Stock Futures Flat As S&P Closes Out Best Quarter In 6 Years

Stock Futures Flat As S&P Closes Out Best Quarter In 6 Years

US index futures erased an earlier gain following some belligerent Iran headlines, but are still set to end a quarter that is set to be the S&P 500’s best in six years with markets behaving as though period-end dynamics have now completed. As of 8:30am, the S&P 500 was flat, pointing to a calm finish for the index that has surged 14% since the beginning of April. Nasdaq futures rose 0.1% erasing a sizable gain earlier, but on pace to close the quarter with a staggering 24% gain; In premarket trading, semis are mixed, Mag7 are flat, Cyclicals are generally leading Defensives with exceptions being Energy (lower) and Healthcare (higher). European stocks rallied, with gains led by Abivax SA after a clinical-trial update soothed investor concerns. Chipmakers drove Asian shares higher. JPM says with the major US holiday coming up, keep an eye on low liquidity moves in the region. Bond yields reversed an earlier drop to trade higher by 1bp pushing the 10Y yield to 4.39%. The USD is stronger, looking to erase all of yesterday’s losses. Commodities are stronger with crude flat into today’s US / Iran discussions, Metals seeing a bid, and Ags outperforming the other commodities complexes. Today's economic data calendar includes April Case-Shiller home prices (9am), June MNI Chicago PMI (9:45am, several minutes earlier for subscribers), June consumer confidence and May JOLTS job openings (10am) and June Dallas Fed services activity (10:30am). Fed speaker slate empty for the session. Chairman Warsh participates in an ECB panel event on Wednesday in Sintra

In premarket trading, Mag 7 stocks are mostly higher (Alphabet +0.3%, Amazon +0.1%, Apple unchanged, Meta Platforms +0.3%, Microsoft +0.4%, Nvidia +0.8%, Tesla (TSLA) -0.9%).

- AeroVironment (AVAV) soars 30% after the defense company reported fourth-quarter results that topped expectations and forecast 2027 revenue that at the midpoint exceeds estimates. Analysts note strength in its drones business.

- Aevex (AVEX) climbs 12% after winning a $50 million contract from the US Air Force to continue expanding unmanned mission‑support capabilities for current operations.

- Block (XYZ) inches about 1% higher after Piper Sandler upgraded the digital payments company by two notches to overweight, citing earnings potential.

- Concentrix (CNXC) tumbles 23% after the call-center company slashed its full-year outlook. The company’s forecasts for reported revenue and adjusted earnings per share also undershot Wall Street’s expectations.

- Patrick Industries (PATK) and LCI Industries (LCII) announced plans to combine in an all-stock merger. LCI shares are up 7%, while Patrick shares are halted.

- Replimune (REPL) gains 6% after BMO Capital Markets upgraded the drug developer by two notches to outperform from underperform, citing a clearer regulatory path for the firm’s experimental treatment of advanced melanoma.

- Space stocks were among the biggest US premarket gainers. Michael Saylor’s Strategy Inc. eased after Monday’s rally as Bitcoin dipped below $60,000. Microsoft Corp. was firmer, but still on course for its worst month since December 2000.

In other news, biotech company Abivax reported positive ABTECT maintenance part two results for experimental bowel disease drug Obefazimod. Susquehanna is attempting to identify individuals it claims made at least $100 million trading on inside information about a Chinese government crackdown on cross-border brokerages. Millennium will back a new quant hedge fund firm led by former Citadel researcher Paul Dou. Taiwan government agencies raided the offices of Super Micro Computer and several local affiliates as part of an investigation into the alleged smuggling of Nvidia chips into China. Blackstone is selling its stakes in a trio of data centers across Northern Virginia for $3.5 billion, cashing out of part of a bet it made less than three years ago.

Global stocks cemented gains ahead of another strong earnings season that analysts say will be driven by the debt-fueled investment boom in artificial intelligence. A strong macro backdrop will offer added support as falling oil prices help keep worries about inflationary pressures in check.

“US futures are being supported by renewed demand for tech, with investors returning to the view that IT offers one of the few strong and reliable earnings-growth stories,” said Marija Veitmane, head of equity research at State Street Global Markets. “That makes any jitters in tech look like a buying opportunity, and I think that is what we are seeing after last week’s wobble."

