Why Bitcoin Lacks the Staying Power of Gold

Table of Links

- Introduction/Abstract

- The Blockchain

- Vulnerability of Revenue-Free Bubbles

- Success in Wrong Places

- Principles for a Currency

- The Difficult with Inflation Hedges

- Some Additional Fallacies

- Conclusion and References

VULNERABILITY OF REVENUE-FREE BUBBLES

A central result (even principle) in the rational expectations and securities pricing literature is that, thanks to the law of iterated expectations, if we expect now that we will expect the price to vary at some point in the future, then by backward induction such a variation must be incorporated in the price now. When there are no dividends, as with growth companies, there is still an expectation of future earnings, and a future expected reward to stockholders — directly via dividends, or indirectly via reverse dilutions and buybacks. It remains that a stock is a claim on accumulated assets and their residual value.

\ Earnings-free assets with no residual value are problematic.

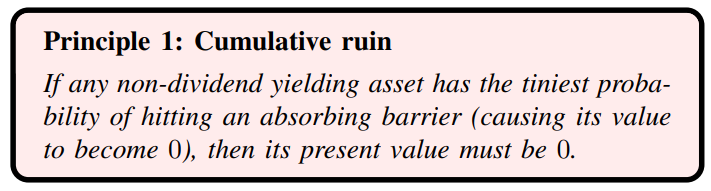

\ The implication is that, owing to the absence of any explicit yield benefitting the holder of bitcoin, if we expect that at any point in the future the value will be zero when miners are extinct, the technology becomes obsolete, or future generations get into other such "assets" and bitcoin loses its appeal for them, then the value must be zero now[3].

\ The typical comparison of bitcoin to gold is lacking in elementary financial rigor[4]. We will see below how precious metals lost their quality as a medium of exchange; gold and other dividend-free precious items (such as other metals or stones) have held some financial status for more than 6, 000 years, and their physical status for several orders of magnitude longer (i.e., they did not degrade or mutate into some other alloy or mineral). So one can expect one’s gold or silver possessions to be around physically for at least the next millennium, as well as having some residual economic value by iteration, for the same reason. Metals have ample industrial uses with demand elasticity (and substitution for other raw materials). Currently, about half of gold production goes to jewelry (for which there are often no storage costs), one tenth to industry, and a quarter to central bank reserves.

\ Path dependence is a problem. We cannot expect a book entry on a ledger that requires active maintenance by interested and incentivized people to keep its physical presence, a condition for monetary value, for any period of time — and of course we are not sure of the interests, mindsets, and preferences of future generations. Once bitcoin drops below a certain threshold, it may hit an absorbing barrier and stays at 0 — gold on the other hand is not path dependent in its physical properties[5]. As discussed in [7], technologies tend to be supplanted by other technologies with a vulnerability in proportion to their past survival duration (>99% of the new is replaced by something newer), whereas items such as gold and silver have proved resistant to extinction. Furthermore bitcoin is supposed to be hacker-proof and is based on total infallibility in the future, not just at present. It is crucial that bitcoin is based on perfect immortality; unlike conventional assets, the slightest mortality rate puts its value at 0[6].

\

\ We exclude collectibles from that category, as they have an aesthetic utility as if one were, in a way, renting them for an expense that maps to a dividend — and thus are no different from perishable consumer goods. The same applies to the jewelry side of gold: my gold necklace may be worth 0 in thirty years, but then I would have been wearing it for six decades.

\ The difference between the current bitcoin bubble and past recent ones, such as the dot-com episode spanning the period over 1995-2000, is that shell companies were at least promising some type of future revenue stream. Bitcoin would be allowed to escape a valuation methodology had it proven to be a medium of exchange or satisfied the condition for a numeraire from which other goods could be priced. But currently it is not, as we will see next.

\

SUCCESS IN WRONG PLACES

More generally, the fundamental flaw and contradiction at the base of most cryptocurrencies is, as we saw, that the originators, miners, and maintainers of the system currently make their money from the inflation of their currencies rather than just from the volume of underlying transactions in them. Hence the total failure of bitcoin to become a currency has been masked by the inflation of the currency value, generating (paper) profits for a large enough number of people to enter the discourse well ahead of its utility.

\

\ Transactions in bitcoin are considerably more expensive than wire services or other modes of transfers, or ones in other cryptocurrencies[7]. They are order of magnitudes slower than standard commercial systems used by credit card companies —anecdotally, while you can instantly buy a cup of coffee with your cell phone, you would need to wait ten minutes if you used bitcoin[8]. They cannot compete with African mobile money.[9]. Nor can the system outlined above —as per its very structure —accommodate a large volume of transactions — which is something central for such an ambitious payment system.

\ To date, twelve years into its life, in spite of all the fanfare, but with the possible exception of the price tag of Salvadoran permanent residence (3 bitcoins), there are currently no prices fixed in bitcoin floating in fiat currencies in the economy.

\

:::info Author:

(1) Nassim Nicholas Taleb, Universa Investments, Tandon School of Engineering, New York University Forthcoming, Quantitative Finance.

:::

:::info This paper is available on arxiv under CC BY 4.0 DEED license.

:::

\ [5] The absorbing barrier does not have to be 0 for the price to spiral to 0 upon hitting the barrier. This is similar to saying "if the heart rate drops below ten beats per minutes, it will be 0 (death)" — nor does it necessarily have to be caused by a drop in price. Nor does it have to be endogenous.

\ [6] To counter the effect of the absorbing barrier, the asset must grow at an exponential rate forever, without remission, and with total certainty. Belief in such an immortality for BTC — and its total infallibility — is in line with the common observation that its enthusiastic investors have the attributes of a religious cult

\ [7] Transactions in bitcoin are orders of magnitude more expensive than those done using African mobile phones.

\ [8] "As it grew in popularity, Bitcoin became cumbersome, slow, and expensive to use. It takes about 10 minutes to validate most transactions using the cryptocurrency and the transaction fee has been at a median of about $20 this year." By Eswar Prasad, New York Times, Jun 15, 2021.

\ [9] There appear to be other protocols issued from the original white paper that claim to be more transaction focused; as with Ethereum, we exclude them from this analysis.

You May Also Like

OpenAI Calls for Global Shift in Taxation, Labor Policy as AI Takes Over

Oklo (OKLO) Stock: Top Execs Dump $21M in Shares Amid Cramer Criticism and Earnings Disappointment