Adobe Stock is Trading Near 52-Week Low: Here’s Where Shares Could Go in 2026

Key Takeaways for Adobe Stock as of June 2026

- Analysts rate Adobe stock 9 buys, 2 outperforms, 24 holds, and 3 sells with a mean target of $282, implying around 39% upside from the current price of $203.

- TIKR’s mid-case model values Adobe at around $350 by November 2030, implying around 73% total return, or roughly 13% annualized.

- AI-first annualized recurring revenue tripled year over year to exceed $500 million, while creative freemium monthly active users surged over 70% year over year to 90 million.

Adobe stock sits near a 52-week low of $190 despite a $167 million revenue beat and a full-year guidance raise. See how the data compares to Street targets on TIKR for free →

Adobe Beats Revenue Estimates but Freemium Pivot and Leadership Exits Hit ADBE Stock

Adobe (ADBE), the creative and digital experience

ADBE Stock Q2 2026 Earnings in USD (TIKR)

ADBE Stock Q2 2026 Earnings in USD (TIKR)

software company, posted record Q2 fiscal 2026 revenue of $6.62 billion, following $6.40 billion in Q1, growing 13% year over year and clearing the consensus estimate of $6.45 billion by $167 million.

The Q2 result prompted management to raise full-year revenue guidance to $26.5 billion to $26.6 billion and set a Q3 target of $6.67 billion to $6.72 billion.

That growth came from subscription momentum across all three customer groups. Business Professionals and Consumers subscription revenue reached $1.85 billion, growing 16% year over year, while Creative and Marketing Professionals subscription revenue hit $4.54 billion, growing 13% year over year.

Addressing the AI engine driving both segments on the Q2 fiscal 2026 earnings call, CEO Shantanu Narayen stated: “Adobe’s AI innovation has driven an impressive 3x year-over-year increase in AI first ARR to greater than $500 million.” That momentum extended to Firefly, where annualized recurring revenue approached $300 million exiting Q2, growing approximately 50% quarter over quarter through apps and credit packs.

Creative freemium monthly active users also crossed 90 million in Q2, growing over 70% year over year.

The bigger story, though, is a strategic pivot creating near-term ARR pressure. Adobe will defer previously planned Creative Cloud second-half price increases and aggressively expand its freemium offering through Firefly and Acrobat. Narayen told analysts roughly half of the reduced ARR growth expectation traces to the deferred price increase, with the other half from accelerating freemium expansion.

The quarter also carried leadership uncertainty. CFO Dan Durn announced his departure effective June 15, with Senior Vice President Steve Day serving as interim CFO. That exit follows CEO Narayen’s earlier decision to transition to Board Chair, leaving Adobe’s next leadership chapter unsettled during a critical strategic shift.

What that means for investors is a stock near its 52-week low of $190, down around 40% year to date, and trading at roughly 8x forward earnings compared with 11x on early June. Even so, Adobe raised full-year revenue guidance to $26.5 billion to $26.6 billion and targeted Q3 revenue of $6.67 billion to $6.72 billion.

Adobe’s freemium pivot raised the revenue ceiling while pressuring near-term ARR. Pull the full forward model alongside management’s guidance on TIKR for free →

Wall Street Holds Adobe Stock as 12 Analyst Downgrades Follow the Q2 Report

Street Analysts Target for ADBE Stock (TIKR)

Street Analysts Target for ADBE Stock (TIKR)

Wall Street holds a cautious stance on Adobe stock, with 9 buys, 2 outperforms, 24 holds, and 3 sells across the analyst coverage base. The mean price target of $282 implies around 39% upside from the current price of around $203, though at least 12 brokerages cut their targets following the Q2 earnings report.

Those cuts cited the CFO departure and near-term ARR headwinds as primary drivers. The median target of $250 and a high estimate of $460 signal wide dispersion in how the Street is pricing Adobe’s freemium transition.

Wall Street Expects Adobe Revenue Growth Above 8% Through Fiscal 2027 as ADBE Stock Trades Near a 52-Week Low

ADBE Stock Revenue Actuals & Estimates (TIKR)

ADBE Stock Revenue Actuals & Estimates (TIKR)

For Q2 fiscal 2026, Adobe posted revenue of $6.62 billion, growing nearly 13% year over year and beating the consensus estimate of $6.45 billion by around $167 million. Adobe raised full-year revenue guidance to $26.5 billion to $26.6 billion following the print.

Analysts project Q3 FY26 revenue of around $6.70 billion, up roughly 12% year over year, and Q4 FY26 revenue of around $6.83 billion, up around 10% year over year. Both estimates sit within the revenue trajectory implied by Adobe’s raised full-year guidance range.

Into fiscal 2027, the Street models Q1 revenue of around $6.99 billion, up around 9% year over year, and Q2 revenue of around $7.20 billion, up around 9% as well.

Management set Q3 revenue guidance of $6.67 billion to $6.72 billion, putting the first test of the freemium strategy within one quarter. The Q3 result will determine whether the pivot can sustain double-digit revenue growth without the Creative Cloud pricing lever Adobe deferred for the second half.

