Delta Air Lines Stock Surged 88% Over the Past Year. Can It Continue Climbing in 2026?

Key Takeaways for Delta Air Lines Stock as of July 2026

- 20 analysts rate Delta a buy against just 1 hold and 1 sell, with a mean target of $86 that sits 8% below the current $93.66 price.

- TIKR’s mid-case model puts Delta stock at $134 by December 2030, a 43% total return and 4% annualized rate from today’s price of $94.

- EBIT is projected to jump from $0.65 billion in the March quarter to $2.72 billion by June 2027, a 91% swing that points to Delta stock trading below its recovering earnings power.

- Following an April 8 call in which fuel averaged $2.62 a gallon, up $0.40 from guidance, Delta is now recapturing 40% to 50% of a $2 billion quarterly fuel hit.

Pull up Delta Air Lines stock on TIKR and see the full EBIT recovery curve, analyst targets, and forward estimates behind this call. Access Professional Tools to Analyze DAL stock on TIKR for free →

Delta Stock Faces a $2 Billion Fuel Hit It’s Already Clawing Back

Delta Air Lines (DAL) runs the largest U.S. network carrier by revenue, anchored by hubs in Atlanta, New York and Los Angeles alongside a vertically integrated jet fuel refinery. In the March quarter, the company posted record revenue of $14.2 billion, up 9% year over year, but pretax profit fell to $530 million as fuel costs spiked following the Iran conflict.

That fuel spike traces directly to the Trainer, Pennsylvania refinery Delta owns through its Monroe Energy subsidiary, which caught fire in June during a restart of its 68,000-barrel fluid catalytic cracker. CFO Dan Janki addressed the cost pressure on the Q1 earnings call: “Fuel prices averaged $2.62 per gallon, including a $0.06 benefit from our refinery. This was nearly $0.40 higher than we expected at the start of the quarter.” Nonfuel unit costs also grew 6% over the prior year.

Even so, demand didn’t crack. Cash sales grew mid-teens in March with momentum extending into April, and CEO Ed Bastian said corporate demand hit double-digit growth across nearly every sector Delta tracks. Diverse revenue streams, including premium seating and loyalty, made up 62% of total revenue.

What matters more for the stock is the recapture math. Delta guided to recovering 40% to 50% of a $2 billion June-quarter fuel headwind through flat capacity and targeted cuts to off-peak flying. Bastian called it explicitly: the industry hasn’t returned its cost of capital in years, and higher fuel is forcing the same consolidation pressure that drove Delta’s 2008 Northwest acquisition. That dynamic sits underneath every forward estimate the Street is now building.

See how Delta’s fuel recapture is playing out in the numbers behind the April print. Access Professional Tools to Analyze DAL stock on TIKR for free →

Wall Street Rates Delta Stock a Buy, But the Target Trails the Price

Street Analysts Target for DAL Stock (TIKR)

Street Analysts Target for DAL Stock (TIKR)

Wall Street holds a decisively bullish consensus on Delta stock, with 20 buy ratings against 5 outperforms, 1 hold, and 1 sell. The mean price target of $86 sits below the current $94 share price, a gap that has persisted through several quarters of target revisions.

That mean has climbed from $80in March 2026, reflecting upward momentum even as it lags spot price.

Wells Fargo raised its price target on U.S. airlines in late June, citing easing costs and tighter capacity, one of several bank actions pushing the average higher through the summer.

Wall Street Expects Delta Stock’s EBIT to Nearly Double by Mid-2027

DAL Stock EBIT Actuals & Estimates (TIKR)

DAL Stock EBIT Actuals & Estimates (TIKR)

Delta posted EBIT of $0.65 billion in the March quarter, down 31% year over year as the fuel spike hit margins directly. Analysts expect a snapback to $1.42 billion in the June quarter and $1.73 billion by December, a 36% year-over-year gain as recapture takes hold.

Looking further out, the Street models EBIT reaching $2.72 billion by June 2027, a 91% increase over the prior year period.

That trajectory rests on one open question: whether fuel prices settle at a “higher for longer” level, as Bastian described it, without eroding the pricing gains Delta has already locked in.

