Advanced Micro Devices vs Marvell Technology: The Better AI Chip Maker

The post Advanced Micro Devices vs Marvell Technology: The Better AI Chip Maker appeared first on 24/7 Wall St..

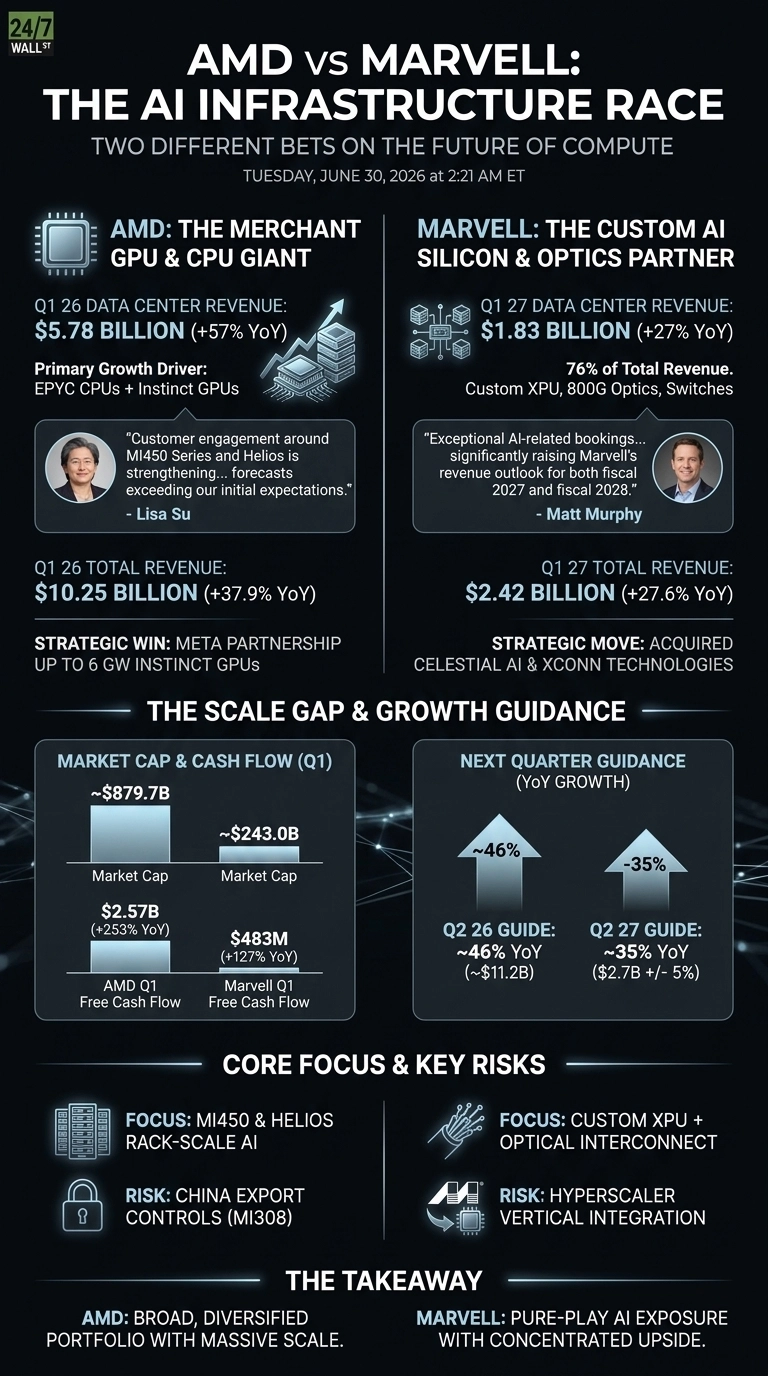

Advanced Micro Devices (NASDAQ: AMD) and Marvell Technology (NASDAQ: MRVL) both just reported quarters that put AI infrastructure at the center of their stories.

AMD posted $10.25 billion in Q1 revenue powered by Instinct GPUs and EPYC servers. Marvell pulled $2.418 billion with custom AI silicon and high-speed optics. Same end market. Very different bets.

Instinct GPUs Carry AMD. Optics and Custom Silicon Carry Marvell.

AMD’s Data Center segment hit $5.78 billion, up 57% YoY, and is now the dominant earnings engine. Lisa Su told investors “customer engagement around MI450 Series and Helios is strengthening, with leading customer forecasts exceeding our initial expectations.”

The Meta deal for up to 6 gigawatts of AMD Instinct GPUs gives that claim teeth. Client Ryzen revenue grew 26% YoY, while Gaming and Embedded stayed modest. The portfolio is broad, and it is finally working in sync.

Marvell came in narrower and faster. Data Center made up 76% of total revenue, growing 27% YoY. Matt Murphy said “we are seeing exceptional AI-related bookings” across 800G and 1.6T optics, 51.2T Ethernet switches, and custom XPU silicon. He raised both the fiscal 2027 and fiscal 2028 outlook. That is rare confidence.

Merchant GPU Heavyweight vs. Hyperscaler Co-Pilot

AMD wants to be the alternative to NVIDIA in merchant AI accelerators. Marvell wants to be the silicon partner inside hyperscaler racks that build their own chips. Those are different theories of where AI margin pools settle.

| Lens | AMD | Marvell |

| Core Bet | MI450 and Helios rack-scale AI | Custom XPU plus optical interconnect |

| Q2 Guide | ~$11.2B, +46% YoY | $2.7B, ~35% YoY |

| Key Vulnerability | China export controls on MI308 | Hyperscaler vertical integration |

| Forward P/E | 74 | 66 |

Marvell also bought Celestial AI (photonic fabric, closed February 2, 2026) and XConn Technologies (chiplet connectivity) to deepen the interconnect moat.

AMD already operates at a different scale, with $2.57 billion in Q1 free cash flow, up 253% YoY. Marvell’s free cash flow of $483 million grew faster on a percentage basis but is roughly a fifth the size.

24/7 Wall St.

24/7 Wall St.

The Next Test Is MI450 Volume and Marvell’s Bookings Conversion

I will be watching whether AMD’s MI450 customer forecasts translate into shipped revenue through the back half of 2026. Lisa Su’s $11.2 billion Q2 guide implies that ramp is already starting.

For Marvell, you should keep an eye on whether those exceptional bookings actually pull forward, and whether custom XPU programs hold as hyperscalers like Google and Amazon push deeper into their own designs.

AMD has rallied 51.86% since filing. Marvell is up 39.78% over a shorter window. Both have already priced in plenty.

Why I Lean AMD for Breadth and Marvell for Pure AI Beta

For steadier compounding exposure, AMD offers more diversified growth handles. The combination of EPYC, Instinct, and Ryzen gives the business multiple growth handles, and the Meta and OpenAI partnerships look durable. The forward multiple at 74x is rich, but the cash generation is real.

If you want concentrated upside tied directly to AI infrastructure spending, Marvell fits better. The narrower model amplifies bookings momentum and Murphy’s accelerating-each-quarter language is uncommon.

I would stay cautious on the customer concentration risk and the steady insider selling, which suggests executives are happy to lock in gains. Both stocks look richly valued, and both can work if AI capex stays this aggressive into 2027.

Act now: the analyst who called NVIDIA in 2010 just named his top 10 AI stocks — and AMD didn’t make the cut. Grab the names FREE today.

The post Advanced Micro Devices vs Marvell Technology: The Better AI Chip Maker appeared first on 24/7 Wall St..

You May Also Like

Belgium eyes tech transfer over rare earths from Malaysia, not just raw exports

Strategic Sanctions: Tether Freezes USDT in TRON Wallets