary reports helps keep your approach current.

Top red flags cryptocurrency investors see in unsolicited contacts

Messaging and social engineering signs

Unsolicited messages that push you to act right away are a top red flag. Consumer authorities see urgent pressure, unexpected contact, and requests to bypass usual channels as consistent indicators of fraud, especially when the message asks you to move funds into a private wallet or to share sensitive account access FTC guidance.

Scammers use familiar formats to lower a target’s guard: chat messages claiming to be platform support, direct messages from social accounts posing as people you trust, or emails that mimic known brands. These messages often ask for quick confirmation, recovery codes, or permission to connect a browser wallet; responding without verification raises the odds of loss.

Investment promises and pressure tactics

Promises of guaranteed or unusually high returns are common banners for scam pitches. When an offer claims a sure outcome or pressures you to invest now to avoid missing out, treat the claim as suspect and step back to verify independently with regulators or recognised sources ACCC Scamwatch.

Other pressure tactics include time-limited offers, requests to transfer funds to private wallets, or instructions to use unverified apps. These tactics try to create a sense of urgency that reduces the chance you will pause to check addresses, domains, or identities.

A step-by-step verification checklist for cryptocurrency investors

Quick checks you can do in minutes

Before you send funds or approve a wallet connection, do these quick checks: verify the wallet address in a blockchain explorer, confirm the sender’s identity through official channels, and double-check the domain of any link by typing it yourself or using a bookmark. Using these short steps can catch the majority of simple scams Chainalysis report.

Also look for common message signals like unsolicited contact, spelling or formatting errors, and mismatched sender details. If anything feels off, pause and use the deeper checks below rather than sending funds immediately.

Look for unsolicited urgency, guaranteed return claims, and requests to move funds to private wallets; verify addresses with a blockchain explorer, confirm identities via official channels, enable technical protections, and report suspicious activity to the appropriate authority.

Deeper verification if you plan to send funds

If you plan to send a meaningful amount, run a deeper verification flow: check the wallet address on a blockchain explorer for prior activity, search for the person or platform name with public regulatory registers, and confirm reviews or independent mentions beyond the message thread. For identity claims tied to platforms, contact the platform using contact details published on its official site rather than those given in the message FATF guidance.

Consider doing a small, reversible test transfer where possible, and keep records of transaction IDs and communications so you can report quickly if something goes wrong.

How scammers operate: social engineering, impersonation, and on-chain patterns for cryptocurrency investors

Impersonation of exchanges and customer service

Impersonation remains a leading social-engineering method: scammers pose as exchange support, recovery teams, or trusted services to extract credentials or to trick people into moving funds. These attacks often begin with unsolicited contact and escalate by requesting codes or wallet approvals, which is a key behaviour to watch for in messages IC3 annual report.

Impersonation can also appear on social media, where accounts with similar names and copied profiles try to build trust. Always confirm identities through official support channels listed on the platform’s own website.

Romance and investment platform scams

Romance scams and fake investment platforms are common social vectors. These schemes use emotional persuasion or staged performance to get targets to send funds or reveal access. Europol and other authorities list these as primary theft drivers and caution that social pressure and requests to move funds to private wallets are frequent red flags Europol IOCTA.

In many cases the scammer asks the victim to transfer assets off-exchange or to a private wallet as a so-called safe step, which in practice removes protections that might otherwise help recovery or dispute resolution.

On-chain laundering signals

On-chain patterns also reveal aggressive laundering techniques: rapid movement of funds across many addresses, large transfers into known mixer services, and quick conversion between tokens can indicate attempts to obfuscate proceeds. Industry analysis found an increase in sophisticated laundering and larger transfers in 2024 and 2025, which makes tracing harder without specialised tools Chainalysis report.

While on-chain signals are not definitive proof of wrongdoing, they are useful indicators when combined with messaging red flags and verification failures.

