Arm Holdings Is Up 111% Over the Past Year. Here’s Whether the AI Rally Still Has Room to Run

Key Stats for ARM Stock

- Past week’s performance: -18%

- 52-week range: $100 to $453

- Valuation model target price: $546

- Implied upside: +56.9% over the next 2.8 years

Explore Arm’s full valuation model, and analyst estimates on TIKR (It’s free) >>>

The Chip Rally Finds Arm at the Center of a Structural Shift

Arm Holdings (ARM) caught a fresh updraft on June 25 when Micron and Qualcomm both issued forecasts that ignited a $400 billion AI chip stock rally across the sector. Qualcomm’s projection of $15 billion in data center chip sales by 2029 was particularly relevant for Arm, because Qualcomm designs its server chips using Arm’s CPU architecture. Every data center chip that Qualcomm ships generates a royalty for Arm.

That royalty model is ARM’s defining business characteristic. Arm does not manufacture chips. Instead, it designs processor architectures and licenses them to semiconductor companies, including Apple, Qualcomm, Samsung, and Nvidia. Chip designers pay Arm an upfront license fee and then a per-chip royalty every time a device ships. As AI drives a new wave of custom chip design across cloud providers and data center operators, Arm sits in the middle of virtually every major new compute platform.

Arm’s CEO confirmed in early June that both ByteDance and Oracle are using Arm-designed data center CPU chips. The company also stated that the U.S. would have significant difficulty banning exports of AI CPU chips to China, suggesting that Arm’s architecture is now deeply embedded in global compute infrastructure. Those comments came as Arm introduced its own Arm-designed data center CPU, the Arm AGI CPU, specifically for agentic AI infrastructure at the company’s product event in late March.

ARM Revenues and Net Income (TIKR)

ARM Revenues and Net Income (TIKR)

Full-year fiscal 2026 results reported in May showed revenue climbing 23% to $4.92 billion and net income rising 14% to $904 million. Going forward, whether ARM stock can hold its gains depends on whether data center royalty revenue expands fast enough to justify a valuation that remains one of the most stretched in all of semiconductors.

See analysts’ growth forecasts and price targets for ARM (It’s free) >>>

Is Arm Stock Worth Buying at 160x Forward Earnings?

ARM Guided Valuation Model (TIKR)

ARM Guided Valuation Model (TIKR)

Under valuation model assumptions realized through 12/31/28, the stock is modeled using:

- Revenue growth (CAGR): 29.4%

- Operating Margins: 46.5%

- Exit P/E Multiple: 108.4x

Based on these inputs, the model estimates a target price of $546, implying 56.9% total upside from the current share price and a 17.7% annualized return over the next 2.8 years.

A 17.7% annualized return clears the threshold for what makes a stock attractive, but only just. The model demands belief in several high-conviction assumptions simultaneously. A 29.4% revenue CAGR through fiscal 2029 would require Arm to nearly triple its top line from fiscal 2026’s $4.92 billion. That trajectory is plausible given the royalty engine’s leverage to AI chip volume, but it depends on sustained chip production growth across every major semiconductor customer.

ARM Guided Valuation Model (TIKR)

ARM Guided Valuation Model (TIKR)

The 46.5% operating margin assumption is actually conservative relative to Arm’s current LTM EBIT margin of 18.5%. The gap between today’s 18.5% and the modeled 46.5% reflects how much of Arm’s current cost structure is still growing headcount and R&D investment to support the AGI CPU and new architecture work. As those investments mature and royalty revenue scales, margins should expand materially because the royalty business has near-zero marginal cost.

The 108.4x exit P/E multiple is where the model’s internal tension lives. Even after the rally, ARM trades at a trailing P/E above 400x. The model assumes significant multiple compression to 108x by 2029. That compression is realistic only if earnings growth is so rapid that it shrinks the multiple organically rather than through a valuation re-rating.

