Alchemy’s AgentCard and Visa: Are AI Commerce Rails Becoming the Next Stablecoin Distribution Layer?

AI agents are moving from chatboxes to checkout. With Alchemy’s AgentCard launching on Visa’s new commerce stack, developers can now provision an agent with payments and identity in minutes. This piece explains what’s actually live, how the rails route money, and whether these agent-native flows could become the next distribution layer for stablecoins.

We’ll cover what AgentCard does today, where stablecoins fit, how this differs from prior “crypto card” attempts, and the real implementation and compliance work you’ll still need to do. Expect practical comparisons, trade-offs, and a clear-eyed look at risks.

Short answer: yes—AI commerce rails are positioned to become a fresh distribution layer for stablecoins, but most transactions will still touch card networks in the near term. Alchemy’s AgentCard, built on Visa Intelligent Commerce, provisions each agent with payment credentials and a wallet via one API, defaulting to tokenized card payments while supporting crypto where accepted. Visa’s scale and early stablecoin volume suggest meaningful distribution potential, but builders must plan for compliance, routing fallbacks, and fee economics as they stand today.

- AgentCard sets up an agent’s card token, email, phone, and wallet in under a minute (PR Newswire (Alchemy press release)).

- Visa reports an annualized stablecoin run rate of about $7B and 160+ stablecoin-linked card programs (Visa investor press release (Visa Payments Forum 2026)).

- AgentCard defaults to tokenized card payments, with routing that can select agent-native protocols and crypto where merchants accept them; it can fall back to single-use tokens (PR Newswire (Alchemy press release)).

- Adoption hinges on merchant acceptance, compliance, dispute processes, and fee math—especially for microtransactions.

How does AgentCard actually route money today?

AgentCard is a developer-facing layer that gives every AI agent a payment identity and operational tooling. According to the launch materials, each agent can be provisioned with a Visa payment token, a dedicated email, a phone number, and a crypto wallet from a single API call, with setup in under a minute (PR Newswire (Alchemy press release)). The goal: practical, programmatic purchasing by AI agents without custom card-on-file hacks or duct-taped wallets.

By default, AgentCard routes via Visa-issued tokenized card payments. That means merchants generally see familiar card rails, benefiting from network fraud controls, chargeback rights, and global acceptance. Where a merchant supports crypto or emerging agent-native protocols, AgentCard says it can route to those rails; otherwise, the system can fall back to single-use tokens for security (PR Newswire (Alchemy press release)).

Visa’s own disclosures provide context: the company highlighted new AI, stablecoin, and token initiatives at its June 2026 forum and noted it has moved “billions of dollars” in stablecoins, with an annualized run rate of roughly $7 billion as of March 2026 (Visa investor press release (Visa Payments Forum 2026)). It also cited more than 160 stablecoin-linked card programs live or in development globally. In short, the card ecosystem is already experimenting at scale—AgentCard slots into that momentum with an agent-first wrapper.

Are AI commerce rails really becoming the next stablecoin distribution layer?

Distribution is ultimately about endpoints and user journeys. Stablecoins have three primary growth engines today: centralized exchanges and brokerage apps, on/off-ramp fintechs, and embedded wallets in consumer apps. AI agents unlock a fourth: autonomous or semi-autonomous spenders making frequent, programmatic purchases on behalf of users or organizations. If those agents are funded in stablecoins—even if settlement to merchants is via card rails—stablecoins become the funding currency that flows into and through these agent accounts.

Why this matters: agents generate repeatable, machine-speed demand. Think: inventory restocks, SaaS renewals, data/API usage, ride-hail, travel, or ad credits. If top-ups are made in stablecoins, each AgentCard instance becomes another sink and conduit for stablecoin liquidity. Over time, as more merchants accept crypto directly, some of those flows can stay on-chain end-to-end, but even now, the funding leg may be stablecoin while the acceptance leg remains card.

Visa’s numbers don’t guarantee adoption, but they show the pipes are being built. A $7B annualized run rate and 160+ stablecoin-linked programs suggest that when AI-native rails arrive with enterprise-grade tokenization, we’re not starting from zero capacity (Visa investor press release (Visa Payments Forum 2026)).

What separates AgentCard from older crypto cards and standard web3 wallets?

AgentCard is not just “another crypto card.” It’s an orchestration layer designed for machine actors. It binds identity artifacts (email, phone) with a tokenized card credential and a crypto wallet per agent, exposing controls to program policy, limits, and routing. The developer surface is the product; the card is only one rail.