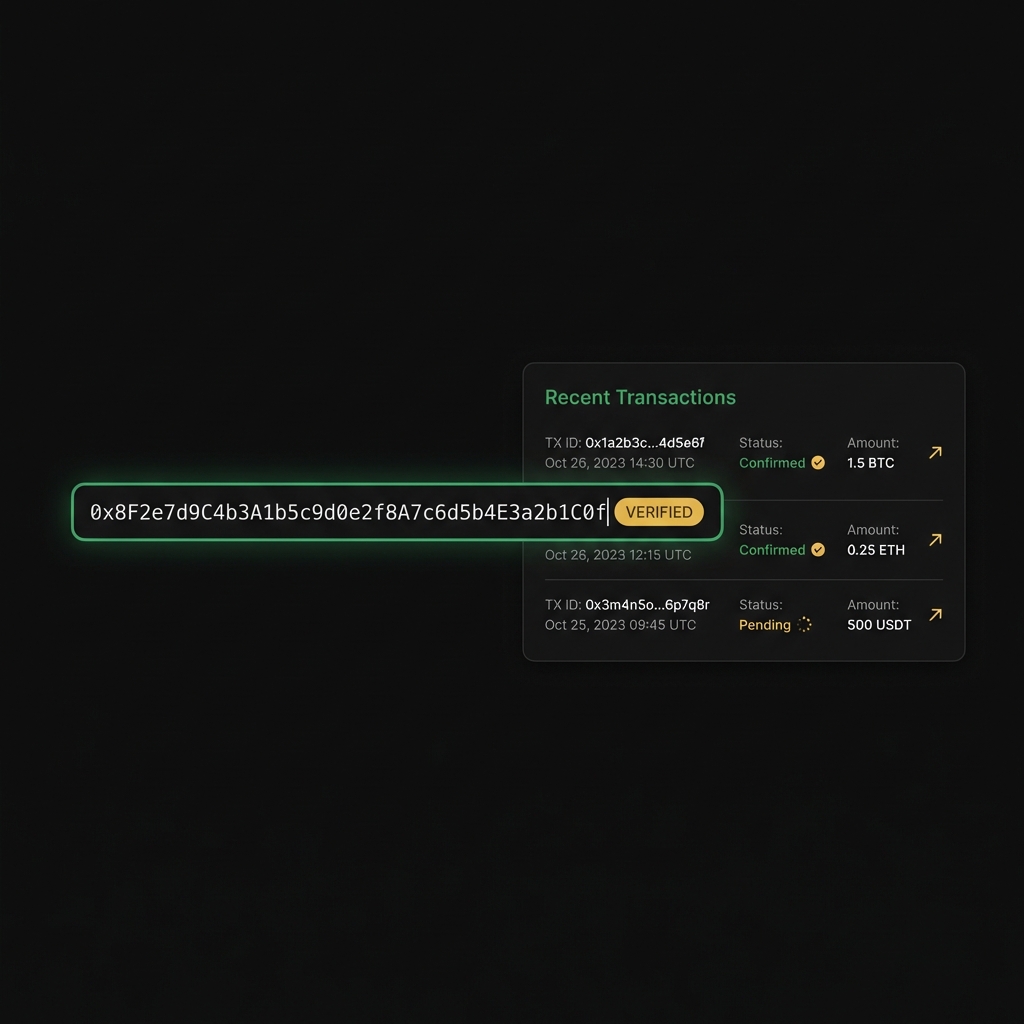

Guide to using a blockchain explorer to check an address

Use this to confirm prior activity and outgoing patterns

Verification tools and practical resources for cryptocurrency investors

Blockchain explorers and how to use them

A blockchain explorer lets you paste a wallet address and view its public transaction history. Checking the address first can show whether funds have moved through multiple hops, whether the address is inactive, or whether it has interacted with known mixer services, all of which are practical clues before you send money Chainalysis report.

When using an explorer, copy and paste addresses rather than typing them from a message, and double-check the first and last characters of an address after you paste. If you see rapid outgoing transfers or many small hops, pause and consider a deeper check.

Official complaint and regulator portals

If you suspect fraud, report quickly to the appropriate national complaint portal. In the United States, IC3 collects internet crime complaints and provides a route for law enforcement review, while consumer agencies like the FTC accept reports that feed prevention and education work IC3 annual report. See the IC3 cryptocurrency information page here.