Stress-test the ARM valuation model and compare against analysts’ forecasts on TIKR >>>

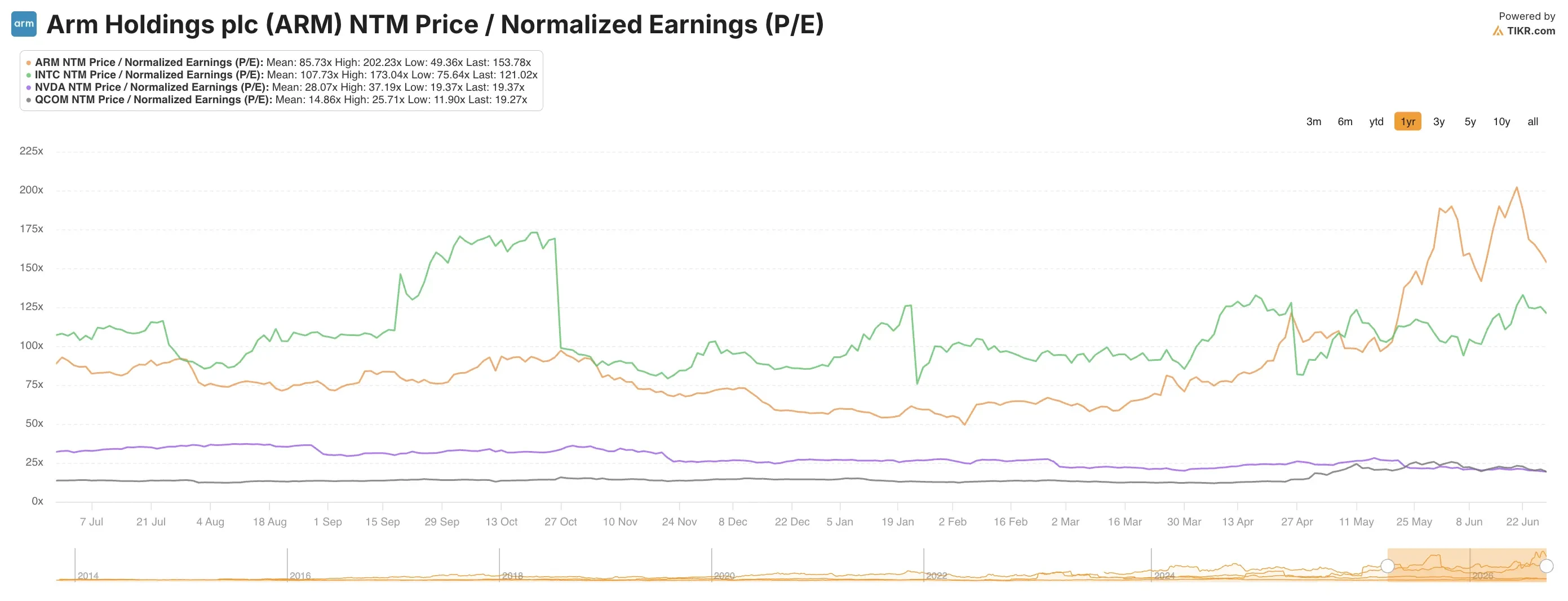

How ARM Compares to Nvidia, Intel, and Qualcomm

Arm’s competitive comparison is unusual because it is both a partner to and a potential competitor of every major semiconductor company. NVIDIA (NVDA) designs its Grace Hopper and Blackwell CPUs on Arm architecture and pays Arm royalties. Qualcomm (QCOM) builds Snapdragon and Oryon chips on ARM licenses. Apple’s entire chip lineup, from the M-series Mac chips to the A-series iPhone processors, runs on Arm architecture.

NVIDIA trades at roughly 35x to 40x forward earnings, which looks inexpensive next to ARM’s 160x NTM P/E. But Nvidia’s revenue is nearly 15 times larger than Arm’s, and Nvidia owns its own chip manufacturing relationships and ecosystem. Intel (INTC) and AMD both trade at substantially lower multiples, reflecting margin pressure and competitive challenges in the CPU market that Arm does not face because it licenses rather than competes directly.

