Atlassian Stock Fell 8% in a Day. Here’s Where TEAM Could Go in 2026

Key Stats for Atlassian Stock

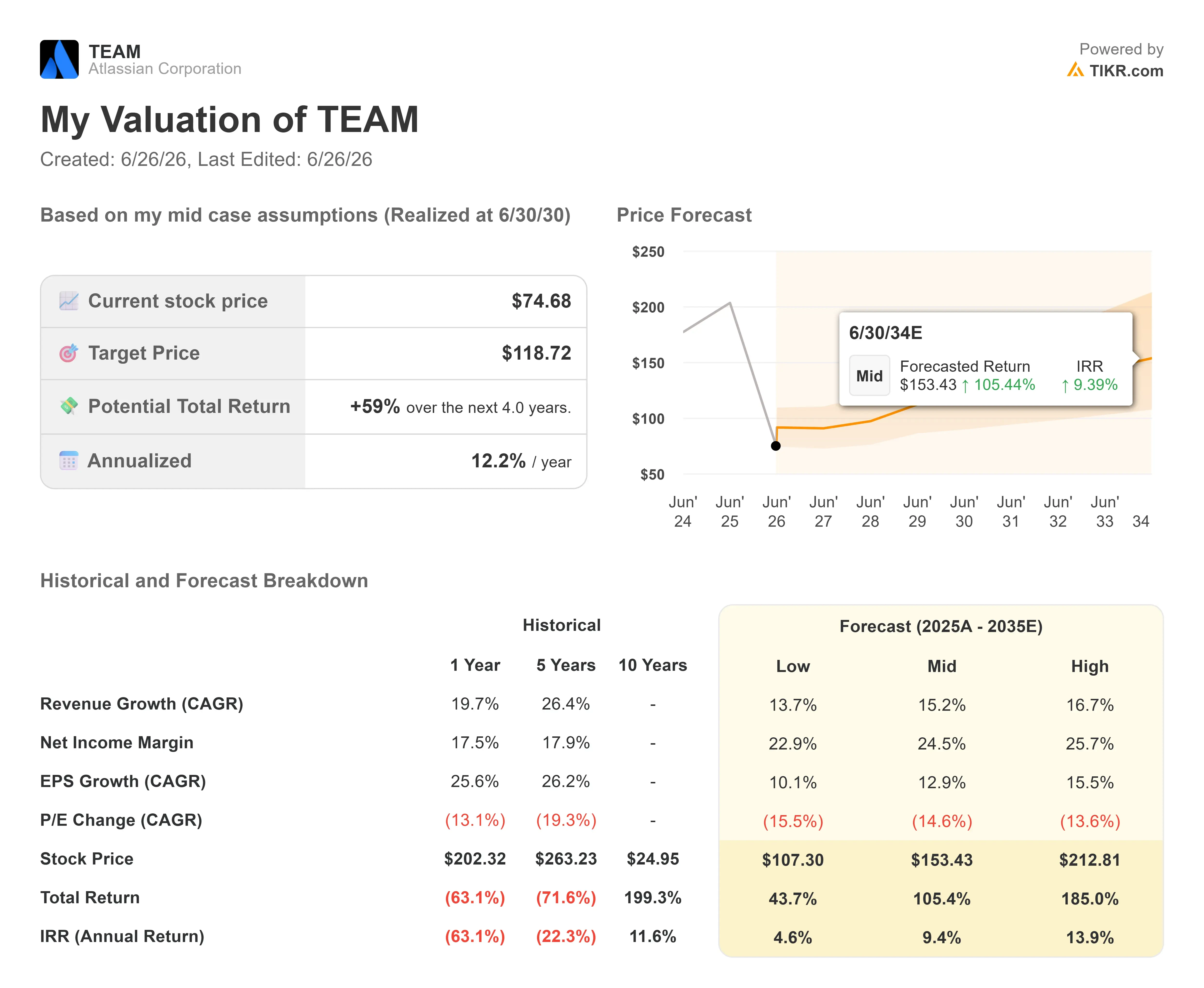

- Current Price: $74.68

- TIKR Target Price (Mid): ~$119

- Street Target (Mean): ~$140

- Potential Total Return (Mid): ~59%

- Annualized IRR (Mid): ~12% / year

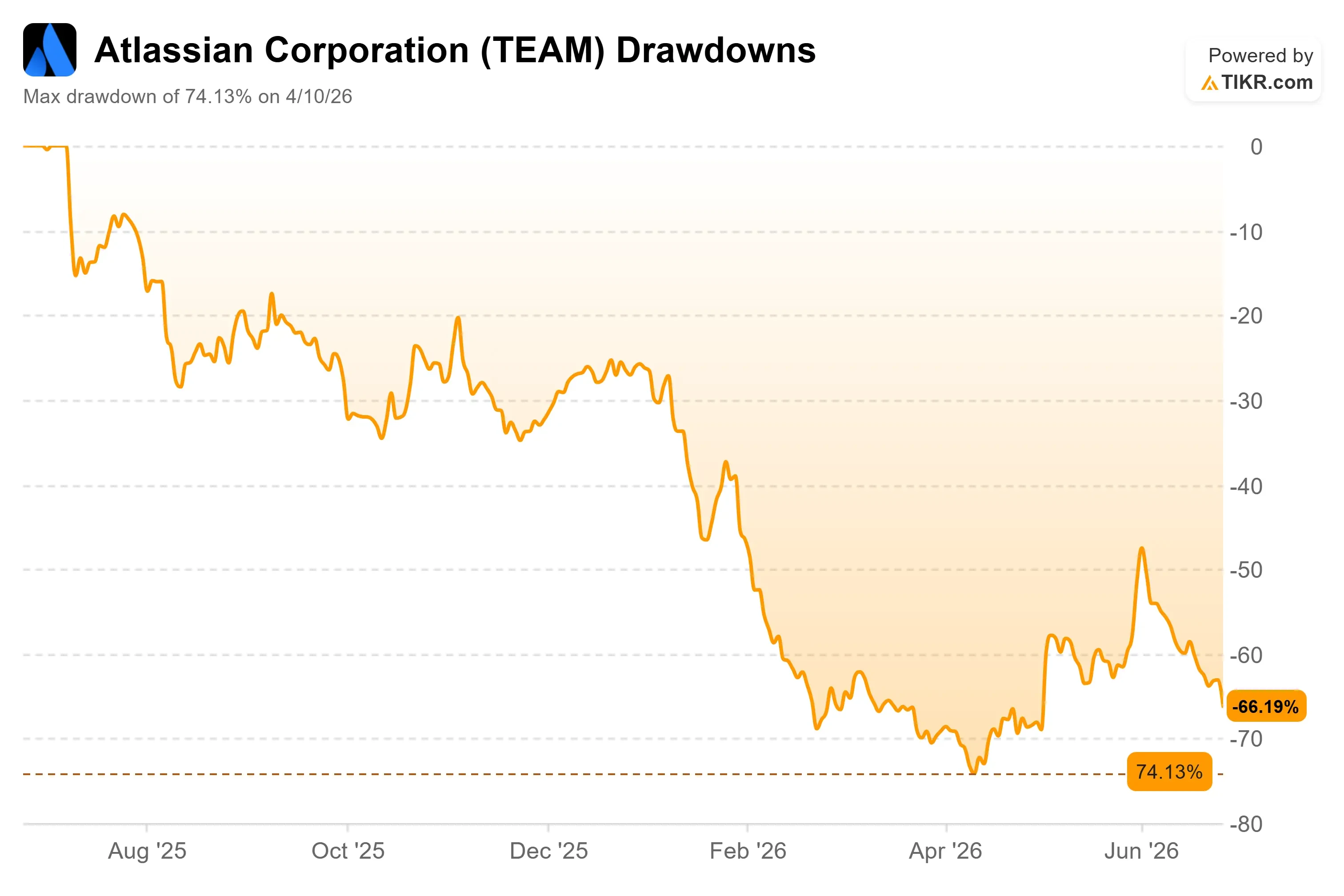

- Max Drawdown: 74.13% (April 10, 2026)

Now Live: Discover how much upside your favorite stocks could have using TIKR’s new Valuation Model (It’s free) >>>

Why Did Atlassian Stock Fall?

Atlassian (TEAM) closed at $74.68 on June 25, down 8.42% on the day, and almost none of it was the company’s fault. There was no guidance cut, no downgrade, no product stumble. The stock got caught in a broad software and AI selloff as investors took profits and repriced stretched tech valuations. For a stock already near its 52-week low of $56.01, the timing stung.

That is the tension worth sitting with. Atlassian sits 74% below its peak, yet it just delivered the best operational quarter in its history. The market is treating a business that is accelerating as if it were breaking. The question for investors is simple: is the fear about the company, or about the category it lives in?

The category fear has a name. The “SaaSpocalypse,” meaning the 2026 selloff in subscription-software stocks on worries that AI agents will replace per-seat licenses, has hammered every name that charges by the user. Atlassian sits squarely in the blast radius.

Atlassian Drawdowns (TIKR)

Atlassian Drawdowns (TIKR)

See historical and forward estimates for Atlassian stock (It’s free!) >>>

A Quarter That Argued the Opposite

In its fiscal Q3 2026 report, Atlassian posted revenue of $1,786.97 million, beating consensus by 5.24%, and the stock jumped 29.58% in reaction. Then the broader software tape clawed most of it back.

