Zazu, a digital financial operating system designed for African small and medium-sized enterprises (SMEs), has raised $1 million in pre-seed funding to accelerate its rollout in South Africa and Morocco.Zazu, a digital financial operating system designed for African small and medium-sized enterprises (SMEs), has raised $1 million in pre-seed funding to accelerate its rollout in South Africa and Morocco.

Backed by $1 million, Zazu is building a Mercury-style banking experience for African SMEs

For feedback or concerns regarding this content, please contact us at crypto.news@mexc.com

Zazu, a digital financial operating system designed for African small and medium-sized enterprises (SMEs), has raised $1 million in pre-seed funding to accelerate its rollout in South Africa and Morocco and lay the foundation for broader pan-African expansion in 2026.

This funding round saw participation from Plug and Play Ventures, as well as investors and fintech founders from Launch Africa Ventures, AUTO24.africa, Paymentology, Chari, Fiat Republic, and several founding members of European fintech unicorns like Qonto and Solarisbank.

Founded in 2024 by Rinse Jacobs and Germain Bahri, both former employees at the German banking-as-a-service unicorn Solarisbank, Zazu is positioning itself as a “Mercury-style” banking experience for Africa. With over 50 SMEs already in beta and a waitlist exceeding 1,000 businesses, the startup aims to solve the funding gap affecting Africa’s “missing middle.”

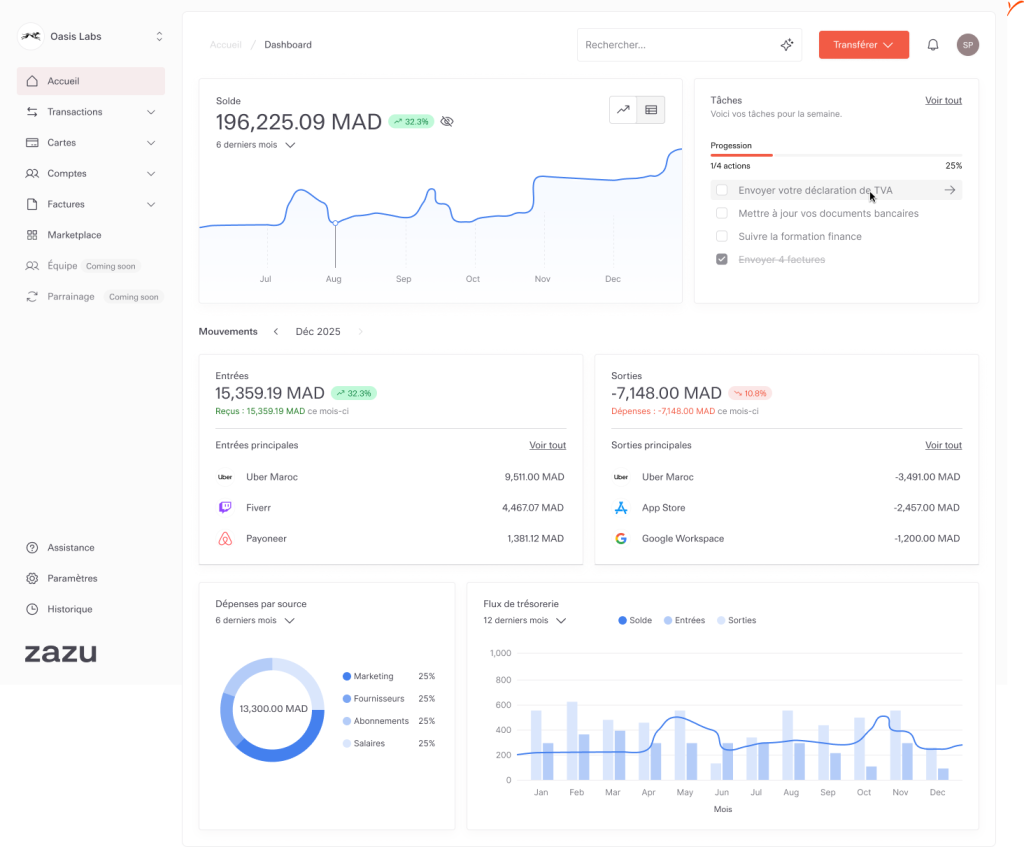

Zazu Dashboard; Image source: Zazu

The missing middle

Africa’s economic landscape is plagued by a persistent crisis known as the “missing middle.” At the bottom of the financing pyramid, micro-entrepreneurs are served by a robust network of microfinance institutions and mobile money agents. At the top, large conglomerates and multinationals receive premium service from banking partners.

Right at the centre of that pyramid, where the continent’s 50 million small and medium-sized enterprises (SMEs), which form the backbone of the economy, sit, a vacuum exists. Despite their contribution to the continent’s gross domestic product (GDP), these businesses face a funding gap estimated at over $330 billion. For the modern founder, this failure manifests as an administrative roadblock, as accessing financial services can expend time and resources.

