Capital One Stock Is Down Nearly 20% in 2026: Is the Discover Integration Selloff an Opportunity?

Key Stats for Capital One:

- 52-Week Range: $178 to $261

- Current Price: $200.48

- Market Cap: ~$75 billion

- Street Mean Target: ~$257

- NTM P/E: ~10x

- LTM Net Debt/EBITDA: N/A (bank)

- Dividend Yield: ~1.6%

- Q1 2026 Adjusted EPS: $4.42

- Q1 2026 Pre-Provision Earnings: $6.8 billion (up 8% sequentially)

Now Live: Discover how much upside your favorite stocks could have using TIKR’s new Valuation Model (It’s free)>>>

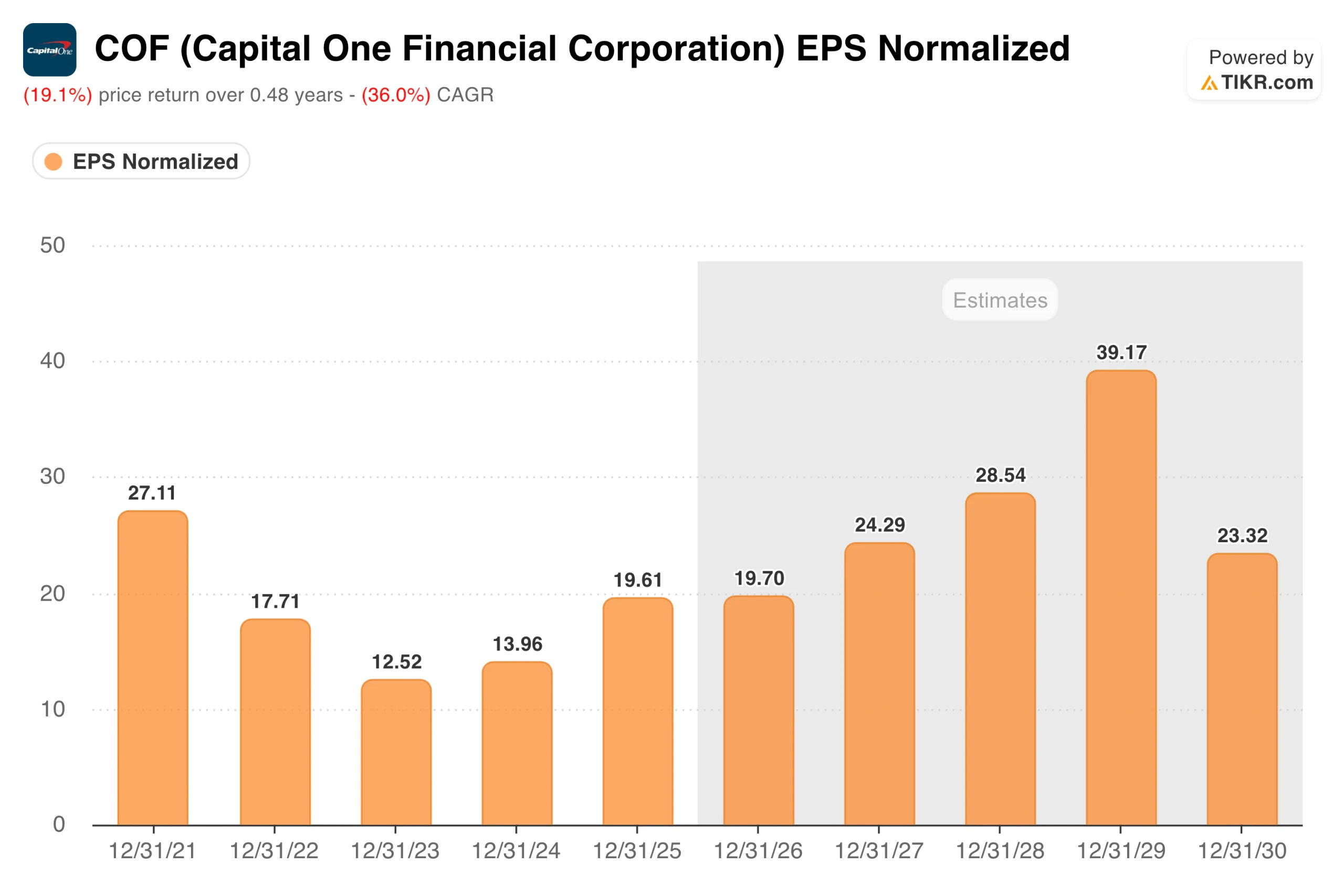

Capital One Earned $27 in 2021. Then It Fell to $12. Here Is What Happened Next

The EPS chart for Capital One Financial Corporation (COF) tells a story that requires some context to read correctly. Normalized earnings started at $27.11 in 2021, a figure inflated by pandemic-era reserve releases that flattered the whole banking industry.

