SPX Technologies Stock Is Up 56% in a Year, and the Data Center Story Is Just Getting Started

Key Takeaways for SPX Technologies Stock as of June 2026

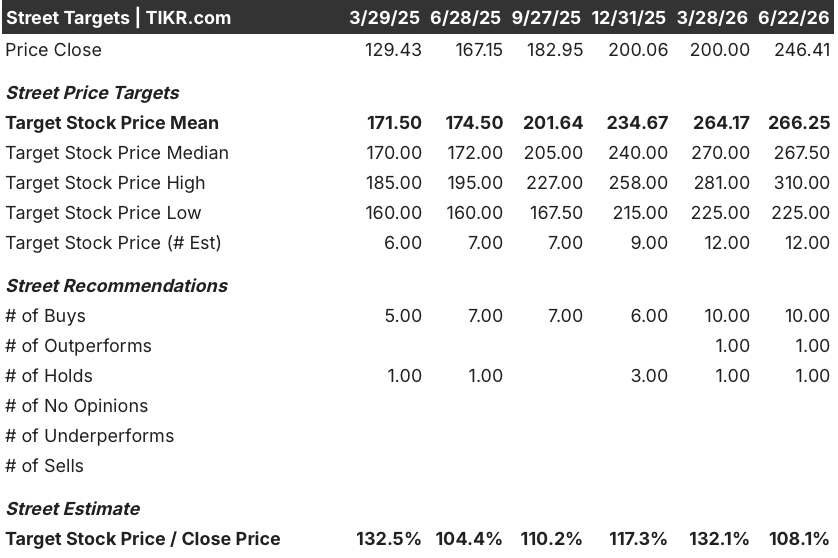

- Analysts rate SPX Technologies stock 10 Buys, 1 Outperform, and 1 Hold, with a street mean target of $266, implying 8% upside from the current price of $246.

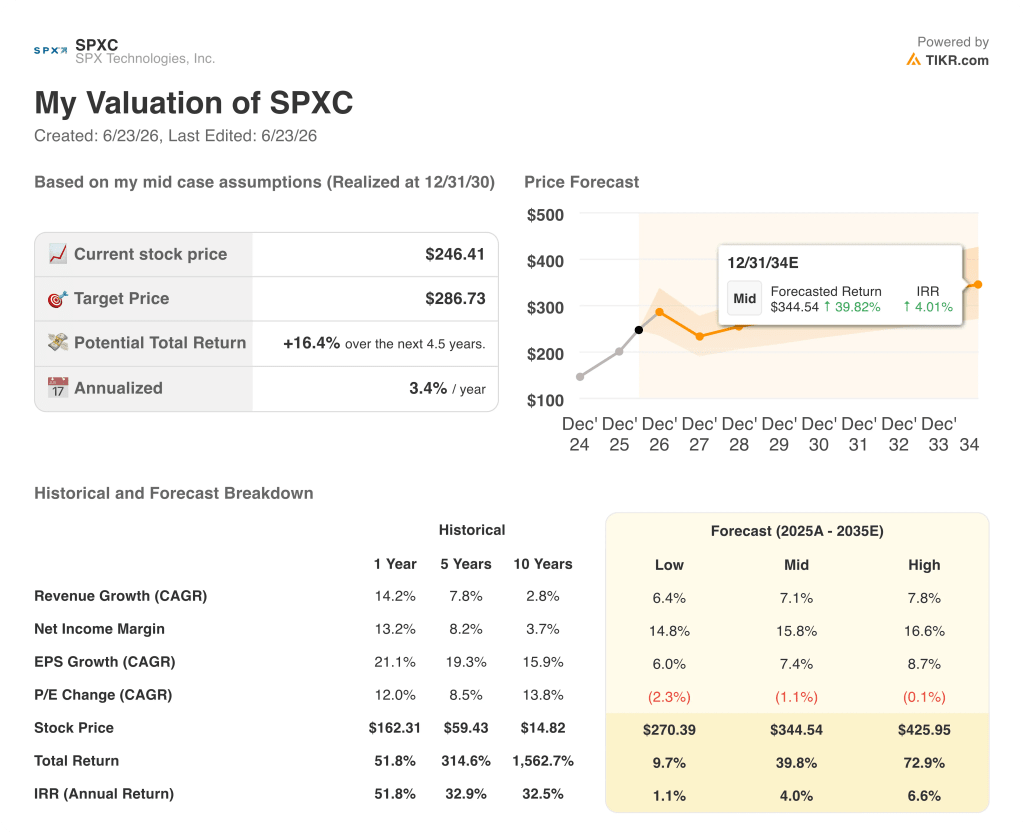

- TIKR’s mid-case model values SPX Technologies at $287 by December 2030, implying 16% total return from current levels, or 3% annualized.

- SPX Technologies delivered Q1 non-GAAP adjusted EPS of $1.69, beating the $1.56 estimate by 8%, while raising full-year guidance and accelerating data center cooling revenue from $200 million in 2025 to a guided $350 million in 2026.

Run the full SPXC estimates, analyst targets, and valuation model at your own pace. Explore SPXC stock data on TIKR for free →

SPX Technologies Beats Q1 on Revenue and EPS, Raises Guidance, and Lifts Data Center Revenue Target to $350 Million

SPXC Stock Q1 2026 Earnings in USD (TIKR)

SPXC Stock Q1 2026 Earnings in USD (TIKR)

SPX Technologies (SPXC) posted Q1 revenue of $566.8 million, beating the $557.6 million consensus by 2% and growing 17% year over year, while non-GAAP adjusted EPS of $1.69 came in above the $1.56 Street estimate for 22% growth on the same period last year.

