Astera Labs Rose 5% Today. Here’s Why 2026 Could Test the Rally

Key Stats for Astera Labs Stock

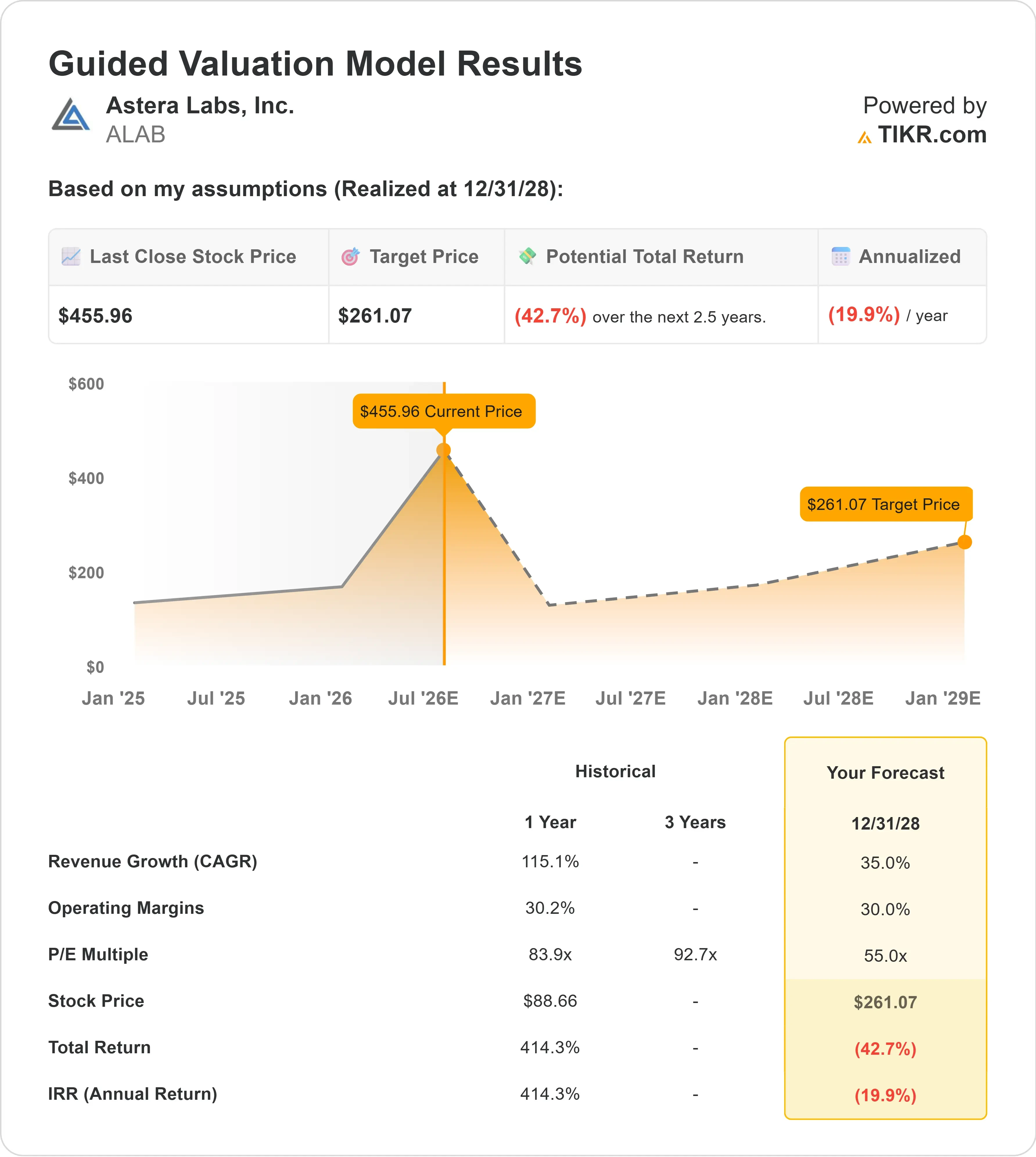

- Today’s Performance: 5%

- 52-Week Range: $86 to $457

- Valuation Model Target Price: around $260

- Implied Downside: around 43%

Analyze your favorite stocks like Astera Labs with TIKR (It’s free) >>>

What Happened?

Astera Labs stock rose about 5% today, trading near $456 per share, as investors continued to chase one of the market’s clearest AI infrastructure stories. The company is being treated as a key connectivity supplier for AI data centers, where faster data movement between chips, memory, networking equipment, and storage is becoming more important as hyperscalers build larger GPU and XPU clusters.

