Palantir Is Down 26% in 2026 Despite a High-Conviction Upgrade. Is the Bottom Finally In?

The post Palantir Is Down 26% in 2026 Despite a High-Conviction Upgrade. Is the Bottom Finally In? appeared first on 24/7 Wall St..

- Palantir (PLTR) fell 3% to $130.86 Tuesday after Wolfe Research upgraded to Peer Perform from Underperform, with stock down 26% in 2026.

- Wolfe upgraded PLTR citing best product-market fit among enterprise software firms but maintained neutral stance due to elevated valuation at 142x P/E and 59x price-to-sales.

- Act now: the analyst who called NVIDIA in 2010 just named his top 10 AI stocks — and Palantir didn't make the cut. Grab the names FREE today.

Palantir (NASDAQ:PLTR) stock is sliding again Tuesday, down 3% at midday to $130 and change, even as a notable Wall Street rating change tries to pull the narrative the other way. The drop extends a brutal run that has Palantir stock down 26% in 2026.

The catalyst getting attention today: Wolfe Research upgraded Palantir to “Peer Perform” from “Underperform,” resuming coverage of one of the most polarizing names in enterprise AI. It’s an important reversal of a bearish stance, but it isn’t a Buy call.

That tension is the story. The bull case argues that the steep drawdown has reset expectations on a best-in-class operator. The bear case notes that Wolfe itself isn’t pounding the table, and PLTR stock is still falling on the day the upgrade was announced.

Wolfe Lifts Its Bearish Call With Limited Conviction

Wolfe Research’s qualitative read on the business is strikingly positive. The firm believes Palantir’s Artificial Intelligence Platform (AIP), ontology, and forward deployed engineers prove the company can turn AI interest into “scaled enterprise adoption.”

Wolfe went further, calling Palantir the best product-market fit of any enterprise software company in the market today, and tagging it as the most applied enterprise AI software company, with the largest and fastest growth rates in the industry. Those are unusually strong characterizations from a firm that had been bearish on the name.

The catch is the company’s valuation. Wolfe said Palantir’s current valuation already reflects much of its improved growth and margin outlook, which is why the rating tops out at neutral. Wolfe issued no Palantir stock price target, a meaningful tell about conviction.

Fundamentals Are Still Running Hot

The disconnect between PLTR stock and Palantir’s operating numbers is what makes the “bottom” debate worth having. Palantir’s Q1 2026 revenue grew 85% year over year (YoY) to $1.63 billion, with U.S. commercial revenue up 133%.

Moreover, Palantir’s management raised the company’s full-year 2026 revenue guidance to $7.65 to $7.66 billion. CEO Alex Karp asserted, “Palantir’s Rule of 40 score has soared to 145%… we are raising our full-year revenue guidance to 71% growth.”

However, the multiples remain demanding. Palantir stock carries a trailing P/E ratio of 142x and a forward P/E ratio of 88x, with a price-to-sales ratio near 59x. That’s the valuation caveat Wolfe flagged, in numerical terms.

Prediction Markets and Sentiment Are Cooler

If anyone needs a real-time gut check on the “is the bottom in” question, the prediction markets aren’t buying it yet. Polymarket traders pegged the probability of a down day for Palantir today at 0.971.

For Palantir stock in June, the modal outcome is a touch of $126 at 65% probability, with the upside tail to $168 or higher sitting near 5%. Insider activity is mixed too, with concentrated selling from senior executives on May 20 at prices in the $132 to $137 range.

What to Watch Next

The setup is genuinely two-sided. Palantir shares are well off the 52-week high of $207.52 and now trade below the 200-day moving average of $160.42, which the bulls can read as a reset and the bears can interpret as a broken trend.

The next scheduled catalyst is the Q3 2026 earnings report, expected August 3. Until then, follow-through on the Wolfe upgrade, any commentary from other research desks, and whether PLTR stock can hold the recent lows will shape the stock’s near-term direction.

Investors might consider watching for confirmation rather than chasing. Given the elevated multiples and the fact that even Palantir’s newest convert at Wolfe only went neutral, position sizing should stay modest on either side of the trade.

Act now: the analyst who called NVIDIA in 2010 just named his top 10 AI stocks — and Palantir didn’t make the cut. Grab the names FREE today.

The post Palantir Is Down 26% in 2026 Despite a High-Conviction Upgrade. Is the Bottom Finally In? appeared first on 24/7 Wall St..

You May Also Like

'Hypocrite': JD Vance gets more than he bargained for in testy appearance on ‘The View’

Hedera Price Prediction Holds Bullish as Iran Peace Deal Pushes Bitcoin Above $65,000 and Pepeto Presale Passes $10 Million

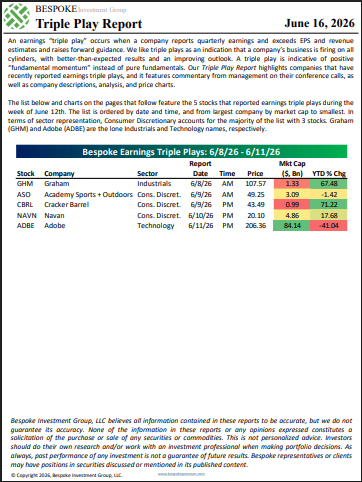

The Triple Play Report: 6/16/26