Must Read

If the GCash IPO merely rotates domestic funds among existing listed companies, the success will be more symbolic than transformativeIf the GCash IPO merely rotates domestic funds among existing listed companies, the success will be more symbolic than transformative

[Vantage Point] Can the market handle GCash?

For feedback or concerns regarding this content, please contact us at crypto.news@mexc.com

GCash has already proven it can redefine digital finance. But is the Philippine Stock Exchange ready for it? A P470-billion IPO would test the market’s liquidity, depth and ability to attract fresh capital — making the listing not just a milestone for fintech, but a referendum on the maturity of the country’s capital market.

GCash’s proposed initial public offering (IPO) won’t just be memorable for the billions of pesos it plans to raise.

Instead, it will be a referendum on the maturity of the Philippine capital market itself. A success would mean that the Philippine Stock Exchange (PSE) has finally put depth in place to bankroll world-class technology companies. But if it fails, it will reveal a structural weakness that investors have long remained quietly cognizant of: the country’s equity market remains too small and too illiquid to support companies that have already outgrown it.

Why? Vantage Point considers GCash as something of a unique listing. Since its inception in 2004 as a text-based money-transfer service, it has grown to become the country’s dominant digital financial platform with about 94 million registered users.

It now offers payments, money transfers, savings, lending, insurance, investments and even stock trading — making it one of Southeast Asia’s few genuine financial super applications. Public records reveal that its parent Mynt is aiming for a valuation of at least $8 billion, or roughly P470 billion, while raising about $1 billion through the offering.

GCash has become consistently profitable, while its earnings contribution to Globe Telecom has grown rapidly over the past several years. Investors are thus not just purchasing a payments company. They are buying a platform whose future increasingly relies on consumer finance, wealth management, and digital banking.

But not all outstanding companies make an outstanding IPO. A vital issue is whether the Philippine capital market has the capacity to accommodate a company of this size without disrupting the rest of the exchange.

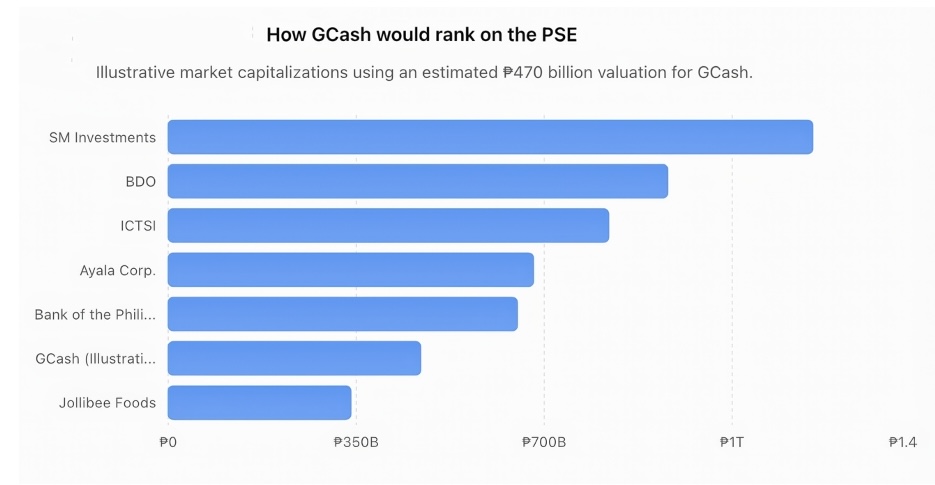

At a valuation approaching half a trillion pesos, GCash would quickly rank as one of the country’s biggest listed companies. It would compete with businesses that have spent decades constructing banks, power plants, property portfolios, and infrastructure assets. Unlike those traditional companies, however, GCash’s valuation rests primarily on future growth rather than accumulated physical assets.

GCash would debut among the country’s corporate giants despite having virtually no legacy physical assets.

This immediately begs the liquidity question. The PSE remains one of Asia’s illiquid markets. Daily trading activity remains concentrated in a limited number of blue-chip stocks, with foreign investors being one of the most significant net sellers in recent years. (READ: [Vantage Point] PSE’s Monzon years: Rearranging the plumbing while the house burns)

Finite pools of capital are held by domestic pension funds, insurance companies, and mutual funds. Unless the IPO raises substantial new foreign funds, demand for GCash shares is likely to originate from investors selling existing investments.

An IPO, after all, creates no liquidity. It just reallocates existing funds unless entirely new capital enters the market. That possibility should concern existing listed companies. A successful GCash listing could broaden investor choice, but it could also divert scarce investment capital away from Philippine corporations already competing for limited liquidity. Ironically, the more attractive the GCash story becomes, the greater the potential rotation from established blue chips.

Valuation presents another challenge.

An $8 billion valuation means that investors have paid an extraordinarily high premium for future earnings growth. In venture capital, such multiples are common since investors tend to buy optionality and disruptive potential.

Public markets are a different ballgame.

Every quarter is a report card that measures whether real earnings meet high expectations. And that’s exactly why the actual investment case isn’t in payments but in monetization. Payments businesses process enormous transaction volumes while earning relatively thin margins.

Real profits come from higher value-added operations such as consumer lending, insurance distribution, investment products, and merchant financing. GCash has cleverly diversified into all these offerings, transforming from a mere e-wallet into a strong digital financial ecosystem.

Its recent move to introduce fees for selected cash-in transactions illustrates this transition. Investors welcome recurring fee income because it diversifies revenues beyond transaction processing. But monetization also carries risk. Consumers have become accustomed to free digital services, while competitors such as Maya, traditional banks and future financial technology (fintech) entrants remain capable of competing aggressively on price. Network effects are powerful, but they are rarely permanent.