As those tailwinds faded and credit costs normalized across the sector, earnings fell steadily to $12.52 in 2023. That was not deterioration in the business; it was the industry reverting to normal after an extraordinary period, and the distinction matters for how you interpret what came next.

Capital One EPS Normalized. (TIKR)

Capital One EPS Normalized. (TIKR)

From there, the recovery began. EPS climbed to $13.96 in 2024, then jumped to $19.61 in 2025 as the $35.3 billion Discover Financial Services acquisition closed, and the combined entity began generating earnings at scale.

The deal transformed Capital One into the largest credit card issuer in the United States by loan volume. The consensus now projects continued acceleration: around $20 in 2026, building toward roughly $24 in 2027 and around $29 in 2028. CEO Richard Fairbank said on the Q1 2026 call that “the Discover integration continues to go well and we continue to build momentum from this game-changing acquisition.”

Adjusted EPS came in at $4.42 for the quarter, ahead of the prior year period, and pre-provision earnings grew 8% sequentially to $6.8 billion.

See analysts’ growth forecasts and price targets for Capital One stock (It’s free) >>>

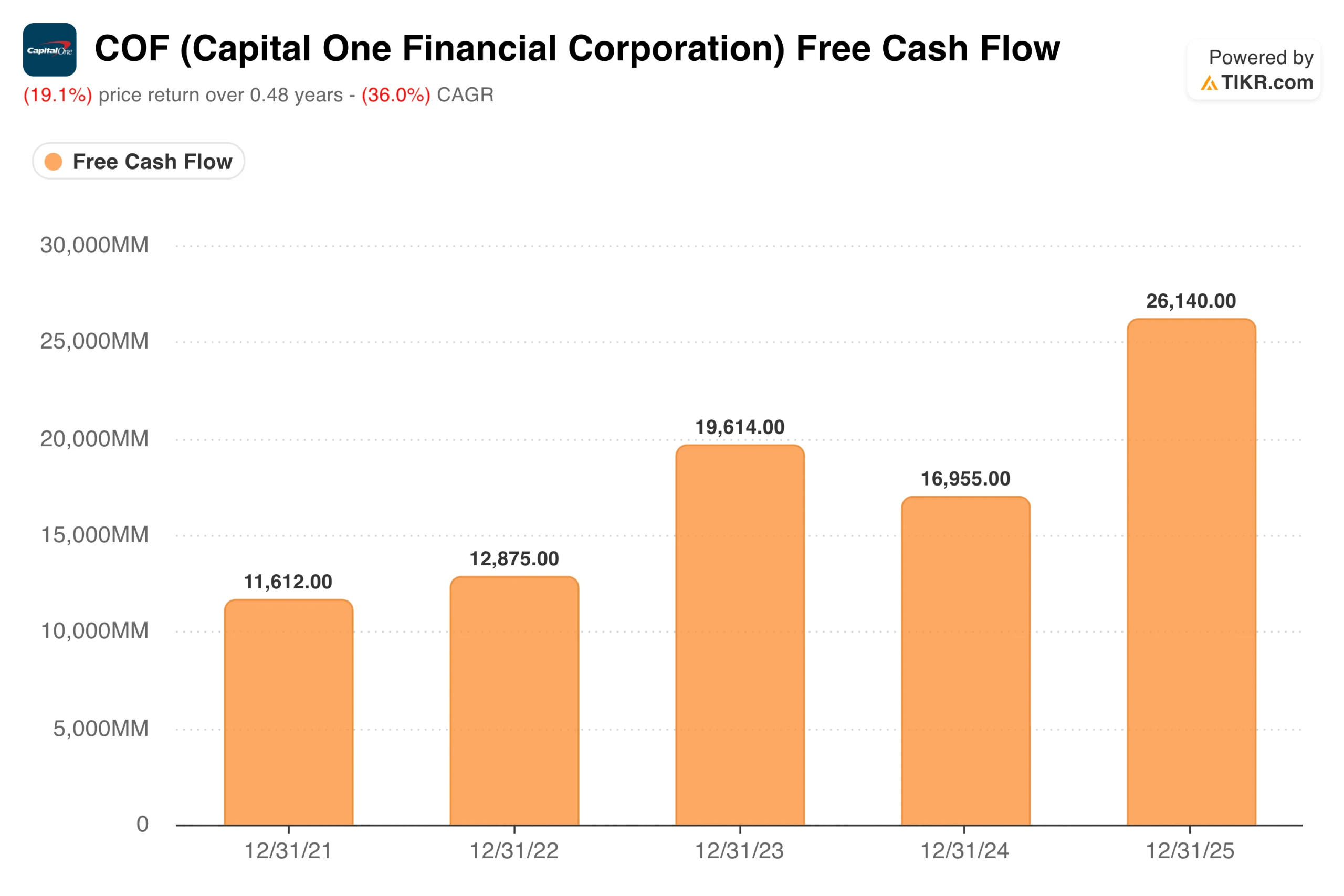

The Discover Deal Pushed Free Cash Flow to $26 Billion. The Migration Work Starts Now

The free cash flow chart captures the scale of what the Discover combination created. Capital One generated $11.6 billion in free cash flow in 2021, grew to $19.6 billion in 2023, dipped to $17.0 billion in 2024 as integration costs weighed on results, and then surged to $26.1 billion in 2025 as the combined business began operating.

That is a meaningful step up in cash generation, and it occurred before the bulk of the planned synergies were realized.

Capital One Free Cash Flow. (TIKR)

Capital One Free Cash Flow. (TIKR)

What the market is focused on now is whether that cash generation holds through the most operationally complex phase of the integration.

Capital One is migrating Discover’s card portfolio onto its own technology systems starting late 2026, with full conversion expected by early 2027. The company also closed its $5.15 billion acquisition of Brex in early 2026, adding a commercial payments business to the mix.

Running two integrations simultaneously has made investors nervous, which explains much of the year-to-date selloff.

The strategic logic underneath the complexity is real: by owning the Discover network, Capital One now captures interchange fees it previously paid to Visa and Mastercard. The company is targeting $2.7 billion in pre-tax synergies by 2027.