Investors will keep a close watch on peace talks scheduled for Tuesday after Iran reiterated its determination to control maritime traffic through the Strait of Hormuz. Oil prices remain an important part of the inflation outlook, with the Federal Reserve expected to hike interest rates as soon as September.

“The decline in oil prices suggests concerns around energy-driven inflation are largely behind us, but if AI-driven inflation from memory costs starts to materialize over the next two to three months, that will be important,” said Paisley Nardini at Simplify Asset Management. “The other risk is whether cracks start to emerge in the consumer.”

Elsewhere, US technology shares are at risk of declines as overall investor exposure to the cohort is extremely elevated, according to Citigroup strategists. Following last week’s price hikes by Microsoft and Apple, rising costs and component shortages are said to be leading to China’s smartphone brands slashing targets, according to the Nikkei.

“So far there are no signs of profit margins rising outside the tech sector. This is ultimately what we are waiting for, because the value of AI companies today rests entirely on the promise that margins in the S&P 493 will eventually climb,” noted Torsten Slok, chief economist of Apollo Global Management, referring to S&P 500 stocks beyond the Mag 7.

The outlook for US earnings momentum, according to a recent Citigroup indicator, remains positive. AI continues to make an outsize contribution with 44 AI companies projected to contribute around 60% to overall S&P 500 earnings growth across calendar 2026, growing earnings at roughly 40.7% — triple the rate of the rest of the S&P 500, Bloomberg Intelligence’s Nathaniel T Welnhofer recently noted.

In politics, Trump refused to commit to signing a major bipartisan housing bill, heightening uncertainty over the fate of the legislation. The Supreme Court has given Trump the power to fire the heads of independent agencies, overturning a 91-year-old precedent that said agencies must be independent of the president. Billionaire venture capitalist Marc Andreessen got a spot on a top Pentagon advisory board.

European stocks rallied in early Tuesday trading, poised for their best quarter since late 2020 as investors bet on an improved outlook for economic growth, with the Stoxx 600 benchmark set for a jump of nearly 10% in the past three months. Here are the biggest movers Tuesday:

- Abivax shares jump as much as 32%, the most since January, after a clinical-trial update soothed some investors’ concerns about whether cancer could be a potential side effect of the French biotech’s most promising experimental drug

- Genmab shares rise as much as 7.9% after the Danish biotech company reported positive late-stage trial results for its Epkinly drug combination in patients with relapsed or refractory diffuse large B-cell lymphoma

- Siemens gains as much as 3.3%, the most in two weeks, as analysts updated their estimates ahead of the German industrial group’s third-quarter earnings, due on Aug. 6, expecting a strong print from the company

- ITM Power shares rise as much as 19% after Berenberg raised its price target on the green-hydrogen equipment maker by 82%, citing a “significant growth opportunity” in its partnership with Rheinmetall

- Truecaller gains as much as 13% as DNB Carnegie reiterated its buy recommendation and raised its price target on the caller-ID company, saying its upcoming second-quarter report “should mark another step in Truecaller’s recovery”

- Maersk shares gains as much as 5.4%, the most in almost three weeks, after the Danish shipping group upgraded its full-year outlook. While the news is a positive, its seen as broadly anticipated by analysts

- Sainsbury’s shares rise as much as 3.5%, the most in seven months, after the British retailer reported 1Q sales that were in line with consensus expectations, avoiding the underperformance of its peer Tesco

- Kering shares slid as much as 5.4% on Tuesday, as analysts caution the luxury goods maker’s 1H earnings report is likely to show the turnaround at key brand Gucci remains gradual

- Teleperformance shares fall as much as 13% after Concentrix, a US peer of the French call-center operator, slashed its full-year outlook, with forecasts for reported revenue and adjusted EPS missing expectations

- Logitech shares fall as much as 4.9% after Bank of America downgraded the stock to underperform from neutral, seeing “demand destruction” for the Swiss firms’ computer peripherals due to price increases in consumer electronics

Asian stocks rose for a second day, driven by gains in technology shares as investors rebalanced portfolios at the end of the quarter. The MSCI Asia Pacific Index climbed as much as 1.5%, bringing its gain for the three months through June to 21%, the strongest quarterly advance since 2009. Japan’s tech-heavy Nikkei 225 marked its biggest ever quarterly advance, while South Korea’s Kospi index posted its best three-month period since 1998. In contrast, the MSCI China index has fallen for a third quarter. Taiwan’s Taiex index was among best performers in the region on Tuesday, with TSMC and MediaTek leading gains after the Philadelphia Semiconductor Index rose 3.8%. Stocks in Japan and South Korea rose. Offshore Chinese stocks continued to lose momentum, with the Hang Seng Index near a technical bear territory. MSCI China has tumbled about 15% this year, amid concerns over a sluggish economy, weak earnings from internet giants and investors’ preference for chipmakers elsewhere in Asia.