Investors should also not mistake registered users for economic value. Although 94 million users represent extraordinary reach, future growth cannot rely indefinitely on adding new accounts. The Philippines has finite demographics. The next stage, therefore, is to make more money off existing customers by cross-selling financial products. That approach promises higher margins for GCash, but also subjects it to greater credit risk, regulatory oversight, and operational challenges.

In many respects, turning into a financial super app also means becoming a financial institution. However, some of the most compelling arguments for the IPO go beyond GCash itself.

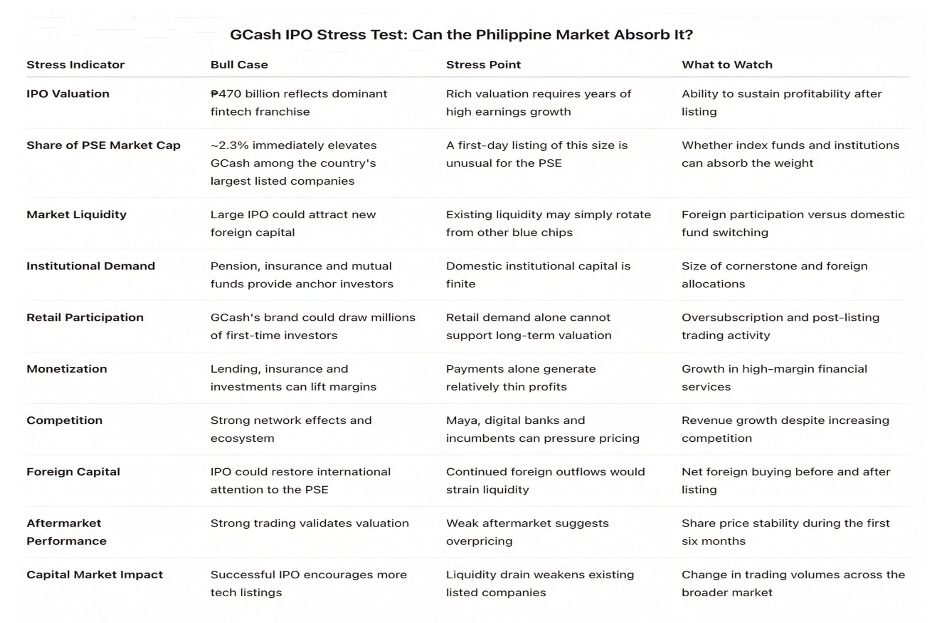

This table reinforces our central thesis: the GCash IPO is not merely a valuation exercise —it is a stress test of the Philippine capital market.

This table reinforces our central thesis: the GCash IPO is not merely a valuation exercise —it is a stress test of the Philippine capital market.

For decades, critics have argued that the Philippine capital market has failed to nurture globally competitive technology companies. A successful domestic listing by GCash would signal that the market is finally evolving beyond its traditional dependence on banks, property developers, and holding companies. It could encourage other high-growth technology firms to list locally rather than seek foreign exchanges with deeper liquidity.

But confidence alone cannot substitute for market depth.

If GCash attracts meaningful foreign participation, trades actively, and expands the pool of investment capital available to Philippine equities, it may well become the defining transaction that modernizes the country’s capital market.

If, however, the offering merely rotates domestic funds among existing listed companies, the success will be more symbolic than transformative.

Ultimately, this IPO is not simply about financial technology. It is about whether the PSE has matured enough to support the country’s next generation of technology champions, while ensuring the broader equity market retains sufficient liquidity.

GCash has already proven that it deserves a place among the nation’s leading companies. The larger question is whether the Philippine capital market is finally prepared to deserve it. – Rappler.com

We draw our analysis from public disclosures and market data from Globe Telecom’s annual reports and regulatory filings, Mynt and GCash corporate announcements, Philippine Stock Exchange (PSE) market statistics and listed company data, and on Mynt’s proposed initial public offering (IPO) valuation and fundraising plans. Market capitalization rankings, comparative valuations, liquidity observations, and stress-test calculations were derived from the latest available PSE data and company disclosures.

Here are other Vantage Point articles you may have missed:

Click here for other Vantage Point articles.

Disclaimer: The articles reposted on this site are sourced from public platforms and are provided for informational purposes only. They do not necessarily reflect the views of MEXC. All rights remain with the original authors. If you believe any content infringes on third-party rights, please contact crypto.news@mexc.com for removal. MEXC makes no guarantees regarding the accuracy, completeness, or timeliness of the content and is not responsible for any actions taken based on the information provided. The content does not constitute financial, legal, or other professional advice, nor should it be considered a recommendation or endorsement by MEXC.

You May Also Like

Fed Governor Calls For Strong Stablecoin Oversight As CLARITY Act’s Final Text Gets Delayed

US Federal Reserve (Fed) Governor has warned about the potential risks that stablecoin may pose to financial stability and urged for strong oversight, as the industry

Share

Bitcoinist2026/04/02 18:00

Global FinTech and the Future of Programmable Money

Money has been changing all along in human history. Every change, from physical coins and paper money to digital banking and mobile payments, has altered the way

Share

Globalfintechseries2026/06/29 15:22

XRP Price: World’s Highest IQ Holder Says the Supercycle Is Just Starting — Analysts Weigh In

TLDR YoungHoon Kim, the world’s verified highest IQ holder (276), publicly stated the XRP Supercycle is just beginning Three technical and on-chain signals have

Share

Coincentral2026/06/29 14:59