ARM NTM P/E vs INTC and NVDA vs QCOM (TIKR)

ARM NTM P/E vs INTC and NVDA vs QCOM (TIKR)

The antitrust probe reported by Bloomberg in May adds a risk layer. U.S. regulators are reportedly examining whether Arm’s licensing practices give it anti-competitive leverage over chip designers. That inquiry could slow the expansion of Arm’s royalty rates, which are the key driver of future revenue per chip. South Korean regulators have also inspected Arm’s Seoul office, signaling that scrutiny is not limited to the U.S.

Qualcomm’s June forecast of $15 billion in data center chip sales by 2029 is perhaps the single most bullish external validation of Arm’s data center royalty thesis. If Qualcomm ships that volume of Arm-based server chips, the royalty stream alone could represent a material step-up in Arm’s revenue base.

Find out why investors are still watching Arm carefully despite the AI chip surge >>>

What’s Driving ARM Stock Going Forward?

The data center CPU royalty ramp is the dominant forward catalyst. Arm’s AGI CPU, designed specifically for agentic AI workloads, is positioned to capture royalties from cloud providers building the next generation of AI inference infrastructure. Agentic AI refers to systems that can take autonomous actions and run complex, multi-step workflows, which require more sustained compute than simple text generation tasks.

The royalty rate per chip is also increasing. As chip designers move toward more sophisticated Arm architectures with higher royalty tiers, the revenue per device shipped grows even if unit volumes stay flat. That mix shift toward high-royalty premium architectures is a structural tailwind that does not require overall chip market growth to deliver revenue upside.

Meta’s multi-year strategic partnership with Arm, announced in late 2025, signals that the largest AI infrastructure builders are embedding Arm architecture deep into their custom chip roadmaps. Custom silicon, meaning chips designed by tech companies specifically for their own AI workloads, carries higher royalty rates than standard licensing because it uses more of Arm’s proprietary IP. Meta, Microsoft, Google, and Amazon are all building custom AI chips, and all of them are doing so on Arm architecture.

Arm’s Q1 fiscal 2027 results are expected on July 29. The forward guidance issued alongside those results will be the most important near-term signal for the stock. An upward revision to the royalty revenue trajectory would confirm that the AI data center demand wave is flowing through to Arm’s income statement faster than consensus expects.

Estimate a company’s fair value instantly (Free with TIKR) >>>

Should You Invest in Arm Holdings?

The only way to really know is to look at the numbers yourself. TIKR gives you free access to the same institutional-quality financial data that professional analysts use to answer exactly that question.

Pull up ARM, and you’ll see years of historical financials, what Wall Street analysts expect for revenue and earnings in the quarters ahead, how valuation multiples have moved over time, and whether price targets are trending up or down.

You can build a free watchlist to track ARM alongside every other stock on your radar. No credit card required. Just the data you need to decide for yourself.

Analyze ARM stock on TIKR Free→

Looking for New Opportunities?

- See what stocks billionaire investors are buying so you can follow the smart money.

- Analyze stocks in as little as 5 minutes with TIKR’s all-in-one, easy-to-use platform.

- The more rocks you overturn… the more opportunities you’ll uncover. Search 100K+ global stocks, global top investor holdings, and more with TIKR.

Disclaimer:

Please note that the articles on TIKR are not intended to serve as investment or financial advice from TIKR or our content team, nor are they recommendations to buy or sell any stocks. We create our content based on TIKR Terminal’s investment data and analysts’ estimates. Our analysis might not include recent company news or important updates. TIKR has no position in any stocks mentioned. Thank you for reading, and happy investing!

Ayrıca Şunları da Beğenebilirsiniz

A deep red state launched a surprising revolt against major conservative cause

An Inherited IRA Quietly Adds Hundreds to Your Monthly Medicare Premium.

Johnson & Johnson’s $5 Billion INLEXZO Bet: What Will Happen If SunRISe-3 Delivers in 2027

Popüler Haberler

Daha fazla