Stablecoins: Unlocking Revolutionary Payment Solutions Beyond Card Fees

BitcoinWorld

Stablecoins: Unlocking Revolutionary Payment Solutions Beyond Card Fees

Are stablecoins a threat to traditional banking, or do they offer a revolutionary alternative to costly payment systems? Recent discussions have painted a picture of stablecoins potentially undermining bank deposits. However, Coinbase, a leading cryptocurrency exchange, presents a compelling counter-argument, suggesting that the true competitive arena for stablecoins lies elsewhere: in the lucrative world of card processing fees.

Understanding the True Role of Stablecoins

Coinbase recently challenged the narrative put forth by some U.S. banks and regulators. These institutions often express concerns that the rise of stablecoins could lead to significant outflows from traditional bank accounts. But what exactly is the foundation of this debate?

- Not a Savings Vehicle: Coinbase’s analysis, as reported by Cointelegraph, clearly indicates that stablecoins are not primarily used for long-term savings. Unlike traditional bank deposits, which often serve as a secure place for holding wealth and earning interest, stablecoins are designed for different purposes.

- A Payment Innovation: Instead, stablecoins function predominantly as a highly efficient means of payment. Think of them as digital cash, pegged to a stable asset like the U.S. dollar, facilitating rapid and low-cost transactions across borders.

This distinction is crucial for understanding their impact on the financial ecosystem. The exchange’s findings suggest there’s no significant link between the growing adoption of stablecoins and a decrease in regional bank deposits.

Why Stablecoins Challenge Card Fees, Not Bank Deposits

The core of Coinbase’s argument pivots on where stablecoins genuinely compete. The company highlights that their primary utility aligns with challenging the high costs associated with traditional payment rails, particularly credit and debit card fees.

- International Remittances: Sending money across borders using traditional methods can be slow and expensive. Stablecoins offer a faster, more cost-effective alternative, enabling individuals to send funds globally with significantly reduced fees and processing times.

- Supplier Payments: Businesses often face substantial fees when paying international suppliers through conventional banking channels. By leveraging stablecoins, companies can streamline these payments, cutting down on expenses and improving cash flow management.

Coinbase points out that U.S. banks annually collect an astounding $187 billion in card fee revenue. This colossal figure represents a massive market where stablecoins can offer a competitive, often superior, solution. Rather than eroding deposit bases, stablecoins are poised to disrupt the economics of transaction processing.

Unlocking Revolutionary Payment Solutions with Stablecoins

The potential of stablecoins as a payment solution is truly transformative. They bring several advantages that traditional payment systems often struggle to match, especially in a globalized economy.

- Speed and Efficiency: Transactions using stablecoins can settle in minutes, not days, regardless of geographical distance. This speed is invaluable for businesses requiring rapid transfers and individuals needing urgent remittances.

- Reduced Costs: By cutting out numerous intermediaries and leveraging blockchain technology, stablecoins dramatically lower transaction fees compared to wire transfers, international bank transfers, and even many credit card processing charges.

- Accessibility: For the unbanked or underbanked populations globally, stablecoins offer a gateway to participating in the digital economy, enabling them to send and receive payments without needing a traditional bank account.

This efficiency and cost-effectiveness position stablecoins not as a threat to the fundamental role of banks as custodians of savings, but as a powerful alternative for the movement of money.

Navigating the Future: Benefits and Challenges for Stablecoins

While the benefits are clear, the path forward for stablecoins isn’t without its challenges. Regulatory clarity remains a key hurdle, but it also presents an opportunity for standardized growth.

- Regulatory Scrutiny: Governments worldwide are grappling with how to regulate stablecoins. Clear frameworks are essential to foster innovation while ensuring consumer protection and financial stability.

- Interoperability: Ensuring that different stablecoins and blockchain networks can seamlessly interact will be crucial for widespread adoption.

- User Education: As with any emerging technology, educating users about how stablecoins work, their benefits, and how to use them securely is vital for mainstream acceptance.