In Australia, ACCC Scamwatch handles complaints and publishes alerts that help others spot emerging tactics. Preserve transaction IDs, screenshots, and the full message thread when you report; these materials are often crucial for investigators ACCC Scamwatch.

What to do if you suspect a scam or have been defrauded as a cryptocurrency investor

Immediate steps to take

If you believe you have been targeted, act quickly to limit ongoing exposure: revoke any granted wallet permissions, change passwords and two-factor authentication where possible, and contact any platform used in the flow to alert them to the incident. Preserving evidence early helps investigators and may be necessary for recovery attempts IC3 annual report. You can also see FBI Operation Level Up for victim assistance Operation Level Up.

Do not keep communicating with the suspected scammer. Stop further transfers and document every message, link, and transaction ID. Quick, clear records are one of the most useful things you can provide when you file a report with consumer authorities.

How to preserve evidence and report

Save screenshots of messages, copy transaction hashes, and export any chat logs you can access. Each jurisdiction has its own channels: use IC3 for U.S. internet crime reports, the FTC for consumer complaints, and ACCC Scamwatch in Australia. Reporting supports investigations and can help identify trends that protect other people FTC guidance.

When you report, include transaction IDs, timestamps, sender and recipient addresses, and a concise sequence of events. These details make it easier for investigators to prioritise and trace activity.

Technical protections every cryptocurrency investor should consider

Two-factor authentication and account hygiene

Two-factor authentication is a simple step that reduces account takeover risk. Use an authenticator app or hardware token rather than SMS when available, and enable 2FA on exchange and email accounts linked to your wallets. This reduces the likelihood that someone who obtains your password can immediately drain your accounts Europol IOCTA.

Good account hygiene also means unique passwords, a password manager, and cautious use of recovery links. Avoid reusing passwords across services and review account activity regularly.

Hardware wallets and permission management

For long-term holdings consider storing assets in a hardware wallet and keep smaller amounts in hot wallets used for trading. Hardware wallets add a physical confirmation step that increases security, and careful permissioning of browser wallets prevents blanket approvals that scammers exploit FATF guidance.

When a dApp or site requests wallet permissions, check exactly what it wants to do. Avoid blanket approvals like unlimited token allowances and revoke permissions you no longer need.

Decision criteria: when to trust an offer or contact as a cryptocurrency investor

Checklist to decide whether to engage

Use a short decision checklist before you engage: can you verify the identity through an official channel, is there independent corroboration, is the intermediary registered or regulated, and is there time to do a small test transfer? If the answer is no to one or more of these checks, lean toward not engaging FTC guidance.

Assess the offer against your risk tolerance and time horizon. For small speculative amounts you might accept more friction, but for larger sums the verification bar should be higher.

Red lines that should stop you

Walk away if the contact asks you to send funds to a private wallet as a condition of participation, guarantees returns, or insists you use an unverified app. These are common red lines cited by consumer agencies and industry reports and are reliable stopping points in decision making Chainalysis report.

Also be wary of unfamiliar payment flows that step outside regulated exchanges or well-documented services, especially when the other party resists independent verification.

Common mistakes cryptocurrency investors make that open the door to scams

Rushing without verification

Rushing to send funds without checking an address or domain is among the most common errors. A short pause to verify an address in an explorer and to confirm a domain can prevent a large share of losses documented in recent reports IC3 annual report.

Another frequent misstep is following links from unsolicited messages. Typing a known site address or using a saved bookmark reduces the risk of phishing pages that mimic legitimate services.

Reusing passwords and weak account hygiene

Password reuse, ignoring two-factor authentication, and granting blanket wallet permissions all increase exposure. Small habit changes, like unique passwords and periodic permission reviews, materially reduce risk even without technical expertise Europol IOCTA.

Overreliance on social proof from unverified sources is also risky. Comments or posts can be fabricated, so look for independent validation beyond the platform where the pitch appeared.