The region’s stocks continue to outperform global peers this year, underpinned by the enthusiasm in artificial intelligence. Chipmakers and hardware suppliers across markets such as Taiwan, Japan and South Korea have rallied as investors chase earnings growth and visibility to the AI buildout, while markets like India and China continue to struggle due to the lack of AI exposure.

“Asia is ending the first half with a selective risk-on tone: Taiwan and Japan are carrying the optimism built over the past few months, while weakness in China, Hong Kong and India shows investors are still cautious about markets without a clear AI, earnings or policy-support catalyst,” said Hebe Chen, a market analyst at Vantage Global Prime in Sydney.

In FX, the yen slid to its weakest level against the dollar since 1986, extending its recent losses to weaken beyond 162 against the dollar, a milestone that will generate unease in Japan and put traders on alert for authorities intervening in the market. Finance Minister Satsuki Katayama said Japan will respond to developments in foreign exchange at any time.

In rates, treasuries are mixed ahead of a reading of US job openings for May. Bloomberg Economics expects the JOLTS report to show declining vacancies and a low quits rate. While hiring is supporting personal income growth, wage pressures are likely to remain rather muted. Yields were within a basis point of Monday’s closing levels, after plying small ranges during Asia session and London morning. European bonds provide support after German state inflation gauges slowed in June. US 10-year yields around 4.37% are marginally richer on the day, and curve spreads are likewise little changed; bunds and gilts trade broadly in line with Treasuries. WTI crude oil futures, little changed, also support Treasuries as they head for biggest quarterly decline since the pandemic. IG dollar issuance slate includes four names so far. Four Yankee banks led a $17.2b US investment-grade new issue docket Monday. Borrowers paid about 3bp in new issue concessions on deals that were 3.5 times oversubscribed. Treasury coupon issuance resumes next week with 3-, 10- and 30-year tenors. Focal points of US session include a swath of economic data headed by consumer confidence and JOLTS job openings.

“The next validation point is now macro,” said Florian Ielpo at Lombard Odier Investment Managers. “JOLTS, consumer confidence, ISM and payrolls need to show enough labor resilience to keep the earnings momentum up, but not so much strength that the real-yield ceiling comes back immediately.”

In commodities, oil is headed for the biggest quarterly decline since the pandemic. Brent crude fell 0.3% to about $73 a barrel as flows through the Strait of Hormuz accelerated. Morgan Stanley analysts cut their oil price forecasts for the second time in about two weeks on a faster-than-expected supply rebound, while strong US supply and weak Chinese demand raise the risk of a glut.

Today's US economic data calendar includes April FHFA house price index and S&P Cotality CS home prices (9am), June MNI Chicago PMI (9:45am, several minutes earlier for subscribers), June consumer confidence and May JOLTS job openings (10am) and June Dallas Fed services activity (10:30am). Fed speaker slate empty for the session. Chairman Warsh participates in an ECB panel event on Wednesday in Sintra

Market Snapshot

Top Overnight News

- US and Iranian officials are set to hold peace negotiations in Doha today, but uncertainty hangs over the meeting. Donald Trump declined to say whether he expected a breakthrough and Iran has yet to confirm it’ll attend. Iran reiterated its determination to maintain control over maritime traffic in the Strait of Hormuz. BBG

- The unexpectedly rapid retreat in energy prices in the past week has further taken pressure off European Central Bank policymakers to lift interest rates next month but the case for a small hike later on remains firm, four sources told Reuters. RTRS

- China’s manufacturing activity expanded in June after remaining flat last month, thanks in part to resilient exports amid robust global demand for artificial-intelligence and green products. The official manufacturing purchasing managers index edged up to 50.3 this month from May’s 50.0. WSJ