Access Professional Tools to Analyze COF stock on TIKR for Free →

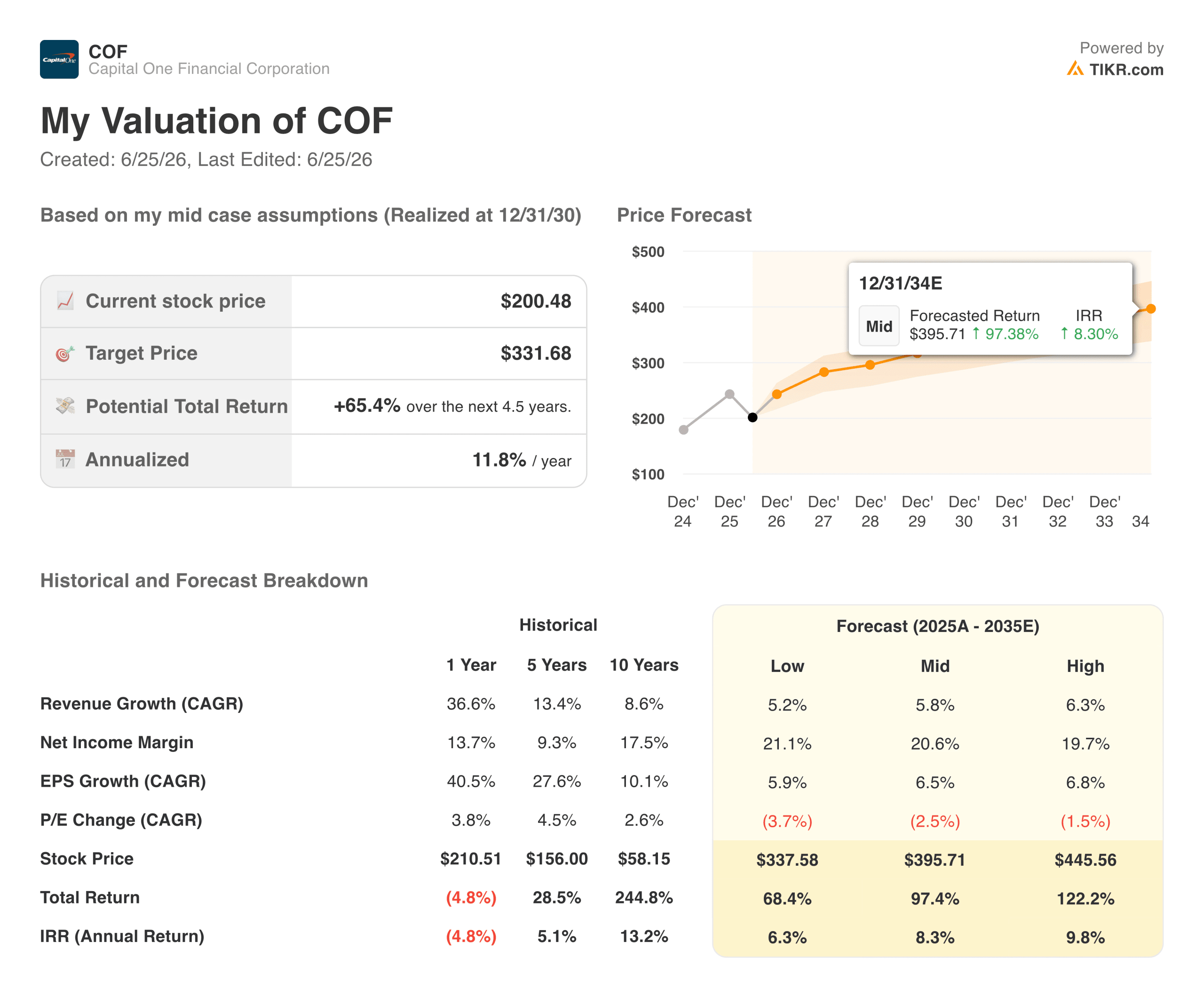

What the TIKR Model Says About the Gap Between Price and Value

The stock’s year-to-date decline has created a setup that the TIKR model finds compelling. At $200.48, the mid-case target of around $332 implies roughly 65% total return, or about 12% annualized over the next 4.5 years.

The model assumes around 6% annual revenue growth and net income margins near 21%, neither of which requires the Discover synergies to fully materialize.

Capital One Valuation Model. (TIKR)

Capital One Valuation Model. (TIKR)

The high case reaches around $446, implying total returns above 120%. The low case lands near $338, still well above the current price. The Street mean target sits around $257, implying about 28% upside from here, suggesting the analyst community broadly views the selloff as an overreaction to near-term execution risk.

The bear case is real: credit quality deteriorates further, integration costs overrun budget, and proposed interest-rate cap legislation creates margin pressure on a business that serves a significant share of middle-market borrowers.

The bull case is that a company generating $26 billion in free cash flow and building toward a closed-loop payments network is trading at roughly 10x forward earnings, a multiple that implies almost no realization of synergies.

Should You Invest in Capital One Financial Corporation?

The investment case for Capital One today is essentially a bet on execution.

