Home Insurance Industry Statistics 2026: Growth Forecast

Home insurance, often a cornerstone of financial stability for families, saw significant shifts. Rising natural disasters, an unpredictable economic landscape, and evolving demographics are changing the way insurers approach policies, coverage, and premiums.

New trends emerged, highlighting the importance of affordable yet comprehensive coverage for homeowners. This article will explore key home insurance industry statistics, offering a well-rounded understanding of the current landscape and what it means for homeowners across the United States.

Editor’s Choice

- Global home insurance premiums reached about $336 billion in 2026, up from roughly $312 billion in 2025.

- Insured losses from natural disasters crossed $107 billion in 2025, marking the sixth consecutive year above the $100 billion threshold.

- US homeowners now pay an average of around $2,424 per year for a policy with $300,000 dwelling coverage.

- US home insurance premiums are projected to rise by about 8% in 2026, part of a 16% cumulative increase through 2027.

- Penetration of home insurance among mortgage holders remains near a record 96%, reflecting its embedded role in lending.

- In the US, more than 1 in 10 home insurance policies are written in high‑risk states such as Florida and Texas as of 2026.

Recent Developments

- California’s Sustainable Insurance Strategy is pushing wildfire‑zone premiums up by roughly 30–40%.

- State Farm is seeking an additional 11% rate hike in California, potentially taking its total increase to about 30% by 2026.

- Insurers have pulled back from high‑risk U.S. regions, pushing more than 1 in 5 wildfire‑prone homes into state‑backed plans.

- FAIR Plan’s recent wildfire losses are estimated at around $4 billion, triggering a $1 billion carrier assessment passed on to policyholders.

- Global insurers are carrying average solvency ratios above 200%, backed by €80 billion of capital relief under updated Solvency II by 2026–2027.