- China has lifted some restrictions on oil-product exports in the past week, rolling back measures introduced to safeguard domestic supplies shortly after the war began in the Middle East. BBG

- Political pressure on the BoJ to slow its interest rate hikes is growing amid a push by Sanae Takaichi's government to restore dovish policymakers to the bank, a shake-up that could change its long-term policy direction. RTRS

- French and Italian inflation cooled more than expected in June, suggesting price pressures are beginning to soften amid falling energy costs due to easing tensions between the U.S. and Iran. WSJ

- US retailers have brought forward orders from China by four-to-six weeks to secure their inventories for Black Friday and Christmas holiday sales before expected tariff hikes later this year, shipping executives said. RTRS

- Companies investing most heavily in AI are adding workers faster than their peers, according to new research that challenges predictions of broad AI-driven job losses. FT

- ECB Chief Economist Philip Lane said knock-on effects from higher energy prices will take a while to show up and that policymakers won’t lock themselves into a rates path. BBG

- US House Speaker Johnson said no veto is expected for the housing legislation and that the housing bill will become law, while he noted that President Trump has yet to decide on signing the bipartisan housing package: POLITICO.

Iran News

- US President Trump's envoys Kushner and Witkoff are flying to Doha for talks, while Iran said the Doha mission is focused on ceasefire compliance and is not there for talks with the US, according to NYT.

- US Secretary of State Rubio said at a Congress briefing that there is a possibility the nuclear talks with Iran may fail, while he also stated that Iran has not yet received any funds under the MoU.

- Iranian President Pezeshkian said "Understanding is a bilateral matter. If the American side adheres to the memorandum of understanding, we will also fulfil our obligations", while he said their approach to unreasonable boasting and unfounded threats is to rely on rationality and human dignity in decision-making and to defend themselves decisively and fearlessly when taking action.

- Iran's Deputy Foreign Minister Gharibabadi said if they do not reach an understanding with Oman on the routes and arrangements of the Strait of Hormuz, they will, in any case, implement Iran's new sovereignty and policy in the Strait of Hormuz, while he added that they do not guarantee the safety and security of ships passing through parallel routes in the Strait of Hormuz.

- Iran's acting Defence Minister al-Reza said we do not trust the enemy and our hands are on the trigger in the event of any ceasefire violations, will take appropriate and necessary action.

- The framework agreement between Israel and Lebanon has reportedly caused a rift in Iran-Lebanon relations, with Iranian FM Araghchi refusing to visit Lebanon, according to Kan's Kais citing a Lebanese newspaper.

- An explosion was reported in southern Lebanon, which was carried out by Israeli forces, while it was also reported that Israeli forces conducted a strike on town of Deir Sryan in southern Lebanon and that Israeli attacks on Gaza left 48 dead and wounded, according to Tasnim and Mehr News Agency.

A more detailed look at global markets courtesy of Newsquawk

APAC stocks were mixed with choppy price action seen overnight heading into quarter-end, despite the gains in the US, where the DJIA notched a record close, and the Nasdaq outperformed amid strength in tech and communications. ASX 200 traded little changed amid mixed performances of its sectors and after the RBA minutes from the June meeting continued to affirm a hawkish stance. It stated that policy needed to remain restrictive and the RBA will do what is needed to achieve price stability, including raising rates if necessary. Nikkei 225 ultimately rallied, but initially swung between gains and losses, with the index fluctuating through the 70k level, amid a weaker currency, FX intervention risks, and disappointing Industrial Production. Hang Seng and Shanghai Comp lagged as a rebound in tech stocks was counterbalanced by losses in miners and energy majors, while they also failed to benefit from better-than-expected PMI data and another PBoC overnight repo operation.

Top Asian News

- Japanese Finance Minister Katayama won't comment on specific effects levels, but said they will respond appropriately to currency moves at any time as needed, while she added that action could include decisive action as agreed in the joint statement with the US.

- Japan's Chief Cabinet Secretary Kihara said he won't comment on FX levels, but added that they are always ready to take necessary action on FX.

- Decision on reducing Japan's consumption tax on food products has been postponed until July due to pushback from the opposition parties, according to TBS.