The bear thesis is that AI replaces the seats Atlassian sells. The quarter said the opposite. Customers added users, and the seat-based model kept compounding. Martin Lam, who runs investor relations at Atlassian, said at the Mizuho Technology Conference on June 10 that cloud strength came from cross-sell into the Teamwork Collection bundle and “seat expansion within core Jira.” Seat durability is the exact thing bears say AI should destroy.

The counterargument to AI disruption is a product, not a slogan. Lam pointed to the Teamwork Graph, the knowledge layer that maps who works on what across an organization. In a company demo, the same coding prompt connected to that graph delivered “48% better results at 44% less token usage.” The pitch: AI without organizational context is weaker, and Atlassian owns the context. Its Rovo assistant now tops 5 million monthly active users, with credit consumption growing 20% month over month.

Where the Risk Still Lives

Atlassian is not cheap on conventional earnings. It trades at an LTM P/E near 90x because GAAP profit is thin, weighed down by stock-based compensation management, which has been flagged to moderate. On a forward free cash flow basis, it looks far more reasonable, near 9x NTM market cap to free cash flow against about $2.04 billion in expected NTM levered free cash flow.

Against peers, the discount is hard to ignore. Atlassian trades at an NTM EV/EBITDA of 9.2x, below the software peer mean of 13.3x and median of 10.7x, with ServiceNow at 13.8x and Salesforce at 8.9x. A company growing high-teens to low-20s on revenue priced under most slower-growing peers points to an AI-disruption discount, not a fundamentals one. Whether that discount is fair is the whole debate.

The genuine risk is the data center business. It faces negative growth next year as accounting changes pull license revenue forward and the product moves toward its March 2029 end of life. That is why management introduced subscription ARR, meaning annual recurring revenue, as a cleaner gauge of the book. It has accelerated from 20% to 23% over the last three disclosed quarters.

Atlassian Beats & Misses (TIKR)

Atlassian Beats & Misses (TIKR)

See how Atlassian performs against its peers in TIKR (It’s free!) >>>

TIKR Advanced Model Analysis

- Current Price: $74.68

- Target Price (Mid): ~$119

- Potential Total Return: ~59%

- Annualized IRR: ~12% / year

Atlassian Advanced Valuation Model (TIKR)

Atlassian Advanced Valuation Model (TIKR)

See analysts’ growth forecasts and price targets for Visa Inc. stock (It’s free!) >>>

Two revenue drivers anchor the mid case: seat expansion in core Jira and cross-sell into the higher-priced Teamwork and Service collections, where Jira Service Management is now a $1 billion-plus ARR business growing over 30%. The margin driver is operating leverage as R&D and headcount growth moderate, lifting net income margin toward the model’s 24.5% mid-case. The primary risk is that AI compresses seat demand faster than cross-sell and Rovo can offset.

If migrations and AI monetization land, the high case points to roughly $213 by mid-2030, near a 14% IRR. If the data center drag deepens and seat growth stalls, the low case sits near $107, above today’s price, but a far thinner return.

Conclusion

The next real test is fiscal Q4 earnings on August 6. Watch subscription ARR. Holding at or above 23% would confirm the underlying book is accelerating regardless of data center noise, making the June selloff look like sentiment. Slipping toward 20% or below, with soft cloud guidance, would hand bears their first real evidence that AI is reaching the seats. Until then, the stock trades on fear that its own numbers keep contradicting.

See what stocks billionaire investors are buying so you can follow the smart money with TIKR.

Should You Invest in Atlassian?

The only way to really know is to look at the numbers yourself. TIKR gives you free access to the same institutional-quality financial data that professional analysts use to answer exactly that question.

Pull up Atlassian, and you’ll see years of historical financials, what Wall Street analysts expect for revenue and earnings in the quarters ahead, how valuation multiples have moved over time, and whether price targets are trending up or down.

You can build a free watchlist to track Atlassian alongside every other stock on your radar. No credit card required. Just the data you need to decide for yourself.

Analyze Atlassian on TIKR Free →

Looking for New Opportunities?

- See what stocks billionaire investors are buying so you can follow the smart money.

- Analyze stocks in as little as 5 minutes with TIKR’s all-in-one, easy-to-use platform.

- The more rocks you overturn… the more opportunities you’ll uncover. Search 100K+ global stocks, global top investor holdings, and more with TIKR.

Disclaimer:

Please note that the articles on TIKR are not intended to serve as investment or financial advice from TIKR or our content team, nor are they recommendations to buy or sell any stocks. We create our content based on TIKR Terminal’s investment data and analysts’ estimates. Our analysis might not include recent company news or important updates. TIKR has no position in any stocks mentioned. Thank you for reading, and happy investing!

You May Also Like

Why The Green Bay Packers Must Take The Cleveland Browns Seriously — As Hard As That Might Be

Luck, Stupidity, and Getting Ripped Off

Why an Altcoin Rally Could Start When Everything Still Looks Terrible