To clarify how this differs from older models, here’s a qualitative comparison:

Feature AgentCard (AI-first) Stablecoin-linked Cards (legacy) Standard Web3 Wallets Primary user AI agents acting on policy Human cardholders Human wallet owners Default rail Visa tokenized card (with crypto/protocol routing where accepted) Card rails with crypto funding On-chain transfers only Identity artifacts Per-agent email, phone, token, wallet Card + KYC profile Wallet address; optional KYC via partners Automation depth Built for programmatic spend, policy engines Limited; human-initiated Programmable via smart contracts, limited merchant acceptance Merchant reach Global card acceptance; selective crypto where supported Global card acceptance Merchant must accept crypto

The net: AgentCard is an agent operations stack with payments as the backbone. It inherits card ubiquity while nudging spend toward agent-native or crypto flows when feasible, without forcing merchants to change terminals first.

What should builders validate before integrating AgentCard or similar rails?

Before wiring real money to machine actors, teams need guardrails. Use a checklist and treat this like standing up a new bank account for a bot—with stricter controls.

- Scope and limits: Set per-transaction caps, daily/weekly budgets, MCC/category blocks, and merchant allowlists.

- Identity and policy: Confirm how per-agent email/phone are used for 3DS, OTP, or merchant verification. Map escalation flows for failed verifications.

- Funding flows: Decide whether to top up in fiat, stablecoins, or both; understand conversion steps and who holds custody at each hop.

- Settlement and fees: Model card network fees, FX spreads, and any crypto conversion costs. Test microtransaction viability.

- Disputes and chargebacks: Define who owns representment and how evidence is captured from agent logs.

- Compliance: Clarify KYC/KYB for the entity behind the agents, sanctions screening, and ongoing monitoring duties.

- Observability: Instrument real-time alerts for anomalous spend, declined auths, and rapid-fire retries.

- Key and wallet ops: Decide whether to self-custody agent wallets or rely on a managed HSM/MPC provider; rotate keys on agent lifecycle events.

Where do fees, risks, and compliance land in 2026?

Economics first: tokenized card transactions still incur card network and issuer fees. For larger tickets or subscription invoices, this may be acceptable for the reach and reliability you gain. But microtransactions can be pressured by minimum fees and authorization overhead. If your use case leans on many small purchases, consider batching, prepaid funding, or shifting some flows to on-chain rails where the merchant accepts them.

Risk next: you inherit new categories—agent misbehavior, prompt or model exploits, and fraud patterns that exploit automated retries. Tokenization and single-use credentials reduce exposure, but you’ll need spending policies and velocity controls. Recordkeeping becomes critical: when an agent buys something, the who/why/when must be reconstructable for disputes and audits.

Compliance: AgentCard’s per-agent identity artifacts simplify mapping behavior to an accountable entity, but obligations remain with the business deploying agents. Expect KYC/KYB for the sponsor entity, sanctions checks, consumer disclosures where relevant, and data protection controls for agent-held PII. If you fund with stablecoins, confirm how those assets are custodied and whether any money transmission or VASP obligations apply in your jurisdictions.

Who should adopt now, and for what use cases?

Early adopters getting the most lift tend to share traits: repetitive purchasing, global merchant exposure, need for programmatic control, and tolerance for current fee structures. Good fits include software teams automating SaaS renewals, marketing ops buying ad credits, procurement agents reordering supplies, travel concierges handling dynamic bookings, and developer tools paying for usage-based APIs.

Where this might be premature: consumer micro-rewards under a few cents, high-frequency arbitrage that lives or dies on fee basis points, and merchants that already accept stablecoins directly at scale. In those cases, a direct on-chain settlement path may be cheaper, provided your counterparties can receive—and accounting can keep up.

Pragmatically, AgentCard offers a near-term bridge: keep the merchant side largely unchanged while enabling agent-native controls and crypto funding on your side. As more merchants turn on crypto acceptance, your routing logic can evolve without rewriting your agent stack.

How do we measure success when agents start spending?

Operational KPIs should combine payment health with agent behavior. Track authorization rates by merchant category, decline codes, average ticket size, and chargeback ratios. Layer in agent-specific metrics like successful task completion rate, mean time to resolution for failed purchases, and the ratio of automated to manual interventions.

For treasury, watch funding currency mix (fiat vs stablecoins), conversion costs, and realized spreads. Stress test settlement timelines and reconciliation: can you trace a top-up through to spend and refund events? Look at gross savings from automation against payment and dispute costs, not just headline interchange.

Finally, audit policy efficacy: are budget caps and allowlists preventing out-of-scope spend without breaking legitimate flows? Use staged rollouts with shadow agents before giving unlimited autonomy.

Common Mistakes

- Skipping per-agent limits and allowlists: Without scoped budgets and merchant controls, a single compromised agent can create outsized losses.

- Underestimating dispute ops: Chargebacks require structured evidence. If you don’t log prompts, agent decisions, and merchant responses, you’ll lose recoveries.