European bourses (STOXX 600 +0.8%) begin the last day of Q2 entirely in the green, with outperformance in the DAX 40 (+1.1%) and AEX (+0.7%). Many indices are set to have their biggest quarterly gain since the end of 2022, with the STOXX 600 just shy of 10% gains for Q2. Focusing on Germany's DAX, analysts see possible continued underperformance, with any flare-up in EU-China tensions posing a further headwind. Its auto sector has been particularly affected in recent months, with China playing a key role in that narrative.- European sectors highlight the positive bias. Basic Resources (+2.1%), Technology (+1.3%) and Industrial Goods & Services (+1.6%) are the outperformers, while Consumer Products & Services (-0.9%), Food, Beverages & Tobacco (-0.4%) and Telecoms (-0.3%) are the only sectors printing modest losses.

Top European News

- UK Government announced a GBP 15bln defence package.

FX

- Snapshot: G10s are lower against the USD to varying degrees. The CHF, EUR and JPY are all the laggards this morning, to the tune of c. 0.3%, whilst the Antipodeans are faring a little better vs peers.

- DXY is firmer this morning and trades at the upper end of a 101.12 to 101.42 range. No real driver this morning for the index, but comes amidst a tense geopolitical risk-tone and ahead of key US data. The slight strength today can also be explained as a bit of a bounce back, after recent USD strength has faded a touch off recent highs. The high from Monday (101.07) was breached this morning, whereby another bout of strength could see a test of Friday’s high (101.57) and Thursday’s best (101.74).

- EUR/USD is amongst the worst performers this morning, as markets digest the sheer amount of ECB speakers at Sintra. Overall, the bias has been hawkish; namely, President Lagarde and Chief Economist Lane have highlighted that the oil price curve remains elevated, and that could suggest higher costs for the economy. Nonetheless, policymakers have broadly reiterated data dependency and avoided any pre-commitment to July/September. On that front, Reuters sources suggested that given recent energy dynamics, September is now seen as more likely than July for another hike; the source clarified that a rate hike is not off the agenda. As it stands, money markets assign a 32% chance of a hike in July and a 70% chance of a move in September.

- On the data front, the EUR has had dovish German State CPI metrics to contend with. Broadly speaking they are indicative of a cooler Y/Y print, despite mainland consensus for the headline remaining at 2.6%.

- JPY is also amongst the laggards. Overnight, the pair jumped above the 162.00 mark, amidst commentary from Chief Cabinet Secretary Kihara. He initially suggested that he would not comment on FX, which saw the pair breach 162.00. However, a few minutes later, he stated that they are always ready to take necessary action on Forex. The move largely unwound on that jawboning attempt. Thereafter, Finance Minister Katayama also commented. She warned that they will respond appropriately to currency moves at any time as needed, while action could include decisive action as agreed in the joint statement with the US. USD/JPY currently holds within a 161.89-162.41 range.

Fixed Income

- Global fixed income benchmarks are firmer across the board, helped by softer energy prices, but also supported by cooler inflation prints in the EZ.

- Bund (+13 ticks) upside initially came following the French inflation data, in which HICP softened to 2%, below the expected 2.4% and from the prior 2.8%. This followed the Spanish print on Monday, which came in slightly hotter-than-expected, but saw relief after the core figure cooled. The German state CPIs can give further relief for the ECB, after prices broadly cooled in all states. This comes ahead of the nationwide figure later today; HICP is expected to hold at 2.7%.

- Many ECB policymakers were also on the wires this morning at the sidelines of Sintra. President Lagarde kicked off the Sintra conference on Monday. Even though her comments sounded slightly hawkish, it seemed to be an unwind of her dovish stance when she spoke last week in a way to keep all options on the table. Lane was the first GC member to speak today, in which he highlighted that the oil price curve is seen elevated in the coming years, which suggests higher economic costs.

- USTs (+2+ ticks) follow its German counterpart higher, albeit to a lesser extent, with focus this week being on comments by Fed Chair Warsh at Sintra on Wednesday and the US jobs report on Thursday.

- JGBs (-3 ticks) traded on the softer side in the Asia-Pac seen, however there was some relief following the 2-year JGB auction. The b/c was 4.82x, which was higher than the prior 3.70x and above the 12-month average of 3.74x. The strong auction was also backed by a small price tail. Despite the strong auction, investors remain concerned about further BoJ hikes, and perhaps more aggressively, to stabilise the Yen (USD/JPY recently topped 162.40).

