KLA Corporation Stock Fell 12% in a Day to $236. Here’s What July 28 Earnings Have to Prove

Key Stats for KLA Corporation Stock

- Current Price: $235.55

- Target Price (Mid): ~$360

- Street Target: ~$215

- Potential Total Return: ~54% (over about 4 years)

- Annualized IRR: ~11% / year

- Earnings Reaction: -11.51% (July 2, 2026)

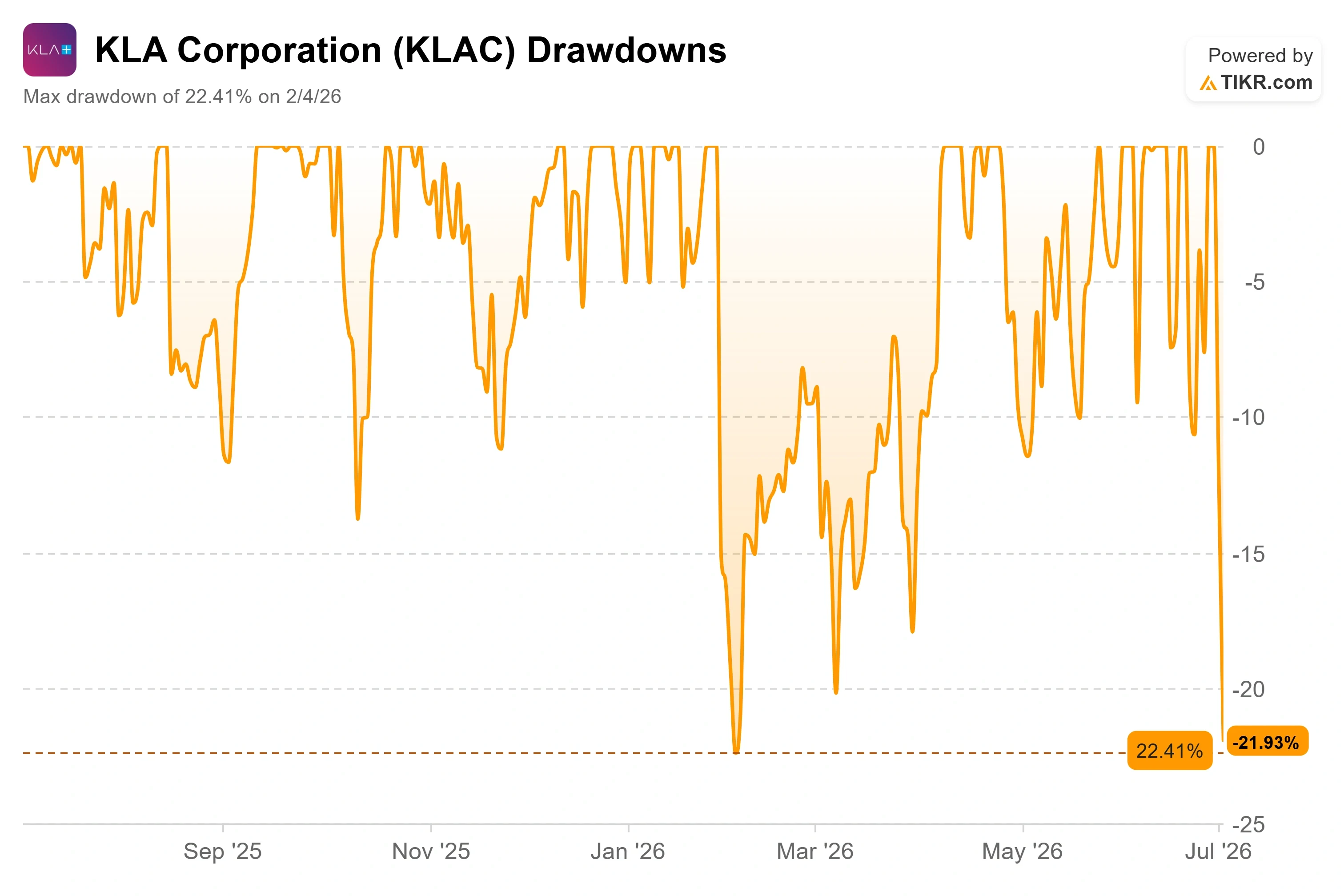

- Max Drawdown: -22.41% (February 4, 2026)

Now Live: Discover how much upside your favorite stocks could have using TIKR’s new Valuation Model (It’s free) >>>

What Happened?

