Up 250% YTD, Does Seagate Have More Upside Ahead?

The post Up 250% YTD, Does Seagate Have More Upside Ahead? appeared first on 24/7 Wall St..

Few large-cap stocks have rerated as violently in 2026 as Seagate Technology (NASDAQ:STX). The hard drive maker has ridden a wave of AI-driven storage demand, HAMR product qualification wins, and serial earnings beats to one of the largest moves in the NASDAQ this year. After such an extraordinary run, the question is whether the stock has already priced in the next several years of structural growth.

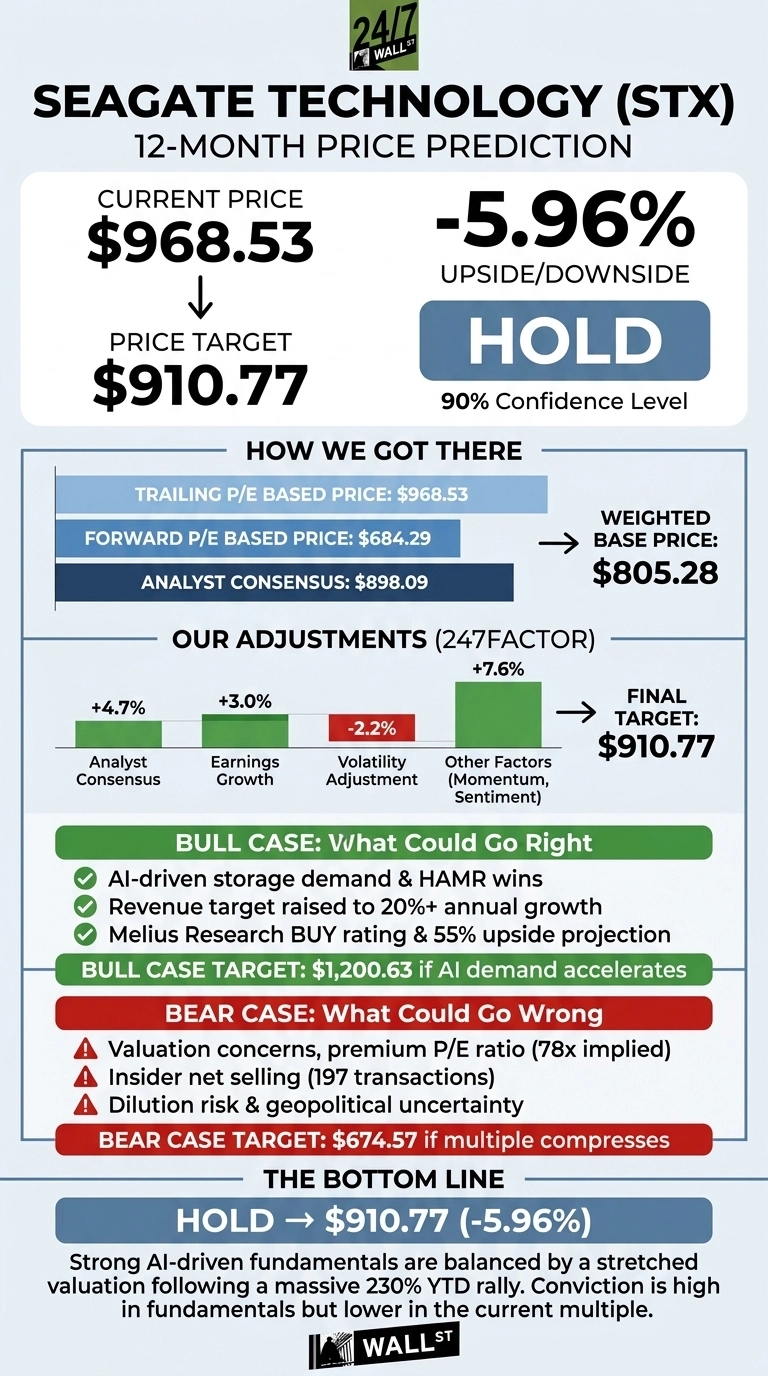

Our 24/7 Wall St. price target for Seagate is $910.77, modestly below the current quote of $968.53. That implies -5.96% over the next 12 months, with a confidence level of 90%. The recommendation is hold.