- Japan sells JPY 2.15tln 2-year JGBs b/c 4.82 (prev. 3.70), average yield 1.407% (prev. 1.369%).

Commodities

- Crude benchmarks are firmer, posting gains of around USD 0.10/bbl at highs of USD 70.88/bbl and USD 74.08/bbl for WTI and Brent, respectively.

- In brief, we await any information relating to or stemming from the Doha talks. US envoys Kushner and Witkoff are travelling to Doha. However, Iran has made clear it will not be holding talks with the US “at any level” in the next few days, with the Doha gathering to only discuss ceasefire compliance. Albeit, sources via Pakistani journalist Mallick suggest that talks could occur via Pakistani/Qatari mediators.

- Spot gold firmer, but only marginally so. Overnight, pressure was seen alongside a jump in USD/JPY (see FX/morning JPY update for details), action that was exacerbated by a breach of the USD 4000/oz mark to the downside. Sending XAU to a USD 3942/oz base.

- In the first part of the European morning this unwound, with XAU climbing back above USD 4k/oz and hitting a USD 4037/oz peak in short order. There wasn’t a specific or fresh fundamental driver behind this, though the move did take place alongside a modest uptick in the fixed income space, marginal downside in energy and a moderation of the performance of both European and US equity futures.

- Base metals in focus after the EU increased tariffs on steel. The move will reduce the duty-free import level by an average of 47%. Following the move, an official cited by the FT outlined that the EU hopes to create a “steel club” with the US and others, in order to reduce trade barriers. Broadly, base metals are firmer, reflecting the risk tone and despite the firmer USD.

- US President Trump posted "Gasoline Retailers must get their Prices down, IMMEDIATELY! They’re too high considering that Oil is now at $68 a Barrel, and heading south. The Retailers must quickly react to this statement, and do what they know is right".

- Shell (SHEL LN) expects LNG demand to increase by around 65% by 2050, largely driven by APAC nations.

- China is said to be easing some refinery fuel export restrictions as domestic supply is ample, according to reports.

- Morgan Stanley slashes its Q3 dated Brent forecast by USD 15 to USD 75/bbl as supply returns through Hormuz.

Trade/Tariffs

- USTR posted that the US welcomes Switzerland’s progress in implementing elements of a historic Framework Agreement, while it was stated that they will continue to work towards the conclusion of an agreement on fair, balanced, and reciprocal trade that will further remove non-tariff barriers.

- China and the EU agreed to maintain global supply chain stability, continue consultations on trade, and solve some intellectual property issues, while China and the EU exchanged market access lists.

- EU declared new rule to protect EU steel. The EU's steel measure, which enters into application on 1 July 2026, reduces duty-free imports of 26 categories of steel products into the EU by an average of 47% as compared with the quotas under steel safeguard.

- White House announced temporary suspension of duties on fertilizer from Morocco, according to a Fact Sheet

Central Banks

- ECB's Lane said there has been some improvement in confidence, but not at pre-war levels. He added that the oil price curve sees elevated levels in the years coming, which suggest higher cost for the economy. On the ECB's rate path, he said July vs September is too narrow a debate but aiming to keep options open by not boxing themselves into a specific meeting.

- ECB's Nagel said it is too early make rate hike calls but rate policy has to stay vigilant as inflation may stay significantly above target.

- ECB's Wunsch said we might need another hike and would rather move quickly if the ECB needs another hike. A quick ECB move does not necessarily mean a July move.

- ECB's Sleijpen said while oil prices have come down, there is still a lot of uncertainty and reiterated the ECB's data-dependent approach.

- ECB sources said a rapid oil price retreat eases pressure on the ECB to hike in July and September is seen as more likely, although a June inflation surprise could reignite talk of a July hike, while sources added that a rate hike is not off the agenda even though it may be delayed, according to Reuters.

- BoJ's Sato said the de-escalation of the Middle East conflict is a welcoming move but uncertainty remains on outlook.

- RBA Minutes from the June meeting stated that policy needed to remain restrictive and it will do what is needed to achieve price stability, including raising rates if necessary. The Board saw merit in using the room created by earlier hikes to assess how the economy was faring and noted that leaving rates unchanged would best balance inflation and jobs objectives. Furthermore, it stated that the economy was operating with excess demand and broad-based price pressure, as well as noted that the Middle East conflict still posed material upside risks to inflation and downside risks to activity.