KLA Corporation (KLAC) just lost more than a tenth of its value in a single session, and almost none of it was about KLA. The stock closed July 2 at $235.55, down 11.51% on the day, caught in a broad semiconductor unwind as investors used the turn into the second half to bank one of the best chip rallies on record. The VanEck Semiconductor ETF had surged 82% in the first half of 2026, and the calendar flip became an excuse to sell. Nothing broke inside the company. The tape simply reset.

That leaves KLAC shareholders staring at an uncomfortable split screen. This is one of the highest-quality businesses in the entire chip supply chain, and yet the average analyst still thinks it should trade lower than it does right now. The move down did not resolve that argument. It sharpened it. And the next real chance to settle it lands on July 28, when KLA reports fiscal Q4 2026.

A great business knocked down on someone else’s news

KLA makes process control tools, the inspection and metrology systems chipmakers use to catch defects and lift manufacturing yields. It is not a commodity equipment vendor. It is the dominant name in its niche, running at 7.5 times the size of its nearest process-control competitor, and it just posted another year of share gains. So when the whole group sells off on profit-taking, KLA falls with it, and the drop tells you more about positioning than about the fundamentals.

The profit-taking did not appear in a vacuum. Short interest in KLAC had exploded through late June, jumping more than 1,000% to roughly 40.8 million shares, about 36.6% of the float. A crowded short base makes the stock jumpier in both directions, which is part of why single-session moves keep landing in double digits. This is not a quiet stock. It has had 25 moves greater than 5% over the past year.

The deeper reason the group is nervous is memory. In late June, a report that South Korea’s SK Hynix is slowing its shift to next-generation HBM4, the stacked memory that feeds AI chips, rattled the entire AI-chip complex. High-bandwidth memory is one of KLA’s real growth drivers, so any hint that the memory buildout is cooling hits sentiment directly, even when order books have not changed.

KLA Corporation Drawdowns (TIKR)

KLA Corporation Drawdowns (TIKR)

See historical and forward estimates for KLA Corporation stock (It’s free!) >>>

What management actually said three weeks ago

Here is the disconnect. While the tape was busy panicking, KLA’s own commentary was moving the other way. At the Bank of America 2026 Global Technology Conference on June 3, CFO Bren Higgins told investors the visibility into next year was unusually clear. “The visibility is really remarkable to be midway through ’26 and be talking about ’27 and talking about ’27 with meaningful growth expectations,” Higgins said. That reframes the memory scare as noise against a backlog that already extends well into 2027.

The more striking data point was structural. Higgins walked through KLA’s advanced packaging business, the back-end work of connecting and stacking chips that AI processors increasingly depend on, and the growth curve is steep. “We’re going to be $1 billion in packaging, up from $635 million last year and $300-ish million the year before,” he said. That is a business that barely existed for KLA a few years ago, when it held under 1% of the advanced packaging market. It now holds over 6%, heading toward the mid-7% range, because hybrid bonding and die-stacking have pushed packaging toward front-end complexity, which is exactly where KLA’s tools win.

Higgins also nudged up the long-term ceiling. Asked whether investors should rethink the company’s 2030 wafer fab equipment assumption, meaning the total tool market chipmakers buy, he put the internal number at $215 billion. Pressed on whether there was still upside to that, he agreed there was “more to go.” A CFO lifting a long-term market assumption in the same weeks the stock is being sold off is the kind of gap between narrative and fundamentals that patient investors wait for.

The valuation is the real fight

None of that makes the stock obviously cheap, and pretending otherwise would be dishonest. Even after the 11.51% drop, KLAC trades at a rich forward multiple, and the analyst data is blunt about it. The Street’s mean target sits at around $215, below the $235.55 close. The breakdown skews bullish in direction, at 13 Buys, 5 Outperforms, 10 Holds, 1 Underperform, and 1 Sell, but the targets say the average analyst still sees the stock as ahead of itself. When a double-digit drop still leaves the price above consensus, the discount is shallower than the red candle suggests.

The bulls have a specific rebuttal, and it is not just hope. KLA has topped revenue estimates in each of the last five quarters, so the argument is that consensus targets are anchored to a stale baseline that estimates are already outgrowing. That is the whole tension in one line: the bears are pricing the multiple, the bulls are pricing the revisions. The disagreement runs right through the analyst community itself, where fresh targets range from Bank of America’s raised $317 and Cantor’s Street-high $325 down to a mean near $215.

