Coinbase Policy Chief Pushes Back on Bank Warnings That Stablecoins Threaten Deposits

Contrary to claims from the U.S. banking industry, stablecoins do not pose a risk to the financial system, according to the chief policy officer at crypto exchange Coinbase (COIN), Faryar Shirzad. Banks' claims that they do are are myths crafted to defend their revenues, he wrote in a Tueday blog post.

"The central claim — that stablecoins will cause a mass outflow of bank deposits — simply doesn’t hold up," Shirzad wrote. "Recent analysis shows no meaningful link between stablecoin adoption and deposit flight for community banks and there’s no reason to believe big banks would fare any worse."

Larger lenders still hold trillions of dollars at the Federal Reserve and if deposits were really at risk, he argued, they would be competing harder for customer funds by offering higher interest rates rather than parking cash at the central bank

According to Shirzad, the real reason for banks' opposition is the payments business. Stablecoins, digital tokens whose value is pegged to a real-life asset such as the dollar, offer faster and cheaper ways to move money, threatening an estimated $187 billion in annual swipe-fee revenue for traditional card networks and banks.

He compared the current pushback to earlier battles against ATMs and online banking, when incumbents warned of systemic dangers but, he said, were ultimately trying to protect entrenched profits.

Shirzad also dismissed reports predicting trillions in potential outflows from deposits into stablecoins, whose total market cap is around $290 billion, according to data from CoinGecko. He stressed that stablecoins are primarily used as payment tools — for trading digital assets or sending funds abroad — not as long-term savings products.

Someone purchasing stablecoins to settle with an overseas supplier, he argued, is opting for a more efficient transaction method the going through their bank, not pulling money from a savings account.

He urged banks to embrace the technology instead of resisting it, saying stablecoin rails could cut settlement times, lower correspondent banking costs and provide round-the-clock payments. Those institutions willing to adapt, he wrote, stand to benefit from the shift.

The U.K., too, faces concerns about the effect of stablecoins on the financial industry.

The Financial Times reported Monday that the Bank of England is considering setting limits on how many "systemic" stablecoins people and companies can hold — setting thresholds as low as 10,000 pounds ($13,600) for individuals and about 10 million pounds for businesses.

Officials define systemic stablecoins as those already widely used for U.K. payments or expected to become so, and say the caps are needed to prevent sudden deposit outflows that could weaken lending and financial stability.

추천 콘텐츠

South Korean Gaming Company NXC Decides to Reduce Its Crypto Holdings! Here Are the Details

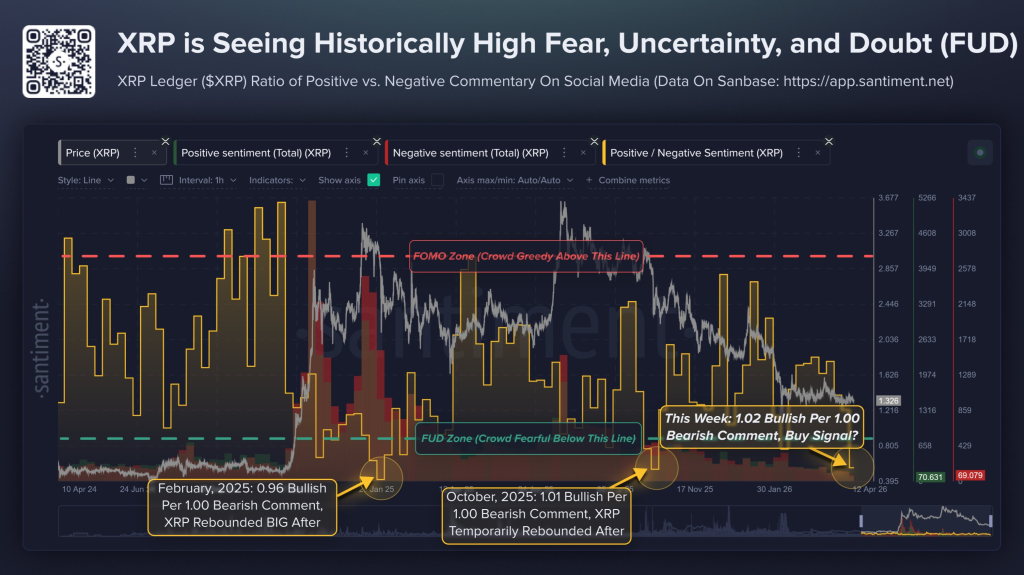

XRP Sentiment Just Flashed a Rare Contrarian Signal – Here’s What Happened the Last Two Times