AMD vs Palantir: Which AI Giant Is a Better Buy?

The post AMD vs Palantir: Which AI Giant Is a Better Buy? appeared first on 24/7 Wall St..

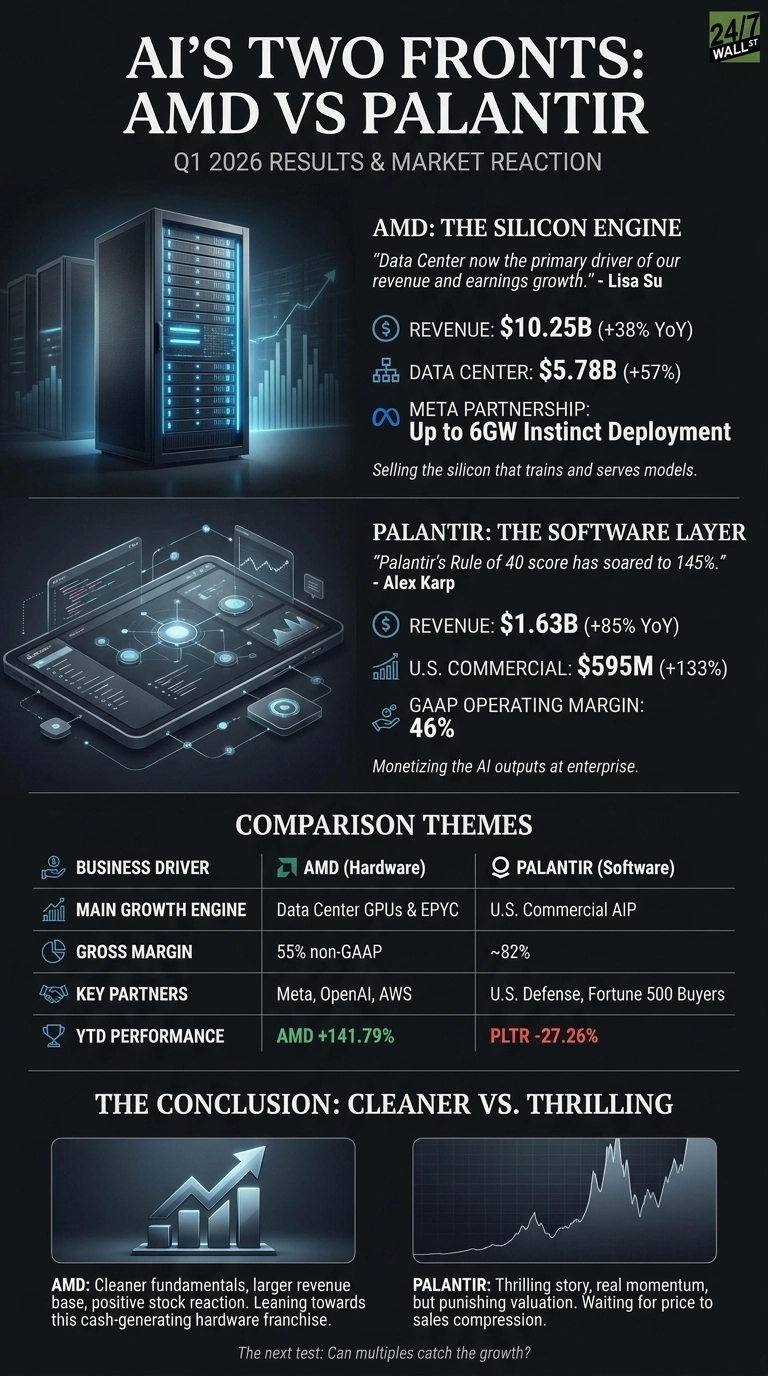

AMD (NASDAQ:AMD) and Palantir (NASDAQ:PLTR) both delivered blockbuster Q1 2026 results in early May, attacking the AI opportunity from different angles.

AMD sold the silicon that trains and serves models. Palantir sold the software layer that turns those models into enterprise workflows. Two months later, the market is rewarding execution very differently.

Instinct GPUs Carry AMD. U.S. Commercial Carries Palantir.

AMD posted revenue of $10.253 billion, up 37.85% YoY, with Data Center alone contributing $5.775 billion at +57%. That segment is now the engine, powered by EPYC servers and Instinct MI350 shipments.

Lisa Su told investors that “Customer engagement around MI450 Series and Helios is strengthening, with leading customer forecasts exceeding our initial expectations.” The Meta deal for up to 6 gigawatts of Instinct deployment gives that claim real weight.

Palantir grew faster off a smaller base. Revenue hit $1.63 billion, up 84.71%, with U.S. Commercial exploding 133% to $595 million. AIP is clearly landing with corporate buyers.

Alex Karp noted that “Palantir’s Rule of 40 score has soared to 145%.” The company closed 206 deals of at least $1 million, signaling that AIP is becoming a repeatable enterprise sale rather than a bespoke consulting engagement.

24/7 Wall St.

24/7 Wall St.

| Business Driver | AMD | Palantir |

| Main growth engine | Data Center GPUs and EPYC | U.S. Commercial AIP |

| Gross margin | 55% non-GAAP | ~82% |

| Key partners | Meta, OpenAI, AWS | U.S. defense and Fortune 500 buyers |

Picks and Shovels vs. Finished Product

AMD is a scale story. Su is chasing a hyperscaler capex cycle where every extra gigawatt of Instinct capacity flows into a huge, lower-margin revenue line. Guidance for Q2 revenue of roughly $11.2 billion with 56% gross margin reflects that trade-off. Export controls on MI308 to China remain a live risk, and TSMC dependence never goes away.

Palantir is monetizing the output layer, which is why GAAP operating income reached a 46% margin. Karp raised FY26 revenue guidance to $7.65 to $7.66 billion. Valuation is punishing. Price to sales sits near 53, and shares are down 27.26% year to date even after the quarter.

The Next Test Is Whether the Multiple Catches the Growth

AMD stock has ripped 141.79% YTD to $517.82, brushing the $508.31 analyst target. Watch whether MI450 revenue in the back half justifies a forward P/E near 77.

For Palantir, keep an eye on whether U.S. commercial can sustain triple-digit growth against a still-heavy $201.6 million stock-based comp bill.

Why I Lean Toward AMD Right Now

AMD looks cleaner. The revenue base is larger, the customer list is concrete, and the stock is reacting positively to fundamentals. Palantir is the more thrilling story, and Karp’s momentum is real, but I want to see the price to sales compress first.

For investors tracking turnaround setups, PLTR’s YTD drawdown is notable. For those following the AI capex boom through a cash-generating hardware franchise, AMD’s fundamentals currently stand out.

Act now: the analyst who called NVIDIA in 2010 just named his top 10 AI stocks — and AMD didn’t make the cut. Grab the names FREE today.

The post AMD vs Palantir: Which AI Giant Is a Better Buy? appeared first on 24/7 Wall St..

You May Also Like

Ozak AI Update: New Website Track Referrals as Launch Date Nears

LEGO Faces Backlash Over Pride-Themed Content Aimed At Kids

ETH Enters High-Stakes Decision Zone