KLA also does not look cheap next to its peers. On next-twelve-months EV/EBITDA, KLAC trades around 41 times against a peer-group median near 32 times, with Applied Materials at roughly 35 times and Lam Research at roughly 40 times. On NTM EV/revenue, KLA sits around 19 times versus a group median closer to 11 times. That premium is not irrational, because KLA earns a 61.4% gross margin and a 43.9% return on invested capital that most of the group cannot touch. But it does mean the stock is priced for continued execution, not for a stumble. There is very little margin for error baked into the price.

KLA Corporation NTM EV/EBITDA (TIKR)

KLA Corporation NTM EV/EBITDA (TIKR)

See how KLA Corporation performs against its peers in TIKR (It’s free!) >>>

TIKR Advanced Model Analysis

- Current Price: $235.55

- Target Price (Mid): ~$360

- Potential Total Return: ~54%

- Annualized IRR: ~11% / year

KLA Corporation Advanced Valuation Model (TIKR)

KLA Corporation Advanced Valuation Model (TIKR)

See analysts’ growth forecasts and price targets for KLA Corporation stock (It’s free!) >>>

This is the mid case, chosen because it reflects neither a memory-cycle collapse nor a blue-sky AI melt-up, and it lines up with what management has actually guided.

Two revenue drivers carry the model. The first is advanced packaging, growing from $635 million toward a targeted $1 billion this year as AI chips demand more inspection. The second is rising process-control intensity at the leading edge, where bigger die, tighter defect budgets, and EUV adoption in DRAM all pull more of KLA’s tools into every fab. The margin driver is KLA’s differentiated, value-priced portfolio, which management expects to lift gross margin from about 62% toward the 63% to 64% range over time. The primary risk is a memory-capex retrenchment, the same fear the SK Hynix headline just triggered.

The upside case is that AI-driven wafer fab equipment spending compounds through 2027 and beyond, and KLA keeps gaining share while packaging scales, pushing results past today’s stale consensus. The downside case is that memory investment stalls, the cyclical end market bites, and a premium multiple compresses fast on a stock priced for perfection.

Conclusion

The number that settles this is revenue on July 28. KLA guided fiscal Q4 to about $3.575 billion, so a print at or above that, paired with any commentary that second-half supply constraints are easing, makes the post-drop price look like the entry bulls are describing. A miss, or softer forward guidance that confirms the memory worry, hands the bears their valuation case and gives the premium multiple a reason to compress. Watch the revenue line against $3.575 billion, and watch whether management holds or lifts the packaging and 2027 framing Higgins laid out in June. That is the tell. Everything else on July 2 was just the calendar.

See what stocks billionaire investors are buying so you can follow the smart money with TIKR.

Should You Invest in KLA Corporation?

The only way to really know is to look at the numbers yourself. TIKR gives you free access to the same institutional-quality financial data that professional analysts use to answer exactly that question.

Pull up KLA Corporation, and you’ll see years of historical financials, what Wall Street analysts expect for revenue and earnings in the quarters ahead, how valuation multiples have moved over time, and whether price targets are trending up or down.

You can build a free watchlist to track KLA Corporation alongside every other stock on your radar. No credit card required. Just the data you need to decide for yourself.

Analyze KLA Corporation on TIKR Free →

Looking for New Opportunities?

- See what stocks billionaire investors are buying so you can follow the smart money.

- Analyze stocks in as little as 5 minutes with TIKR’s all-in-one, easy-to-use platform.

- The more rocks you overturn… the more opportunities you’ll uncover. Search 100K+ global stocks, global top investor holdings, and more with TIKR.

Disclaimer:

Please note that the articles on TIKR are not intended to serve as investment or financial advice from TIKR or our content team, nor are they recommendations to buy or sell any stocks. We create our content based on TIKR Terminal’s investment data and analysts’ estimates. Our analysis might not include recent company news or important updates. TIKR has no position in any stocks mentioned. Thank you for reading, and happy investing!

You May Also Like

Silver’s Stalemate: An Equilibrium Waiting to Break?

PMI-ACP Exam Preparation: How to Use a Simulator and Practice Questions Effectively

Franklin Templeton CEO Dismisses 50bps Rate Cut Ahead FOMC