The business is large, cash-generative, and trading at a below-market multiple relative to its current earnings. If the Discover integration proceeds on schedule and the $2.7 billion synergy target comes through by 2027, the current price will look like a clear discount in hindsight.

The risk is that two simultaneous integrations, credit normalization pressure, and a difficult regulatory environment combine to delay that timeline. Investors with a two- to three-year horizon and tolerance for that uncertainty are looking at a setup that the numbers suggest is more of an opportunity than a threat.

Build your own Valuation Model to value any stock (It’s free!) >>>

Looking for New Opportunities?

- See what stocks billionaire investors are buying so you can follow the smart money.

- Analyze stocks in as little as 5 minutes with TIKR’s all-in-one, easy-to-use platform.

- The more rocks you overturn… the more opportunities you’ll uncover. Search 100K+ global stocks, global top investor holdings, and more with TIKR.

Disclaimer:

Please note that the articles on TIKR are not intended to serve as investment or financial advice from TIKR or our content team, nor are they recommendations to buy or sell any stocks. We create our content based on TIKR Terminal’s investment data and analysts’ estimates. Our analysis might not include recent company news or important updates. TIKR has no position in any stocks mentioned. Thank you for reading, and happy investing!

You May Also Like

Justice Department has 'gone off the rails' for Trump's 'pretzel logic': analysis

Pi Network Faces Centralization Debate as Community Questions Pi2Day Direction

Strategy MSTR Crashes 83%, STRC All-Time Low: Will Saylor Sell Bitcoin

Trending News

More24/7 Live News

MoreQuick Reads

More