24/7 Wall St.

24/7 Wall St.

| Metric | Value |

|---|---|

| Current Price | $968.53 |

| 24/7 Wall St. Price Target | $910.77 |

| Upside/Downside | -5.96% |

| Recommendation | HOLD |

| Confidence Level | 90% |

Why We Could Be Wrong

Seagate is one of the most debated names in tech. Our 24/7 Wall St. price target sits below current levels, and the bull case is real. Mizuho lifted its target to $1,090 and Morgan Stanley took its target to $1,035 on a multi-year HDD shortage thesis. If pricing accelerates into fiscal 2027, the stock can clear our number.

How a 590% One-Year Run Reset the Setup

Seagate has gained 252.59% year to date and 590.38% over the past year, with shares jumping 7.63% on June 29 alone.

The catalyst was Q3 FY2026 revenue of $3.11 billion, up 44.07% YoY, paired with non-GAAP EPS of $4.10 and a 47% non-GAAP gross margin. Data center revenue grew 55% YoY to $2.5 billion, and Seagate guided Q4 to $3.45 billion in revenue and $5 in EPS. Shares now sit 22% below the 52-week high of $1,144.18.

The Case for $1,100+

Bulls point to CEO Dave Mosley saying Seagate is “entering a new era of structural growth as AI applications amplify data creation and support sustained storage demand.” Management raised its annual revenue growth target from low- to mid-teens to a minimum of 20%, with nearline capacity allocated through calendar 2027 and the top three CSPs sitting on $1.1 trillion in RPO.

Melius Research initiated with a Buy and 55% upside on June 29. If Mozaic 4 hits 70% of nearline exabyte shipments by end of fiscal 2027, the bull case scenario points to $1,200.63.

What Could Go Wrong

The bear case starts with valuation. Fox Advisors downgraded to Equal-Weight on June 27, citing overly optimistic HDD pricing assumptions. Insider activity has turned to net selling across 197 transactions.

Risks include dilution from Exchangeable Senior Notes due 2028, Middle East exposure, and the Pillar Two minimum tax. Bulls counter that Seagate retired $641 million in debt last quarter and earned a Fitch upgrade to investment grade. The bear scenario points to $674.57, a reminder of how quickly multiples compress.

Seagate Price Prediction 2026-2030

The 24/7 Wall St. price target of $910.77 reflects high conviction in fundamentals and lower conviction in the multiple. The setup would strengthen if the June quarter prints another double-digit beat and management extends visibility into calendar 2028 with pricing intact. The thesis would weaken if HDD pricing flattens or hyperscaler capex softens. For now, the model reads hold.

Looking further out, here is where our model projects Seagate could trade, assuming current trajectories hold and the multiple normalizes toward the sector.

| Year | 24/7 Wall St. Price Target |

|---|---|

| 2026 | $910.77 |

| 2027 | $935 |

| 2028 | $950 |

| 2029 | $960 |

| 2030 | $962.95 |

These projections assume Seagate executes on its HAMR roadmap and AI storage demand stays durable. Significant upside could come from a structural HDD shortage extending into 2028, while sharper downside is possible if hyperscaler capex pauses or pricing rolls over.

Act now: the analyst who called NVIDIA in 2010 just named his top 10 AI stocks — and Seagate Technology didn’t make the cut. Grab the names FREE today.

The post Up 250% YTD, Does Seagate Have More Upside Ahead? appeared first on 24/7 Wall St..

You May Also Like

Pacquiao insists Mayweather fight for real, shuns exhibition insinuation