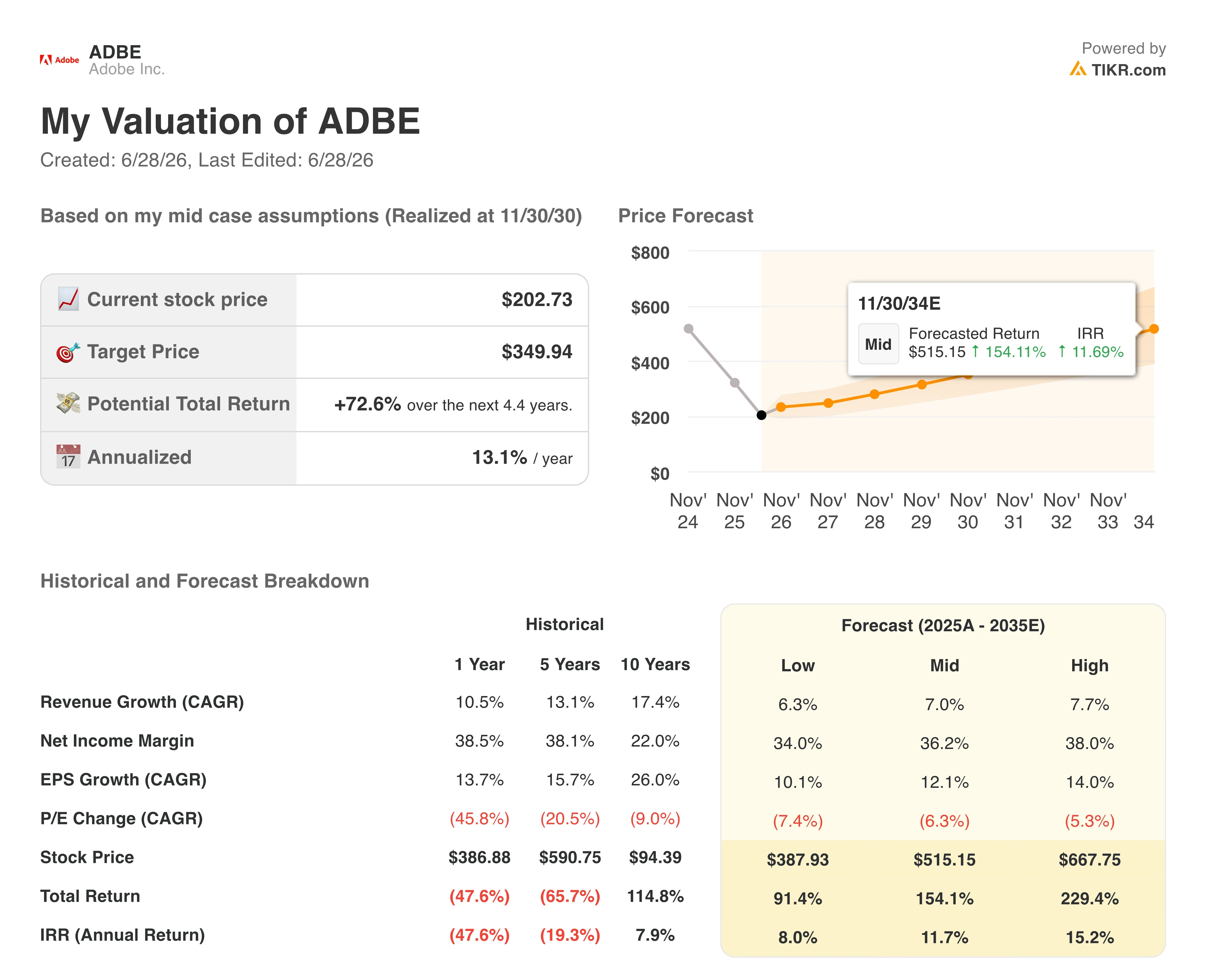

TIKR’s $350 Target on Adobe Stock Holds If the Freemium Funnel Converts as Planned

TIKR’s mid-case model values Adobe at around $350 by November 2030, implying around 73% total return from the current price of around $203, or roughly 13% annualized over 4.4 years.

ADBE Stock Valuation Model Results (TIKR)

ADBE Stock Valuation Model Results (TIKR)

That roughly 13% annualized return positions Adobe stock as a premium-return candidate relative to the broader software sector’s long-run average, reflecting the compressed valuation multiple that the freemium pivot has created.

The path to around $350 rests on the revenue dynamics Adobe anchored at Q2: a raised full-year target of $26.5 billion to $26.6 billion, Firefly annualized recurring revenue approaching $300 million and growing roughly 50% quarter over quarter, and AI-first ARR tripling year over year to exceed $500 million.

Adobe stock’s valuation at roughly 8x forward earnings against that revenue profile is where the gap to $350 lives.

TIKR’s base case puts Adobe stock at around $350 by 2030. Check the full valuation model and historical comps on TIKR for free →

Should You Invest in Adobe Inc.?

The only way to really know is to look at the numbers yourself. TIKR gives you free access to the same institutional-quality financial data that professional analysts use to answer exactly that question.

Pull up Adobe Inc. stock and you’ll see years of historical financials, what Wall Street analysts expect for revenue and earnings in the quarters ahead, how valuation multiples have moved over time, and whether price targets are trending up or down.

You can build a free watchlist to track Adobe Inc. alongside every other stock on your radar. No credit card required. Just the data you need to decide for yourself.

Access Professional Tools to Analyze ADBE stock on TIKR for Free →

You May Also Like

Vitalik Buterin Proposes Self-Sovereign AI Stack To Protect Users From Risks Of AI Agents

Trump’s July 4 plans a 'chaotic' mess as internal emails reveal war between 2 factions