Western Digital (WDC) Stock More Than Doubles in 2026 — Can It Keep Going?

TLDR

- Western Digital spun off its flash unit, SanDisk, in February 2025, making it a pure-play HDD company

- Fiscal Q3 revenue hit $3.34 billion, up 45% year-over-year, beating Wall Street estimates

- Q4 revenue forecast of ~$3.65 billion also came in above expectations

- Western Digital added $4 billion to its buyback program and raised $3.17 billion via a partial SanDisk stake sale to cut debt

- Analyst consensus is Moderate Buy, but the average price target of $450.46 sits below the current stock price

Western Digital’s Q3 revenue came in at $3.34 billion, up 45% year-over-year, with adjusted earnings of $2.72 per share — both ahead of Wall Street estimates.

Western Digital Corporation, WDC

The company then forecast Q4 revenue of around $3.65 billion, again beating expectations. Management pointed to strong demand for high-capacity storage products tied to AI infrastructure spending.

The stock had already more than doubled earlier in 2026 before the April earnings release.

Western Digital completed the spin-off of its flash business, SanDisk, in February 2025. That move left WDC as a more focused hard disk drive company targeting cloud, enterprise, and AI-related storage demand.

Before the split, investors had to weigh two businesses running on different cycles with different margin profiles. Cleaner structure, cleaner story.

AI Is Driving Storage, Not Just Compute

The AI buildout isn’t just buying GPUs. Companies scaling AI systems need storage for training data, video, archived content, and enterprise information — and that demand is showing up directly in HDD volumes.

In late April 2026, Seagate’s strong forecast helped lift the entire storage sector. Analysts following that report said HDD makers could maintain pricing power for years due to AI-driven demand. Western Digital sits right in the middle of that trend.

This isn’t a chip story. It’s the infrastructure around the chips — and right now that infrastructure is very busy.

Buybacks and Debt Reduction

Western Digital added $4 billion to its share repurchase program earlier this year after strong AI-related demand boosted storage sales.

The company also raised approximately $3.17 billion by selling part of its SanDisk stake, with proceeds earmarked for debt reduction. That’s a meaningful shift for a company that has historically carried a heavy debt load.

Historically viewed as a cyclical hardware name, WDC’s current capital allocation approach — buybacks plus debt paydown — is an attempt to reposition investor perception.

The analyst community currently sits at a Moderate Buy consensus: 1 strong buy, 18 buys, 3 holds, and zero sells, according to MarketBeat.

The average price target of $450.46 is now below the current stock price, meaning the rally has moved faster than analyst revisions.

That’s not a red flag on its own, but it does mean the stock is priced for execution, not just improvement.

The Q4 guidance of $3.65 billion is the next hard test. If demand holds, the bull case has legs. If cloud customers slow spending or pricing softens, the stock will feel it fast.

Western Digital’s average price target of $450.46 from analysts currently sits below the market price, with 18 of 22 analysts rating it a buy.

The post Western Digital (WDC) Stock More Than Doubles in 2026 — Can It Keep Going? appeared first on CoinCentral.

You May Also Like

BitGo Launches Stablecoin Minting and Redemption Service for Institutions

Hedera Price Prediction Holds Bullish as Iran Peace Deal Pushes Bitcoin Above $65,000 and Pepeto Presale Passes $10 Million

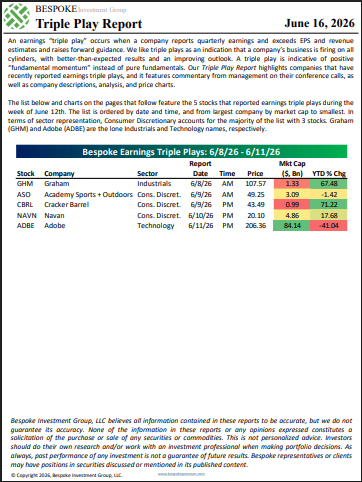

The Triple Play Report: 6/16/26