The HVAC segment drove the top-line beat, growing revenue 22% year over year, with organic volume up 10% and inorganic growth from recent acquisitions contributing 11.5%, as data center cooling orders pushed management to lift the full-year data center revenue target from $300 million to $350 million, up from $200 million in fiscal 2025.

CEO Gene Lowe framed the runway without qualification on the Q1 earnings call: “We actually see some attractive runway looking ahead in ’27 and ’28. We think we have a really good customer mix here. We have a number of hyperscalers and colos. We have a good global presence here.”

The Detection and Measurement segment, which covers underground utility location technology, transportation software, and drone detection systems through the CommTech platform, contributed its own beat, with revenue up 8% year over year and segment margin expanding 410 basis points, driven by an expanded-scope software project in transportation that carried high variable margins.

HVAC backlog at quarter end reached $755 million, up 38% organically year over year, a figure management attributed directly to accelerating data center bookings.

SPX raised full-year adjusted EPS guidance to a midpoint of $7.95, up $0.15, citing Q1 outperformance in D&M and additional data center volume expected in H2, even while absorbing a $0.05 to $0.10 headwind from Section 232 tariffs on products manufactured in Canada.

Management guided Q2 HVAC revenue sequentially higher, signaling that data center demand continues to convert into backlog faster than current capacity can absorb it.

Track SPX Technologies stock’s data center backlog and HVAC revenue growth as the Q2 print approaches. Follow SPXC on TIKR for free →

Wall Street Sees 8% Upside at the Mean on SPXC Stock, With a $310 High Target That Prices In the Full Bull Case

Street Analysts Target for SPXC Stock (TIKR)

Street Analysts Target for SPXC Stock (TIKR)

SPX Technologies stock commands 10 Buy ratings and 1 Outperform against just 1 Hold among the 12 analysts covering it, with a street mean target of $266 and a street high of $310, a range that captures the full scope of the analyst debate from a conservative baseline priced near current levels to a scenario where capacity expansion and acquisitions drive a sustained re-rating.

SPXC Stock Revenue, EBITDA, EBITDA Margins and EPS Actuals & Estimates (TIKR)

SPXC Stock Revenue, EBITDA, EBITDA Margins and EPS Actuals & Estimates (TIKR)

Revenue is forecast to grow 16% in Q2 and 13% in Q3, extending the acceleration trend that produced 17% growth in Q1, and the EBITDA margin picture supports the quality of that growth, with consensus calling for Q3 EBITDA margins of 24%, up from 22.2% in Q1.

Non-GAAP adjusted EPS is estimated at $1.85 for Q2 and $2.10 for Q3, reflecting not just volume leverage but the incremental margin profile of HVAC’s engineered, configured-to-order model, where every contract gets priced in real time and gives management unusual pricing power against input cost inflation.

The D&M margin expansion carries its own weight in the bull case, with the segment printing 410 basis points of year-over-year margin improvement in Q1, and CFO Mark Carano confirmed at the Bank of America Industrials Conference in May that the team now runs at a structurally higher margin level than its own stated target range from prior years.

The open question the Street prices around is whether the data center capacity build across three facilities in Olathe, Tennessee, and Madison, Alabama will translate the $750 million of total stated capacity into booked revenue by 2027, or whether production ramp timing and tariff absorption create a gap before H2 2026 delivers the anticipated step-up.

Is SPXC Stock Undervalued in 2026? TIKR’s $287 Mid-Case Target Prices In a Modest Premium

TIKR’s mid-case values SPX Technologies at $287 by December 2030, implying 16% total return from the current price of $246, or 3% annualized over approximately 4.5 years.

SPXC Stock Valuation Model Results (TIKR)

SPXC Stock Valuation Model Results (TIKR)

The mid-case holds up when mapped to the dynamics already visible in the data. SPX Technologies stock is growing Q1 revenue 17% with EBITDA up 23%, holding HVAC backlog 38% above last year, and expanding D&M margins into a structurally higher band, all while deploying capital at an average pre-synergy acquisition multiple of around 11x with post-synergy costs averaging closer to 9x.

The 16% total return at the TIKR mid-case is modest in absolute terms, but it reflects a company trading close to its 52-week high of $248, with consensus already embedding strong data center revenue growth from an already-elevated 2025 base, making the upside pathway conditional on execution delivering at or above the guided $350 million data center figure.

SPX Technologies stock trades at a level where the announced capacity and current backlog are largely reflected in sell-side targets, and the street high of $310 captures what a bull outcome looks like if hyperscaler demand sustains 70% year-over-year growth through 2027 and the Madison facility hits full production on schedule.

See the full SPXC valuation model and stress-test your own assumptions. Build your SPXC thesis on TIKR for free →

Should You Invest in SPX Technologies, Inc.?

The only way to really know is to look at the numbers yourself. TIKR gives you free access to the same institutional-quality financial data that professional analysts use to answer exactly that question.

Pull up SPX Technologies, Inc. stock and you’ll see years of historical financials, what Wall Street analysts expect for revenue and earnings in the quarters ahead, how valuation multiples have moved over time, and whether price targets are trending up or down.

You can build a free watchlist to track SPX Technologies, Inc. alongside every other stock on your radar. No credit card required. Just the data you need to decide for yourself.

Access Professional Tools to Analyze SPXC stock on TIKR for Free →

You May Also Like

Bitcoin Drop Sparks $700M Liquidation Wave As Leverage Gets Flushed

A 68-Year-Old’s Roth Conversion Cost Him the $6,000 Senior Deduction That Was Shielding His Social Security

Datavault AI Expands WiSA Wireless Audio Technology Into Goldhorn Home Systems in China