A new clash has emerged between the crypto industry and Senator Elizabeth Warren over the approval of federal trust bank charters for several major digital asset firms, including Ripple.

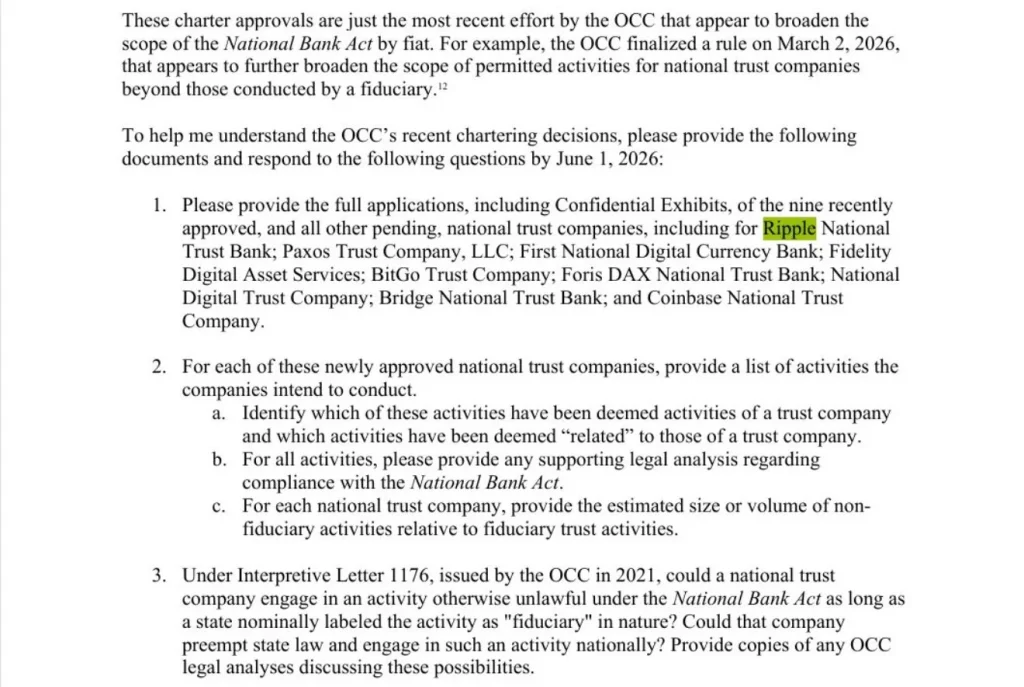

The debate began after Warren sent a letter to the Office of the Comptroller of the Currency (OCC), raising concerns that recently approved trust charters may not comply with the National Bank Act. Her criticism targeted crypto-focused companies such as Ripple, Circle, Paxos, BitGo, Coinbase, and Fidelity Digital Assets, which have either received conditional approvals or are seeking federally regulated trust bank status.

Warren argued that these firms appear to be engaging in activities similar to those of traditional banks without being held to the same regulatory standards. She also questioned whether some companies accelerated their charter applications following the passage of the GENIUS Act, which established a federal framework for stablecoin issuers.

Crypto Industry Defends OCC Decision

The crypto sector was quick to respond. Crypto Dyl News highlighted Warren’s reported request for Ripple to provide confidential documents related to its charter application, arguing that the move came after the OCC had already reached its decision. The post claimed Ripple’s approval marks an important step toward integrating the company and its XRP ecosystem into the U.S. financial system.

Support also came from The Digital Chamber, a crypto advocacy organization representing more than 250 industry participants. In a letter to OCC Comptroller Jonathan Gould, CEO Cody Carbone defended the regulator’s actions, arguing that Warren’s interpretation of banking law overlooks the OCC’s long-established authority to issue trust bank charters.

Carbone further noted that Congress recently created a regulatory pathway for stablecoin issuers through the GENIUS Act. He argued that it would be contradictory to establish such a framework while restricting the OCC from chartering firms intending to operate within it.

What Ripple’s Charter Means

The trust charters sought by companies like Ripple differ significantly from traditional banking licenses. While they would allow firms to custody customer assets under federal oversight, they would not permit them to accept deposits or issue loans like commercial banks.

For Ripple, securing such a charter could strengthen its standing within the U.S. financial system while bringing greater regulatory oversight to its services and stablecoin-related operations. The dispute underscores the broader debate over how digital asset companies should fit into the changing U.S. financial landscape.