“Traditional banks have very archaic measures and metrics about how they deal with and bank SMEs,” says Jacobs. “There is a big mismatch at the moment between the daily tools that SMEs are using versus the kind of tools that they’re using in their banking environment.”

From unbundling to rebundling

According to Jacobs, Africa’s fintech innovation has been defined by startups launching standalone apps for specific verticals like payroll, invoicing, lending, and commerce, forcing SMEs to manage their finances across fragmented dashboards. Zazu positions itself as a rebundled financial operating system for SMEs that offers the core utility of a bank, including accounts, cards, and transfers. Its ecosystem is built around API-driven integrations to connect first with finance tools, including bookkeeping, tax management, payroll, and cap-table management, before expanding into productivity suites such as e-commerce platforms, HR software, and CRMs.

At the foundation of Zazu’s offerings is the core banking stack designed for businesses and their staff. It allows businesses to create accounts that are separated by wallets, roles, spend limits, and the people who handle day-to-day operations. Rather than sharing a single corporate card, a business owner can instantly issue physical or virtual cards tailored to specific roles and contexts.

Crucially, Zazu also addresses the informal economy as it features a digital incorporation flow that helps unregistered businesses legalise their operations, ensure they can enter the formal banking system, and stay compliant with local regulations.

The platform also provides insights and data points that reveal a business’s cash flow, revenue trends, runway projections, and spending patterns. It also acts as an automated financial assistant that generates tasks and reminders for unpaid invoices or upcoming liabilities. Users can configure the system to automatically skim a percentage off every incoming invoice into a capital expenditure fund, ensuring that liquidity crises don’t ambush the business at the end of the fiscal year.

For business owners to understand how their businesses operate, Zazu also connects with accounting platforms and payment gateways through a unified interface that gives the business owner a real-time picture of their financial health.

Get The Best African Tech Newsletters In Your Inbox

Select your country Nigeria Ghana Kenya South Africa Egypt Morocco Tunisia Algeria Libya Sudan Ethiopia Somalia Djibouti Eritrea Uganda Tanzania Rwanda Burundi Democratic Republic of the Congo Republic of the Congo Central African Republic Chad Cameroon Gabon Equatorial Guinea São Tomé and Príncipe Angola Zambia Zimbabwe Botswana Namibia Lesotho Eswatini Mozambique Madagascar Mauritius Seychelles Comoros Cape Verde Guinea-Bissau Senegal The Gambia Guinea Sierra Leone Liberia Côte d'Ivoire Burkina Faso Mali Niger Benin Togo Other

Select your gender Male Female Others

Subscribe

Unlike some full-stack neobanks, Zazu is not pursuing banking licences. Instead, it operates a partnership-first model, working with regulated commercial banks in each market to handle compliance and reporting while Zazu focuses on third-party integrations, user experience, and the commercial layer.

In South Africa, Zazu works with a fully licenced commercial bank, while in Morocco, it partners with Chari, one of the first API-driven banking platforms operating under a payment licence.

The company runs a three-phased revenue generation model. It charges a monthly subscription fee for the platform bundle. Zazu will offer tiered pricing that will include a basic plan for freelancers and sole traders, along with Premium and Pro options for larger teams. These higher tiers will unlock advanced features like multi-accounts and AI-powered workflows. While final pricing is yet to be announced, the founders say it will be a more affordable alternative to traditional incumbents.

The platform also generates network revenue through card interchange fees and interest on deposits, and earns commission revenue through its marketplace, where third-party partners such as lenders or insurers pay a fee when Zazu customers use their services.

Africa’s SMEs rely on platforms like Kuda Business, TymeBank, FairMoney, and Bumpa that tackle parts of the SME workflow, including banking, inventory management, and credit. Zazu says its differentiation is its rebundled architecture: acting as a glue for banking features, rather than building each one internally, and its sole focus on businesses, not retailers. It says its integrations are already live with Paystack, Shopstar, Ozow, and over 20 ecosystem partners in South Africa and Morocco.

Zazu is already operational in Morocco and South Africa, with over 1,000 SME sign-ups for the waitlist and is currently in beta testing with over 50 SMEs. The startup has also secured recognition across global innovation circuits, including its selection into the Visa Accelerator Program.

With the pre-seed capital secured, Zazu is moving quickly to capitalise on its early traction. The company plans to open its seed round in early 2026 to support a broader pan-African expansion and the launch of new financial products tailored to entrepreneurs.

“We fully intend to be live in various countries and figure out the right way to plug those countries together and have a larger network of products that we can work with,” says Jacobs.

Disclaimer: The articles reposted on this site are sourced from public platforms and are provided for informational purposes only. They do not necessarily reflect the views of MEXC. All rights remain with the original authors. If you believe any content infringes on third-party rights, please contact crypto.news@mexc.com for removal. MEXC makes no guarantees regarding the accuracy, completeness, or timeliness of the content and is not responsible for any actions taken based on the information provided. The content does not constitute financial, legal, or other professional advice, nor should it be considered a recommendation or endorsement by MEXC.

Zazu Dashboard; Image source: Zazu

Zazu Dashboard; Image source: Zazu