- Ignoring conversion costs: Stablecoin top-ups don’t equal zero-fee spend. Model card fees, FX, and on/off-ramp spreads together.

- Relying on a single rail: If crypto acceptance fails or a merchant blocks agent traffic, you need card fallbacks and single-use tokens ready.

- Weak key management: Agent wallets without rotation, segregation, or HSM/MPC controls are a breach waiting to happen.

- Thin compliance mapping: Treat agents as operational extensions of your entity; document KYC/KYB, sanctions screening, and data controls.

For ongoing coverage of AI-commerce intersections and stablecoin infrastructure, visit Crypto Daily.

Frequently Asked Questions

Can a team fund AgentCard balances purely with stablecoins?

Funding options depend on the program and partners you use. Many setups can accept stablecoin top-ups, but acceptance rails to merchants may still run on tokenized card payments. Clarify custody, conversion points, and whether any balances are held in fiat vs on-chain at rest.

What happens when a merchant doesn’t accept crypto?

AgentCard defaults to Visa tokenized card payments, so the purchase proceeds over card rails. Only when a merchant supports crypto or agent-native protocols would routing shift; otherwise, the system can fall back to single-use tokens for security.

How do chargebacks and disputes work for agent purchases?

They generally follow card-network processes. Your evidence packet should include timestamps, prompts or instructions the agent acted on, merchant communications, delivery proofs, and any two-factor steps completed via the agent’s designated email or phone.

Can DAOs or decentralized teams provision AgentCards for contributors?

Structurally, yes, but a real-world legal entity usually sponsors the program and handles KYC/KYB. Map governance to spending policies and ensure wallet operations and dispute rights are clearly assigned.

Do these rails expose extra PII because agents have emails and phone numbers?

Per-agent identity artifacts enable merchant verification flows but add data-handling obligations. Apply least-privilege access, rotate identifiers with lifecycle events, and ensure logs avoid storing raw OTPs or sensitive contents longer than necessary.

Is this viable for microtransactions under a few cents?

Card economics and authorization overhead can make ultra-small tickets inefficient. Consider batching, prepaid balances, or waiting until counterparties support direct on-chain settlement for those flows.

How do I prevent an agent from overspending during a model glitch?

Combine stacked controls: hard budget caps, per-transaction limits, merchant allowlists, velocity checks, human-in-the-loop approvals above thresholds, and real-time alerts. Kill switches should revoke tokens and disable the wallet instantly.

Disclaimer: This article is provided for informational purposes only. It is not offered or intended to be used as legal, tax, investment, financial, or other advice.

You May Also Like

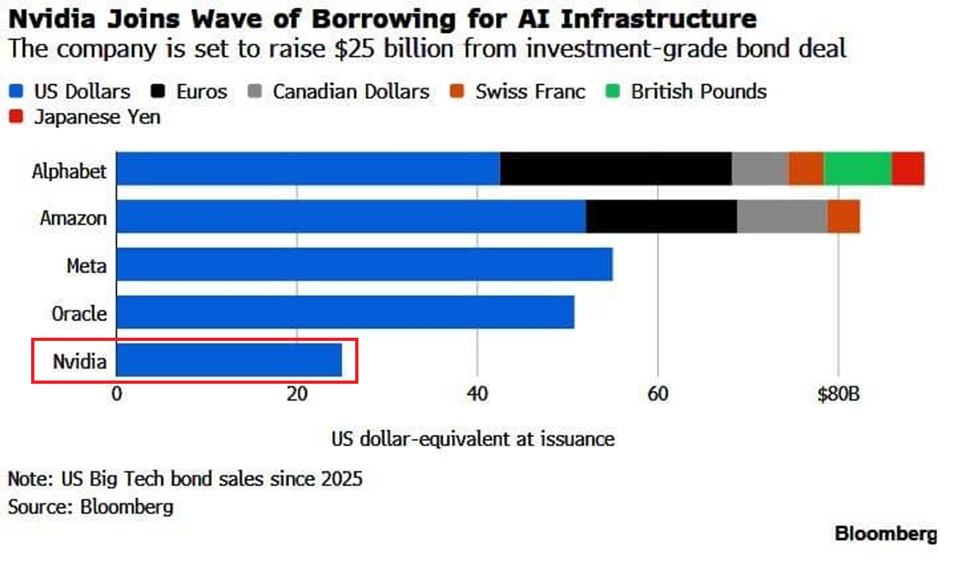

Nvidia Completes $25 Billion AI Debt Financing, Is NVDA Stock Ready for Next Rally?

Inside Trump's new weird obsession with the number 22

AI predicts XRP price for April 30, 2026