Despite these challenges, the inherent advantages of stablecoins in facilitating efficient, low-cost global payments make their continued growth almost inevitable. They are pushing the boundaries of what’s possible in digital finance, forcing traditional institutions to innovate or risk being outpaced in the payment processing arena.

In conclusion, Coinbase’s stance offers a vital perspective: stablecoins are not aiming to replace bank deposits but rather to revolutionize the payment landscape. By providing a cheaper, faster, and more accessible alternative to traditional card fees and international transfer methods, stablecoins are poised to unlock immense value for individuals and businesses worldwide. This shift isn’t about undermining financial stability; it’s about fostering competition and driving innovation in how we move money in a digital age.

Frequently Asked Questions (FAQs)

1. What is Coinbase’s main argument regarding stablecoins?

Coinbase argues that stablecoins primarily compete with high card processing fees and international payment costs, rather than threatening traditional bank deposits.

2. How do stablecoins differ from traditional bank deposits?

Unlike bank deposits, which are often used for savings, stablecoins are designed as a means of payment for quick, low-cost transactions, particularly across borders.

3. What are the primary uses of stablecoins identified by Coinbase?

Coinbase highlights international remittances and supplier payments as key areas where stablecoins offer a superior alternative to traditional methods.

4. What is the approximate annual revenue from card fees collected by U.S. banks?

U.S. banks collect an estimated $187 billion annually from card fee revenue, a market segment where stablecoins present a competitive solution.

5. What are the key advantages of using stablecoins for payments?

Key advantages include increased speed and efficiency, significantly reduced transaction costs, and greater accessibility for global payments, including for the unbanked.

Did you find this article insightful? Share it with your network to spread awareness about the transformative potential of stablecoins in reshaping global payments!

To learn more about the latest crypto market trends, explore our article on key developments shaping Bitcoin price action.

This post Stablecoins: Unlocking Revolutionary Payment Solutions Beyond Card Fees first appeared on BitcoinWorld.

추천 콘텐츠

South Korean Gaming Company NXC Decides to Reduce Its Crypto Holdings! Here Are the Details

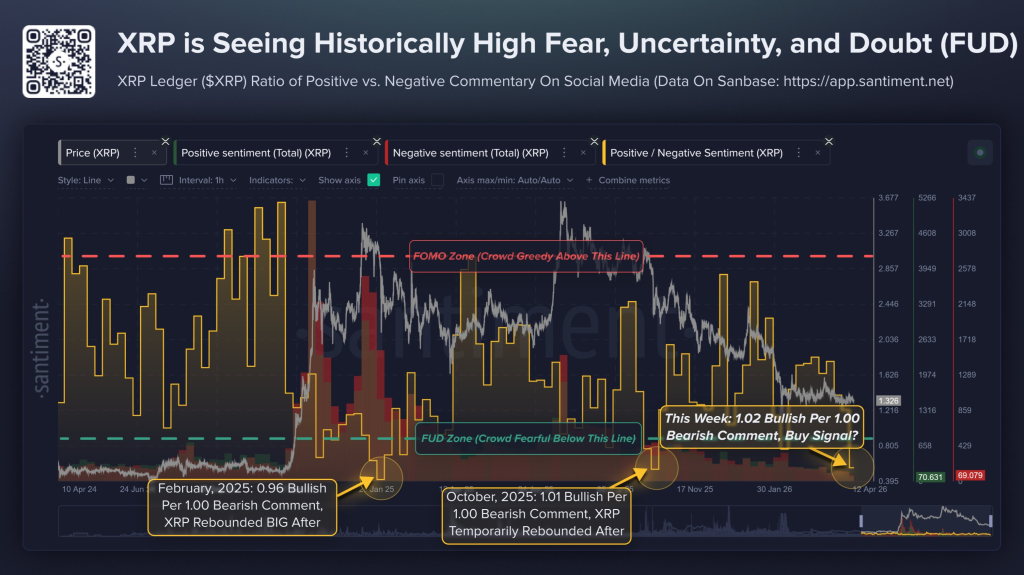

XRP Sentiment Just Flashed a Rare Contrarian Signal – Here’s What Happened the Last Two Times