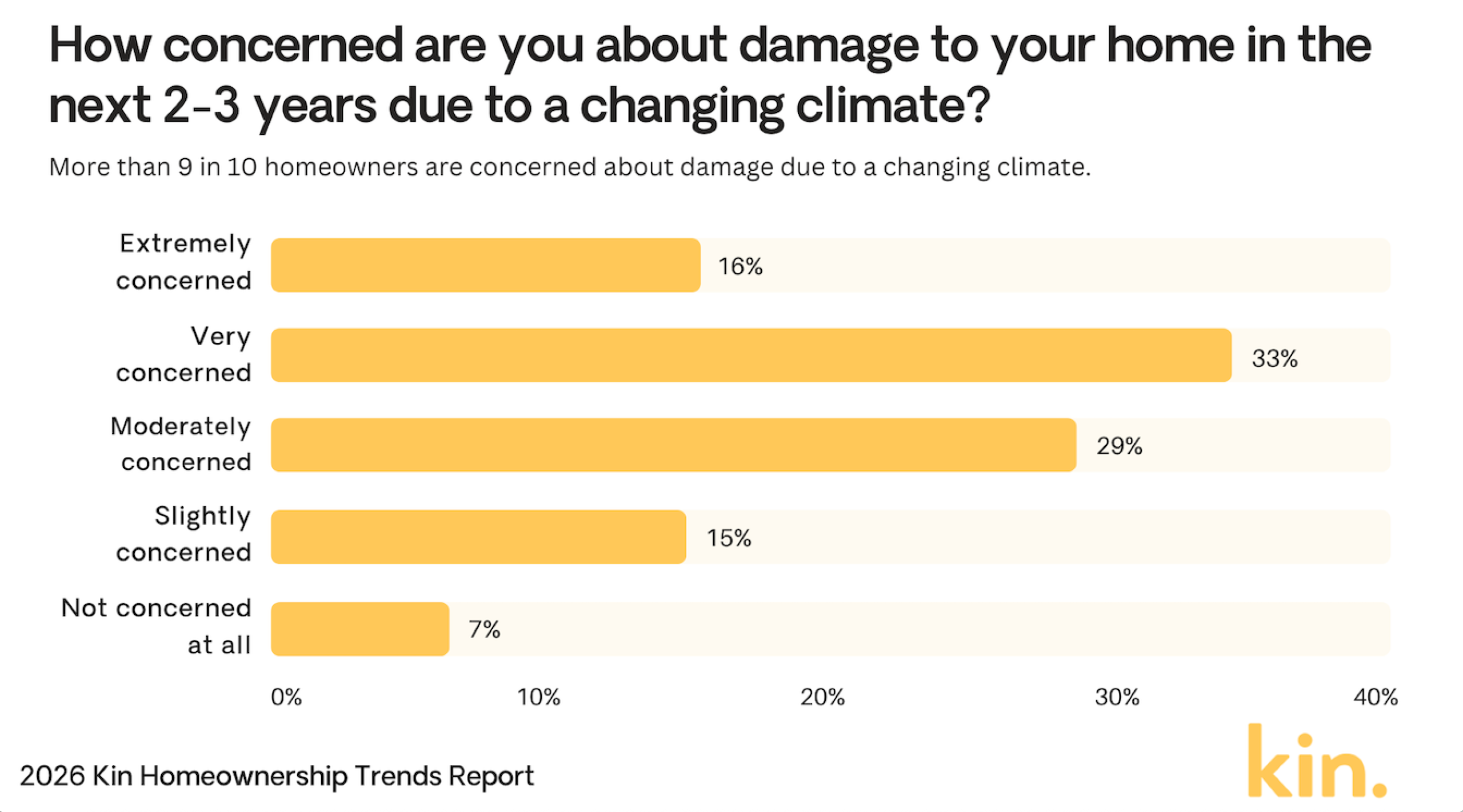

Homeowners’ Concern About Climate Damage

- 33% of homeowners are very concerned about climate damage to their homes.

- 29% feel moderately concerned, showing strong overall worry.

- 16% say they are extremely concerned about possible damage.

- 15% are slightly concerned about climate risks.

- Only 7% are not concerned at all.

- In total, 93% of homeowners show at least some level of concern.

(Reference: Kin Insurance)

(Reference: Kin Insurance)

Homeowners Insurance Premiums and Consumer Prices

- Average US annual home insurance premiums stand at about $2,424 in 2026, up from roughly $2,110 in 2025.

- Premiums in hurricane‑prone states like Florida and Louisiana are on track to rise by as much as 27%, with Florida averaging around $5,409 per year.

- Roughly 40% of policyholders have seen annual premium increases exceeding $200, particularly in high‑rebuild‑cost regions.

- The home rebuilding materials price index has climbed about 7–10% year‑over‑year, lifting both insurer and homeowner costs.

- About 20–30% of new homeowners’ policies in high‑risk zones now carry deductibles of $2,000 or more, up from prior averages near $1,200.

- Policy bundling for home and auto has increased by 15%, with typical savings in the range of 10–25%.

- Approximately 10–15% of insurers have tightened underwriting in high‑risk areas, restricting eligibility and raising premiums.

States Homeowners Avoid Due to Extreme Weather Risks

- 58% of homeowners say they would avoid moving to Florida because of extreme weather risks.

- 52% would avoid California, showing strong concern about disasters in the state.

- 24% say they would avoid Hawaii due to weather threats.

- 22% would avoid Louisiana, likely due to storm and flood risks.

- 21% of homeowners would avoid Texas.

- 21% would also avoid Alaska.

- Florida and California stand far above other states, with more than half of homeowners saying they would avoid them.

(Reference: Kin Insurance)

(Reference: Kin Insurance)

Causes of Homeowners Insurance Losses

- Natural disasters now account for roughly 70% of global insured catastrophe losses, with the U.S. shouldering the largest share.

- Flood‑related claims have climbed by about 28% year‑on‑year, driven by more frequent extreme rainfall in vulnerable regions.

- Wind and hail events generated approximately $44 billion in insured losses in the first half of 2025, pushing up national home insurance rates.

- Water damage and freezing still make up around 24.7% of all home insurance claims, underscoring their persistent cost impact.

- Property‑crime‑linked claims rose 10–12% in several suburban markets, especially where economic strain and policing gaps are growing.

- Wildfire‑related claims have surged by about 40% in western states such as California and Oregon amid prolonged drought and intense fire seasons.

- Roughly 40% of insurers have cut back or capped wildfire coverage in high‑risk zones to manage mounting loss volatility.

Home Insurance Market Share by Provider

- State Farm holds 18.4% market share with $24.4 billion in premiums written.