Practical scenarios: three real-world examples and how to handle them

Impersonated exchange support message

Scenario: You get a direct message from an account claiming to be an exchange support agent saying your withdrawal failed and asking for a confirmation code. Red flags: unsolicited contact and a request for codes or permissions. Quick steps: do not share codes, go to the exchange website manually, and open a support ticket via the official help portal. Preserve the message and any transaction IDs for reporting.

Deeper action if progressed: change your account passwords, revoke wallet permissions, and report the incident to IC3 or your local consumer agency.

Investment opportunity pitched over social media

Scenario: A social post offers a private deal that promises high returns if you send funds now. Red flags: urgency, guaranteed returns, and off-platform payment requests. Quick checks: search for independent reviews and regulatory registration, contact the platform through its official site, and do a small test transfer if you decide to proceed.

If you lose funds, collect timestamps, screenshots, and transaction hashes before filing a complaint with the appropriate portal.

Unknown wallet requests a transfer after a trade

Scenario: After a trade, an address asks you to move funds to a private wallet to ‘complete settlement.’ Red flags: shifting payment instructions post-trade and requests to use an external wallet. Quick steps: pause transfers, confirm settlement instructions with the exchange or counterparty via an independent channel, and check the address on a blockchain explorer for suspicious activity.

If contact persists, stop communications and report the contact while preserving all evidence for investigators.

Quick checklist summary for cryptocurrency investors

Five things to do before sending funds

Verify identity through an official channel, check the wallet address on a blockchain explorer, confirm the domain or app by typing it yourself, avoid urgent pressure lines, and preserve records of the interaction. These five steps form a fast pre-send routine that reduces common errors Chainalysis report.

When in doubt, default to not sending funds and use small test transfers where possible.

When to report and who to contact

Report suspected fraud to national complaint portals such as IC3, the FTC, or ACCC Scamwatch depending on your jurisdiction. Include transaction IDs, timestamps, and a concise description of events to assist investigators ACCC Scamwatch.

Key takeaways and next steps for cryptocurrency investors

Summary of the most important actions

The most reliable protections are simple: recognise unsolicited urgency and guaranteed returns as red flags, check addresses and domains before you act, enable technical safeguards like two-factor authentication, and report quickly if you are targeted. These steps reflect the practical guidance given by consumer agencies and industry reports FTC guidance.

Practice verification with small test transfers and keep your holding strategy aligned with your time horizon and risk tolerance.

How to build safer habits over time

Build habits by bookmarking official sites, keeping a short verification checklist handy, and reviewing account permissions regularly. Making these checks routine reduces the cognitive load when a real decision arrives.

Resources and where cryptocurrency investors can learn more

Official guidance links and why to trust them

This article draws on primary sources that document scam trends and verification best practices. Read official reports from consumer agencies and industry analysis to stay current because patterns and tools change over time Chainalysis report. See the Chainalysis 2026 Crypto Crime Report here and our crypto coverage at Finance Police crypto category.

Check regulator portals and industry reports for updates after 2025, especially where privacy tools or new laundering methods may change traceability assumptions.

Recommended habit-building resources

Use official complaint portals for reporting, practice verification steps with small transfers, and consider hardware wallets for long-term holdings. Treat this article as a starting point and verify details with primary sources and official guidance. Read related guidance and strategies such as strategies to reduce risk in cryptocurrency investments and our article on crypto influencers and their role.

Unsolicited contact, urgent pressure to act, promises of guaranteed returns, and requests to move funds to private wallets are common red flags. Pause and verify before you respond.

Verify the wallet address with a blockchain explorer, confirm the sender through official channels, check the domain manually, and consider a small test transfer.

Report to your national complaint portal or consumer agency, for example IC3 in the U.S., the FTC for consumer complaints, or ACCC Scamwatch in Australia, and preserve transaction IDs and messages.

FinancePolice aims to clarify the decision factors so you can make safer choices with your money. Verify details with primary sources and adjust your practices as tools and threats evolve.

You May Also Like

Jollibee opens new Manhattan store

Mark Cuban Says He Sold Most of His Bitcoin, Calling It a Failed Hedge

Blockchain.com Submits Confidential IPO Filing to SEC Amid Crypto Market Revival