The stock moved higher because investors focused on stronger analyst confidence, Astera’s Nasdaq-100 inclusion, and continued demand for AI connectivity products that sit at the center of today’s AI data center buildout. Stifel’s price target has recently moved as high as around $460, while TIKR market data shows the Street target near $270, signaling that Wall Street has become more constructive on the business even though the average target remains far below the current share price. Astera also joined the Nasdaq-100 before the market opened on June 22, 2026, a milestone that can increase visibility and demand from index-tracking funds while AI infrastructure stocks remain a major market focus.

Astera’s latest results gave the rally a stronger fundamental base. The company reported record Q1 revenue of $308 million, up 93% year over year and 14% sequentially, while non-GAAP EPS reached $0.61 as demand remained strong across its PCIe 6 AI fabric and signal conditioning portfolio. These products help AI systems move data faster and more reliably, which matters as AI clusters grow larger and require more advanced connectivity inside and between servers.

At the recent Evercore Global TMT Conference, management highlighted continued momentum in AI connectivity. CFO Desmond Lynch said Scorpio became Astera’s fastest-growing product line last year and represented about 15% of total revenue, while its 320-lane scale-up solution is expected to enter volume production in the second half of 2026. Lynch also said Scorpio could become Astera’s largest product line by year-end, supported by a $4 billion scale-out opportunity, a $10 billion scale-up opportunity, and two hyperscalers contributing to P-Series revenue in the second half. “Our goal is to grow faster than the market,” said Nicholas Aberle, Senior Vice President of Finance and Head of Investor Relations.

The competitive setup also explains why the market is paying attention. Broadcom remains the larger AI networking and custom accelerator benchmark, with Q1 AI revenue of about $8 billion, up 106% year over year, while Credo is another fast-growing data center connectivity peer after reporting quarterly revenue of $437 million, up 157% year over year. Against rivals such as Broadcom, Marvell, Nvidia, and Credo, Astera has a smaller revenue base but more direct exposure to AI connectivity growth, which gives the stock a powerful upside story while also making valuation expectations harder to meet.

Astera Labs Guided Valuation Model

Astera Labs Guided Valuation Model

Value Astera Labs instantly (Free with TIKR) >>>

Is Astera Labs Overvalued?

Under valuation assumptions, the stock is modeled using:

- Revenue Growth: around 35%

- Operating Margins: around 30%

- Exit P/E Multiple: 55x

Astera Labs is delivering exceptional growth because AI servers need faster connectivity across accelerators, memory, networking equipment, and storage.

Its Scorpio switches, Aries retimers, Taurus Smart Cable Modules, and COSMOS software help solve that problem by improving how data moves inside large AI systems, which becomes more valuable as clusters scale from single servers into full racks and multi-rack deployments.

Astera Labs Revenue & Analyst Growth Estimates Over Five Years

Astera Labs Revenue & Analyst Growth Estimates Over Five Years

See analysts’ growth forecasts and price targets for American Electric Power (It’s free) >>>

The model already assumes strong execution, including around 35% revenue growth, around 30% operating margins, and a premium 55x exit P/E multiple, but the estimated target price is still only around $260, implying about 43% downside from the current price near $456.

That means ALAB does not look cheap, even though the company’s AI infrastructure exposure and product momentum remain impressive.

At current levels, Astera Labs appears overvalued based on this model, with future returns depending on whether PCIe 6 adoption, Scorpio scale-up deployments, hyperscaler customer wins, and operating leverage can become strong enough to justify one of the highest valuations in semiconductors.

How Much Upside Does ALAB Stock Have From Here?

Investors can estimate Astera Labs’ potential share price, or what any stock could be worth, in under a minute using TIKR’s New Valuation Model tool.

All it takes is three simple inputs:

- Revenue Growth

- Operating Margins

- Exit P/E Multiple

From there, TIKR calculates the potential share price and total returns under Bull, Base, and Bear scenarios so you can quickly see whether a stock looks undervalued or overvalued.

If you’re not sure what to enter, TIKR automatically fills in each input using analysts’ consensus estimates, giving you a quick, reliable starting point.

Value Astera Labs in under 60 seconds with TIKR (It’s free) >>>

Ayrıca Şunları da Beğenebilirsiniz

Q2 Market Insights: Bitcoin regains dominance in risk-averse environment, ETFs remain critical to market structure

Canada Exports increased to $66.31B in February from previous $62.48B