Macro Dilemma: Trade War, AI Bubble, and Political Rifts

Author: arndxt

Compiled by AididiaoJP, Foresight News

2025 is a turning point in the economic cycle.

The market is caught in a paradox.

Beneath the surface calm of soft landing optimism, the global economy is quietly fracturing, unfolding along the lines of trade policy, credit expansion and technological overextension.

The next dislocation in the global economy will not arise from a single failure—neither from tariffs nor from AI debt—but from feedback loops between policies, leverage, and beliefs.

We are witnessing the late stages of a supercycle, in which technology underpins growth, fiscal populism replaces trade liberalism, and trust in currency is slowly eroding.

The boom is not over yet, but it has begun to break.

This week's fluctuations are small but significant.

The Volatility Index experienced its biggest surge since April as concerns about US-China tariffs reignited, before retreating before the weekend following President Trump's confirmation that the proposed 100% import tariffs would be "unsustainable." Equity markets breathed a sigh of relief; the S&P 500 stabilized. However, this relief was superficial; the deeper narrative was one of exhausted policy tools and overstretched optimism.

The illusion of stability

The July US-EU trade agreement was intended to anchor a fragile system.

Yet it is now unravelling amidst the climate regulation controversy and US protectionism. Washington’s demand for US companies to be exempted from ESG and carbon disclosure rules highlights a growing ideological divide: decarbonisation in Europe versus deregulation in the US.

Meanwhile, new Chinese restrictions on rare earth exports, including a ban on magnets containing trace amounts of the metal from China, exposed strategic vulnerabilities in global supply chains. The US responded by threatening to impose a 100% tariff on Chinese imports, a political gesture with global consequences. Although the threat was later withdrawn, it served as a reminder to markets that trade has become weaponized finance, leveraging domestic sentiment rather than economic rationality.

The World Trade Organization’s warning of a sharp slowdown in goods trade by 2026 reflects a reality: companies are no longer investing in supply chains with confidence but with contingency plans.

AI Super Cycle

Meanwhile, in the AI economy, a second narrative is unfolding that is more subtle but potentially more consequential.

We are crossing from productive expansion to speculative finance, where "supplier financing is surging and coverage is thinning." Hyperscale companies are now leveraging their balance sheets faster than their revenues can justify, a classic sign of late-cycle exuberance.

This is nothing new. Of the 21 major investment booms since 1790, 18 have ended in collapse, usually when the quality of financing deteriorated. Today's AI capital spending frenzy resembles the telecom bubble of the late 1990s: real infrastructure gains entangled with credit-fueled speculation. Special purpose vehicles, vendor financing, and structured debt—the tools that once inflated mortgage-backed securities—are making a comeback, this time disguised as "computing power" and "GPU liquidity."

The irony? The AI boom is productive, just unevenly distributed. Microsoft financed its expansion with traditional bonds, a sign of confidence. CoreWeave, through a special purpose vehicle, a sign of stress. Both are expanding, but one is building enduring capabilities; the other is building fragility.

Fluctuating symptoms

The surge in the VIX reflects deeper market unease: policy uncertainty, concentrated equity leadership, and credit stress beneath a veneer of booming valuations.

When the Fed now signals rate cuts amid slowing growth, it's not stimulus, it's risk management. The two-year Treasury yield, which has fallen to its lowest level since 2022, tells us that investors are pricing in a deflation of confidence, not just interest rates. Markets may still cheer every dovish turn, but every rate cut undermines the illusion that growth is self-sustaining.

General: Trade, Technology and Trust

The connecting thread between tariff politics and the excitement over AI is trust, or more precisely, the erosion of trust.

The government no longer trusts its trading partners.

Investors no longer trust policy consistency.

Companies no longer trust demand signals, so they overbuild.

Gold's breakout above $4,000 isn't so much about inflation as it is about the erosion of faith in the fiat currency system, in globalization, and in institutional coordination. It's a hedge, not against price inflation, but against policy entropy.

The Road Ahead

We are entering a “fractured boom”: a period of nominal growth and market highs juxtaposed with structural vulnerabilities:

AI investments will drive GDP in the same way that railroads did in the 19th century.

Trade protectionism stimulates local production while draining global liquidity.

Financial volatility oscillates between euphoria and policy panic.

At this stage, risks are cumulative.

Every tariff rollback, every capital spending announcement, every rate cut prolongs the cycle but compresses its eventual collapse. The question is not whether the AI or trade bubble will burst, but how intertwined the two have become when they do.

You May Also Like

Why this former OpenAI researcher thinks it’s time to start gaming out AI’s future

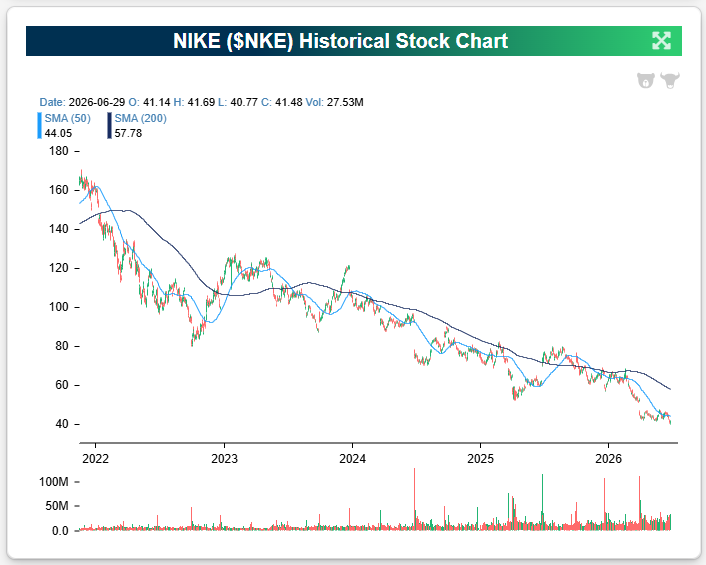

Nike (NKE) – Can the Swoosh Recover?