- Allstate commands 9% share, $12 billion in direct premiums.

- USAA captures 7.3% with $9.7 billion in premiums earned.

- Liberty Mutual at 6.6%, $8.8 billion in premiums written.

- Farmers Insurance has 6.2% share, $8.2 billion in premiums.

- Travelers owns 4.9% of the market, $6.5 billion written.

- American Family 4.4%, $5.8 billion premiums earned.

- Nationwide 2.8% share with $3.8 billion in premiums.

- Chubb secures 2.6%, $3.4 billion in direct premiums.

Top Challenges for the Home Insurance Industry

- 61% of home care leaders say rising costs and client affordability severely limit growth.

- Concerns about profitability have jumped from 13% to 34% of agencies in 2026.

- 53% of agencies still rank caregiver shortages as a top‑tier pain point.

- 60% of agencies expect increasing operational costs to hinder expansion this year.

- 65% of agencies see improving performance in their current market as the biggest growth opportunity.

- Nearly 48% of non‑US health executives cite cybersecurity and data privacy as a leading concern in 2026.

- EVV and labor‑compliance requirements are expected to add 15–20% more administrative burden for home care agencies.

- Agencies project they will need to raise caregiver pay by roughly 10–15% on average to compete for talent.

Top Reasons Why Americans Don’t Have Life Insurance

- 41% say they can’t afford life insurance.

- 32% believe the cost isn’t worth it.

- 27% don’t have dependents needing support.

- 26% feel too young for life insurance.

- 19% already have employer coverage.

- 15% think they’re in good health.

- 12% unaware of available options.

- 8% distrust insurance companies.

Average Home Insurance Rate Changes

- $200,000 coverage averages $1,450/year, up from $1,348.

- $350,000 coverage averages $2,151/year, up from $1,951.

- $500,000 coverage averages $2,891/year, up from $2,553.

- $750,000 coverage averages $5,254/year, up from $3,496.

- The national average for a $300,000 dwelling is $2,424/year.

- Premium growth slowed to 8.5% YoY in 2025.

- Average deductibles rose 22% in 2025.

- Forecasts predict 3-8% rate hikes in 2026.

Premiums for Homeowners and Renters Insurance

- Renters insurance averages $290/year or $24/month.

- 89% of insurers offer safety feature discounts up to 23%.

- Louisiana has some of the highest homeowners’ insurance premiums in the U.S., with statewide averages typically ranging from $4,000 to $6,000 annually

- 67% bundle home/auto, saving $450 yearly.

- 38% insurers tightened underwriting for high-risk homes.

- 23% renters added flood riders in Texas/Louisiana.

- National average dwelling coverage at $300k costs $2,600.

Most Common Types of Homeowners Insurance Claims

- Wind and hail claims account for 41% of total claims.

- Water damage and freezing comprise 28% of all claims.

- Fire and lightning losses represent 22%, averaging $89,500 per claim.

- Liability claims make up 1.6% of total filings.

- Theft claims are 0.7%, with payouts near $5,400.

- Other property damage covers 6.9% of incidents.

- Medical payments are 0.5% of claims.

- Average claim severity rose 7% YoY.

- Total claims frequency up 4.2%.

Frequently Asked Questions (FAQs)

Insurance accounts for 9% of a typical homeowner’s monthly mortgage payment.

HO-3 holds 63.50% market share.

Recent estimates place the national average homeowners insurance premium between $2,400 and $2,600 annually for standard $300,000 dwelling coverage, depending on methodology and insurer sampling.

Conclusion

As home insurance premiums continue to rise in response to economic and environmental factors, homeowners face new challenges in securing comprehensive yet affordable coverage. Key drivers like natural disasters, inflation, and policy changes will likely keep influencing insurance costs in the coming years.

Understanding the regional differences in insurance expenses, as well as staying informed about new developments, can help consumers make more informed choices about their coverage. Looking forward, home insurance companies may increasingly leverage technology and offer climate-resilient discounts, giving policyholders more options to adapt to this evolving landscape.

The post Home Insurance Industry Statistics 2026: Growth Forecast appeared first on CoinLaw.

You May Also Like

Solana (SOL) Positions for Breakout as Market Sentiment Turns Bullish

South Africa port reform accelerates investment