American Airlines Is Barely Breaking Even in 2026. Here’s Where the Stock Could Go

Key Stats for American Airlines Stock

- Current Price: $15.99

- Street Target (Mean): ~$16

- Earnings Reaction: +2.72% (4/23/26)

- Max Drawdown: 37.39% (3/30/26)

Now Live: Discover how much upside your favorite stocks could have using TIKR’s new Valuation Model (It’s free) >>>

What Happened?

American Airlines Group Inc. (AAL) is being priced as a company with one bad year and no clear way out. The stock sits at $15.99, near the low end of a range that bottomed with a 37.39% drawdown on March 30, 2026. The market has decided 2026 is a write-off. What has not been decided, and what every dollar of upside depends on, is whether 2027 looks completely different.

That is the fight. Bears see an over-leveraged carrier with no fuel hedges getting run over by a commodity spike. Bulls see a commercial operation still posting strong demand, held underwater by a fuel price almost nobody expects to last. The question is simple: when fuel normalizes, does America’s earnings power come back, or has the damage become structural?

Why 2026 Earnings Collapsed

The cause is fuel, not demand. After strikes on Iran shut the Strait of Hormuz in late February, jet fuel climbed roughly 70% year over year. The International Air Transport Association expects jet fuel to be near $152 a barrel in 2026 versus about $90 in 2025, and projects industry profits to halve to $23 billion.

CEO Robert Isom put numbers on the hit at the company’s June 10 annual meeting, saying fuel is now expected to add more than $5 billion to expenses year over year, leaving 2026 roughly flat to 2025. He did not argue the hit away. He argued it was temporary: “As fuel prices normalize and we continue delivering strong top line performance, we expect meaningful margin improvement in 2027 and beyond.”

American Airlines Drawdowns (TIKR)

American Airlines Drawdowns (TIKR)

See historical and forward estimates for American Airlines stock (It’s free!) >>>

The 2027 Inflection in the Estimates

This is where the data tells a different story from the headlines. The same business that barely breaks even in 2026 is expected to earn real money in 2027, according to consensus estimates on TIKR:

- EBIT rises from about $1,341M to roughly $3,257M

- Net income jumps from about $58M to roughly $1,472M

- EPS goes from around $0.05 to about $2.23

Revenue only climbs from about $61.9 billion to $64.6 billion over that span, so the rebound is a margin story, not a volume story. The entire bull case rests on that one transition holding.

The Macro Setup Just Shifted

The reason this is a live debate landed four days ago. The International Energy Agency said the oil market could swing to a surplus of more than 5 million barrels per day in 2027, as Strait of Hormuz flows recover and supply rises about 8 million barrels per day against demand growth of just 2 million. A glut that size would push fuel costs down, which is exactly the condition the 2027 estimates assume.

That is the counterweight to the bear case. Bears are right that American carries $26.98 billion in net debt at 2.99x leverage, and at $152 fuel, that is dangerous. But the IEA’s base case is not that world, and in a recovery, the company’s fuel exposure flips from a liability into leverage on the way up.

The Discount, And the Risk

At $15.99, American trades at about 0.60x forward revenue, closer to a distressed asset than a recovering one. That is the opportunity if the rebound shows up, and the trap if it does not. The thesis lives or dies on fuel. If the U.S.-Iran deal breaks, if Hormuz stays constrained, or if the surplus arrives later and smaller than forecast, thin margins and heavy net debt leave almost no cushion for a second year of elevated fuel.

Isom also used the meeting to kill merger speculation, saying regulators across the political spectrum viewed a United combination as a “nonstarter.” For anyone who treated a deal as a hidden floor under the stock, that floor is gone. American is a standalone turnaround now.

American Airlines EBIT & Net Income (TIKR)

American Airlines EBIT & Net Income (TIKR)