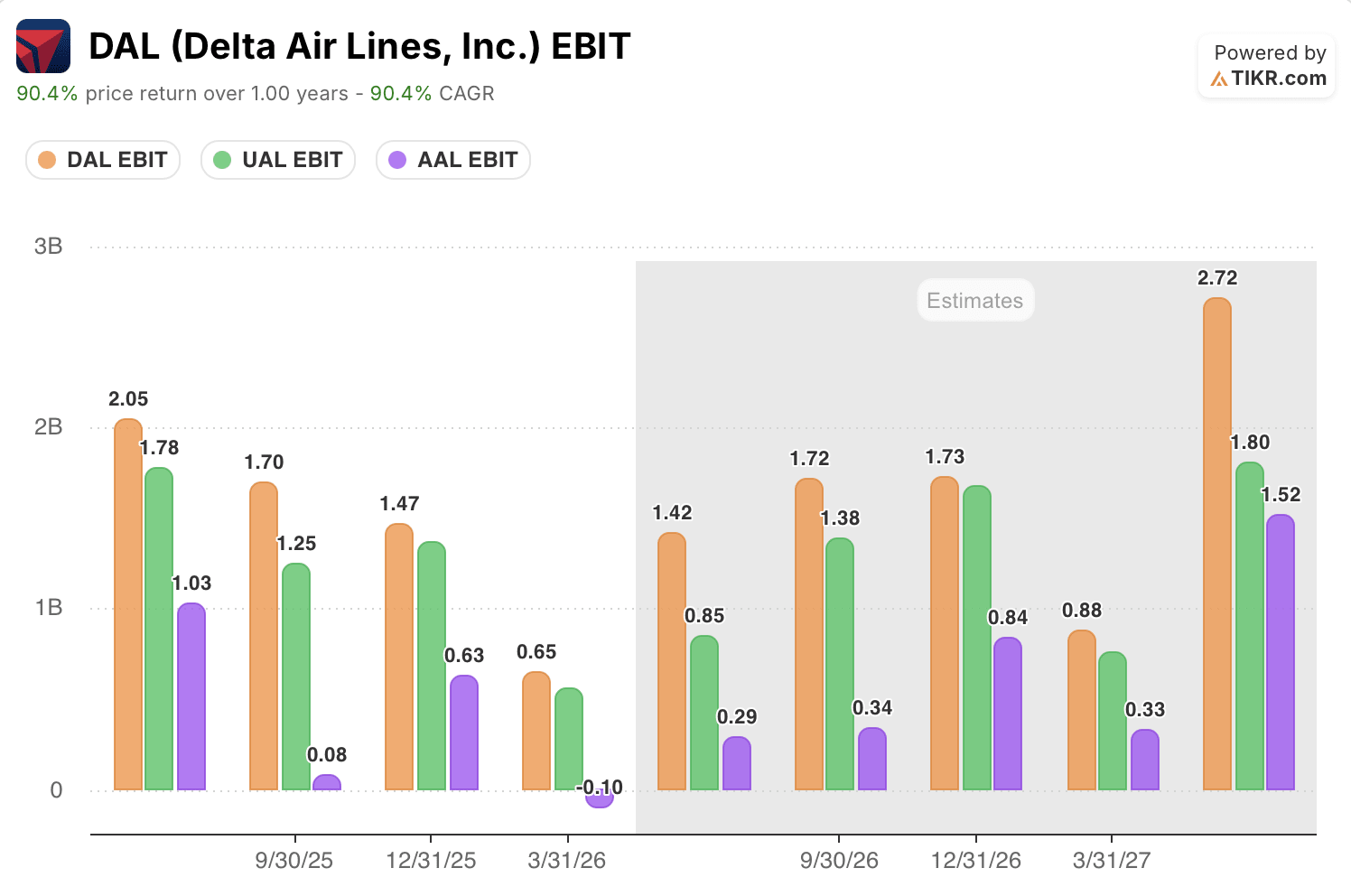

Delta Stock Leads AAL and UAL on EBIT Through Every Forecast Quarter

DAL Stock EBIT vs Peers (TIKR)

DAL Stock EBIT vs Peers (TIKR)

Delta’s EBIT of $1.42 billion in the June quarter outpaces both United Airlines (UAL) at $0.85 billion and American Airlines (AAL) at $0.29 billion, a gap that holds through every forecast period on the chart.

By December 2026, Delta reaches $1.73 billion against United’s $1.38 billion and American’s $0.84 billion. The spread doesn’t close. It widens by June 2027, when Delta’s EBIT hits $2.72 billion versus $1.80 billion for United and $1.52 billion for American.

That gap matters most in the trough quarter. American posted negative EBIT of $0.10 billion in the March quarter while Delta held positive at $0.65 billion, evidence that Delta’s refinery and diversified revenue base cushioned the same fuel spike that pushed a peer into the red.

TIKR’s $134 Target on Delta Stock Holds if Fuel Recapture Sticks

TIKR’s mid-case model values Delta Air Lines at $134 by December 2030, implying a 43% total return from the current price of $94, or 4% annualized over 4.5 years.

DAL Stock Valuation Model Results (TIKR)

DAL Stock Valuation Model Results (TIKR)

That annualized return sits below Delta’s 10-year historical rate of 10.2%, reflecting a market already pricing in much of the near-term recovery after a sharp 1-year run of 86.8%.

The target is reachable because the fuel dynamics driving the March quarter’s earnings compression are the same dynamics Delta is actively recapturing, with EBIT already guided to nearly double by mid-2027. A refinery that partially offsets refining margins, an investment-grade balance sheet with net debt down 20% year over year, and a demand base that held through geopolitical shocks all support the case that this is margin recovery, not margin erosion.

Wall Street’s best ideas don’t stay hidden for long. Catch analyst upgrades, earnings beats, and revenue surprises on thousands of stocks the moment they happen with TIKR for free →

Should You Invest in Delta Air Lines?

The only way to really know is to look at the numbers yourself. TIKR gives you free access to the same institutional-quality financial data that professional analysts use to answer exactly that question.

Pull up Delta Air Lines stock and you’ll see years of historical financials, what Wall Street analysts expect for revenue and earnings in the quarters ahead, how valuation multiples have moved over time, and whether price targets are trending up or down.

You can build a free watchlist to track Delta Air Lines alongside every other stock on your radar. No credit card required. Just the data you need to decide for yourself.

Access Professional Tools to Analyze DAL stock on TIKR for Free →

You May Also Like

Amazon Carbon Project to Restore 50,000 Hectares in South Africa’s Eastern Cape

Vietnam’s economic growth tops expectations in second quarter