Geopolitics

- Russia reported it shot down 419 Ukrainian drones overnight.

US Event Calendar

- 9:00 am: Apr FHFA House Price Index MoM, est. 0.15%, prior 0.1%

- 9:45 am: Jun MNI Chicago PMI, est. 55.1, prior 62.7

- 10:00 am: Jun Conf. Board Consumer Confidence, est. 94.4, prior 93.1

- 10:00 am: May JOLTS Job Openings, est. 7295.5k, prior 7618k

DB's Jim Reid concludes the overnight wrap

As we hit the last day of the first half of the year, markets in Asia are largely continuing trends seen in the year and quarter to date. The KOSPI (+3.23%) is leading gains and remains on track for an impressive quarterly rise of over 65% and exceeding 105% YTD. Japan’s Nikkei (+1.70%) is also notably higher, now more than 37% higher for the quarter. Elsewhere the CSI (+1.12%) and Shanghai Composite (+0.20%) are also up but the Hang Seng (-1.19%) and the S&P/ASX 200 (-0.08%) are lower. Minutes from the RBA’s June meeting indicated that policymakers remain cautious about inflation and will continue to evaluate incoming data before making policy adjustments. S&P (+0.14%) and Nasdaq (+0.44%) futures are higher as I type.

In China, manufacturing activity in June slightly exceeded forecasts, supported by strong export demand and continued investment in artificial intelligence. The official manufacturing PMI rose to 50.3, above expectations of 50.1, and up from 50.0 in May. Meanwhile, the non-manufacturing PMI improved to 50.2, surpassing the 49.9 forecast and edging up from 50.1 previously, signaling modest improvement in services activity despite overall subdued demand.

The Japanese yen has weakened further overnight even with officials commenting that intervention could happen at any time. Over the last 24 hours it's fallen to its lowest level against the US dollar since 1986, closing at 161.94 last night and now trading at 162.40 this morning. So historic times for Japan.

Ahead of all this, markets saw a decent risk-on move yesterday, as a recovery in tech stocks helped to lift US equities more broadly. So the Magnificent 7 (+2.58%) bounced back, which meant the S&P 500 (+1.18%) finally ended a run of 5 consecutive declines. Indeed, with just one day of Q2 left, the S&P is on the verge of its best quarterly performance in six years, back when the index was bouncing back sharply from the pandemic slump. Those moves yesterday included a big advance for Tesla (+8.46%), Alphabet (+4.79%) and Amazon (+3.20%). And the Philly semiconductor index (+3.83%) rebounded after posting its worst week since the post-Liberation Day sell-off last April. It was a more mixed day for the rest of the US stock market, but both the equal-weighted S&P 500 (+0.18%) and the small-cap Russell 2000 (+0.01%) still inched up to new record highs. And over in Europe, equities were basically flat, with the STOXX 600 up +0.04%. European futures are around +0.6% higher this morning.

Perhaps the biggest story yesterday was news on Fed independence, as the US Supreme Court voted 5-4 that Fed Governor Lisa Cook could remain in post while fighting Trump’s attempt to remove her over allegations of mortgage fraud, ruling that the President could not remove her without proof of wrongdoing. It’s worth noting that’s not the end of the story, as they didn’t rule on whether Trump could fire Cook if the allegations were found to be true, but it means she can stay in post for now.

On the broader legal backdrop, the Court also ruled separately that the President can remove senior officials at other independent agencies without needing to meet the longstanding “for cause” standard, effectively overturning a 91-year precedent. In practical terms, that tilts the balance of power back towards the executive, giving the White House greater scope to replace officials across much of the regulatory apparatus. The carve out for the Fed therefore looks quite deliberate, reinforcing its unique independent status, but it also raises the stakes around how durable that distinction proves over time. If anything, it points to a more uncertain institutional backdrop, where independence can no longer be taken as a given across the wider policy framework—even if the Fed remains insulated for now.