See how American Airlines performs against its peers in TIKR (It’s free!) >>>

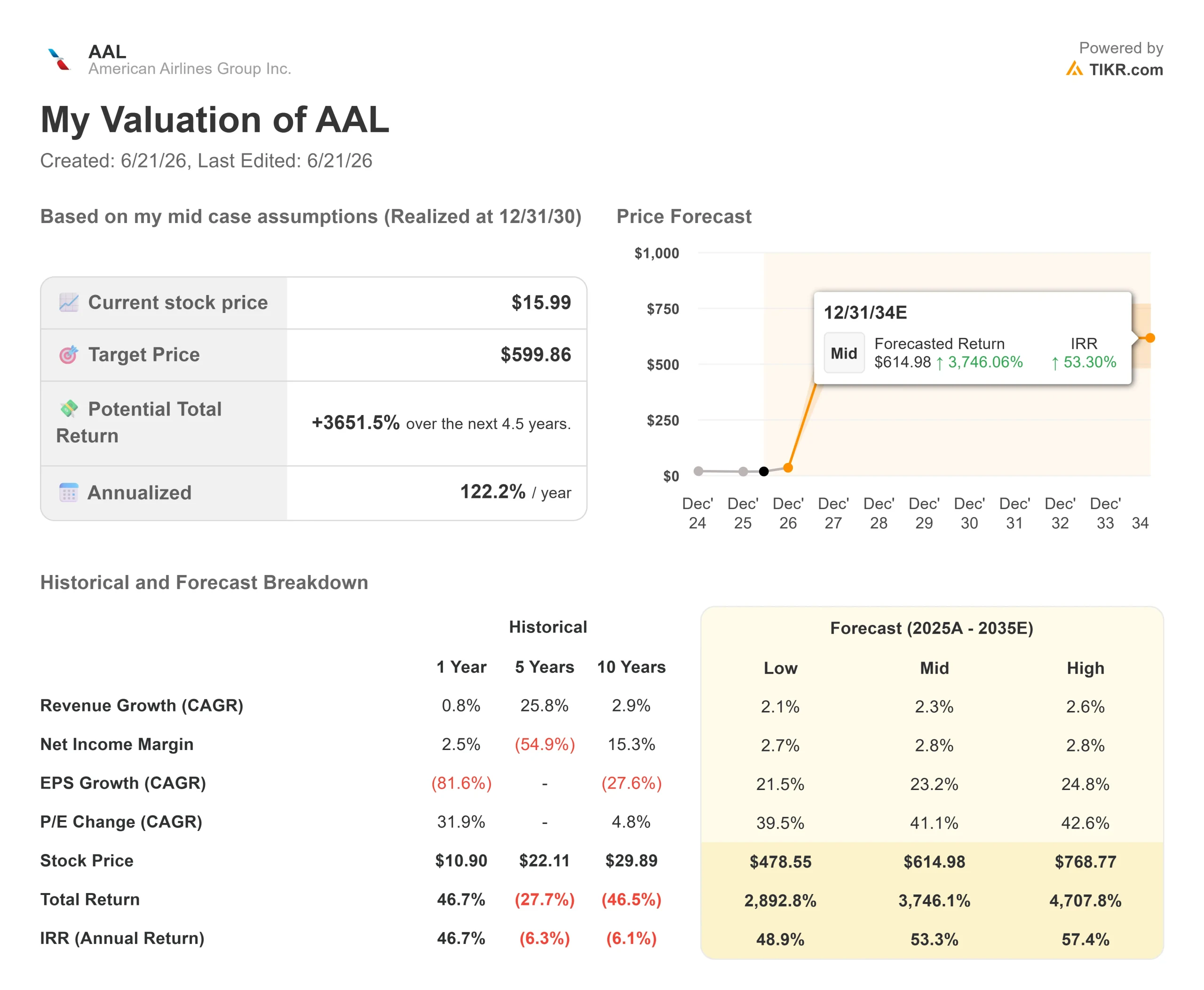

TIKR Advanced Model Analysis

American Airlines Advanced Valuation Model (TIKR)

American Airlines Advanced Valuation Model (TIKR)

See analysts’ growth forecasts and price targets for American Airlines stock (It’s free!) >>>

The mean sits right where the stock trades, but the gap between the $10 and $24 targets is the fuel question in numerical form. The revenue driver behind the upside is continued demand growth, with revenue estimated to rise from about $61.9 billion in 2026 to $64.6 billion in 2027. The margin driver is fuel normalization in 2027, the single variable that turns a near-breakeven 2026 into an estimated $2.23 in EPS the next year. The primary risk is the mirror image: sustained high fuel against $26.98 billion in net debt.

Upside, in one line: if fuel normalizes on the IEA’s 2027 timeline and demand holds, margins recover sharply, and the path toward the high-$20s opens.

Downside, in one line: if fuel stays elevated into a second year, leverage and thin margins expose the stock to the $10 target.

Conclusion

Watch unit revenue at the Q2 2026 report, expected in late July. Isom said the commercial engine is still delivering strong top-line performance, and that report is the proof, while fuel does its damage. Good, looks like revenue growth is holding up alongside early signs of fuel cost recovery. Bad looks like demand softening while fuel stays high, because that would undercut the one thing bulls are counting on.

The bigger verdict comes from outside the company: whether the IEA’s 2027 oil surplus actually arrives. American has built a business that works at roughly $90 fuel. The market will spend the next year deciding whether it gets back there.

See what stocks billionaire investors are buying so you can follow the smart money with TIKR.

Should You Invest in American Airlines?

The only way to really know is to look at the numbers yourself. TIKR gives you free access to the same institutional-quality financial data that professional analysts use to answer exactly that question.

Pull up American Airlines, and you’ll see years of historical financials, what Wall Street analysts expect for revenue and earnings in the quarters ahead, how valuation multiples have moved over time, and whether price targets are trending up or down.

You can build a free watchlist to track American Airlines alongside every other stock on your radar. No credit card required. Just the data you need to decide for yourself.

Analyze American Airlines on TIKR Free →

Looking for New Opportunities?

- See what stocks billionaire investors are buying so you can follow the smart money.

- Analyze stocks in as little as 5 minutes with TIKR’s all-in-one, easy-to-use platform.

- The more rocks you overturn… the more opportunities you’ll uncover. Search 100K+ global stocks, global top investor holdings, and more with TIKR.

Disclaimer:

Please note that the articles on TIKR are not intended to serve as investment or financial advice from TIKR or our content team, nor are they recommendations to buy or sell any stocks. We create our content based on TIKR Terminal’s investment data and analysts’ estimates. Our analysis might not include recent company news or important updates. TIKR has no position in any stocks mentioned. Thank you for reading, and happy investing!

You May Also Like

This insane JD Vance admission has Republicans — and Fox News — paralyzed with fear

Turkish lira stablecoins show why Europe’s regulated euro tokens may struggle

Does the World’s First Trillionaire Pay Less Into Social Security Than You? A New Fact-Check Weighs In