Elsewhere, oil prices picked back up yesterday as they reacted to the weekend strikes that took place between the US and Iran, even if the weekend ended in a better place than it started with a halt to tit-for-tat strikes agreed by both sides late on Sunday night. So Brent crude (+1.61%) rose from its 4-month low on Friday, closing at $73.15/bbl, with WTI (+2.20%) back up to $70.75/bbl. That oil move also came as Iran’s Deputy Foreign Minister said that Tehran will control maritime traffic through the Strait of Hormuz with or without Oman. Otherwise, further meetings are set to take place today, with Trump posting that Iran had requested a meeting that would take place in Doha. And separately, Axios reported that the US’ Steve Witkoff and Jared Kushner would be travelling to Doha to meet today with the Qatari PM and other officials. They also reported that the US and Iranian technical teams would meet separately with the Qatari and Pakistani mediators.

That uptick in oil prices meant inflation concerns crept back in a bit yesterday on both sides of the Atlantic. So the US 1yr inflation swap (+4.5bps) was back up to 2.14%, from a 20-month low on Friday. And in turn, investors priced in a more hawkish path for the Fed, with the amount of hikes priced by the December meeting up +1.4bps on the day to 33bps. So that led to another rise in Treasury yields, with the 2yr yield (+1.4bps) up to 4.11%, whilst the 10yr yield (+0.5bps) moved up to 4.38%.

Meanwhile in the Euro Area, there was a similar pickup in bond yields across the continent. That was partly because of the oil move, but we also started to get the flash CPI prints for June, with Spain’s release surprising on the upside yesterday. It showed CPI unexpectedly remaining +3.6% (vs. +3.4% expected), which added to concerns that the other prints might come in on the stronger side too, and that the ECB would need to keep hiking rates. Indeed, market pricing moved in a slightly hawkish direction, with 27bps of hikes now priced by the December meeting, up +2.6bps on the day. And in turn, yields on 2yr bunds (+2.1bps) moved higher, while those across 10yr bunds (+0.7bps), OATs (+0.5bps) and BTPs (-0.4bps) were more stable.

Here in the UK, gilts were a relative outperformer, with the 10yr yield falling -1.5bps to 4.72%. That came as the favourite to be next PM, Andy Burnham, delivered a speech outlining some of his plans, which included a commitment to stick to the current fiscal rules. So that reassured investors who were concerned about looser fiscal policy, and there was also some underwhelming UK data as well. For instance, mortgage approvals for May fell more than expected to 56.2k (vs. 63.0k expected), which is their lowest since December 2023.

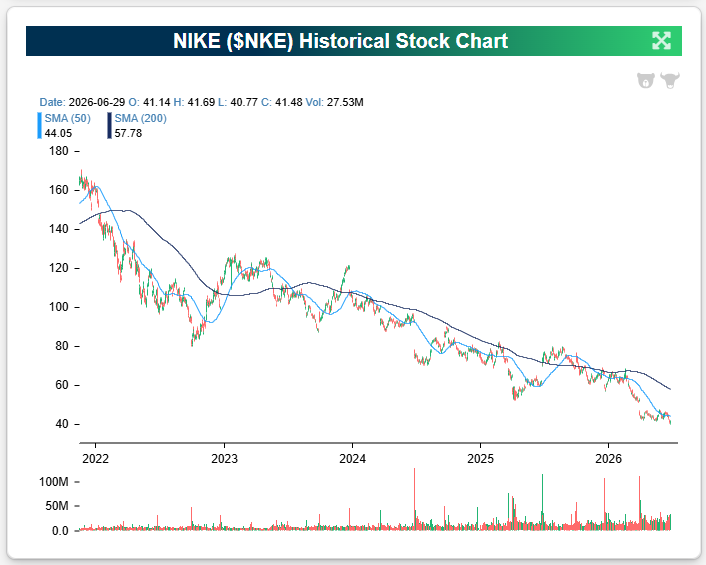

Looking at the day ahead, data releases include the flash June CPI prints from Germany, France, and Italy, along with German unemployment for June. Meanwhile, US releases include the JOLTS report for May, the Conference Board’s consumer confidence for June, and the FHFA’s house price index for April. Otherwise from central banks, we’ll hear from the ECB’s Vujcic, Elderson, Schnabel, Cipollone and Lane, along with the BoE’s Breeden. Finally, today’s earnings releases include Nike.

Potrebbe anche piacerti

Why this former OpenAI researcher thinks it’s time to start gaming out AI’s future

Nike (NKE) – Can the Swoosh Recover?