Ripple’s dollar stablecoin hits a wall in Japan, one of XRP’s friendliest markets, as megabanks earn most of the trust

Japan has long been one of Ripple's most fertile markets. SBI's investment in Ripple dates to 2016, SBI Remit launched Japan's first XRP-enabled international remittance flow in 2021, and SBI VC Trade counts XRP among its most popular assets.

When Ripple and SBI announced in August 2025 that SBI VC Trade intended to distribute RLUSD in Japan, the move read as a natural extension of an already deep local partnership.

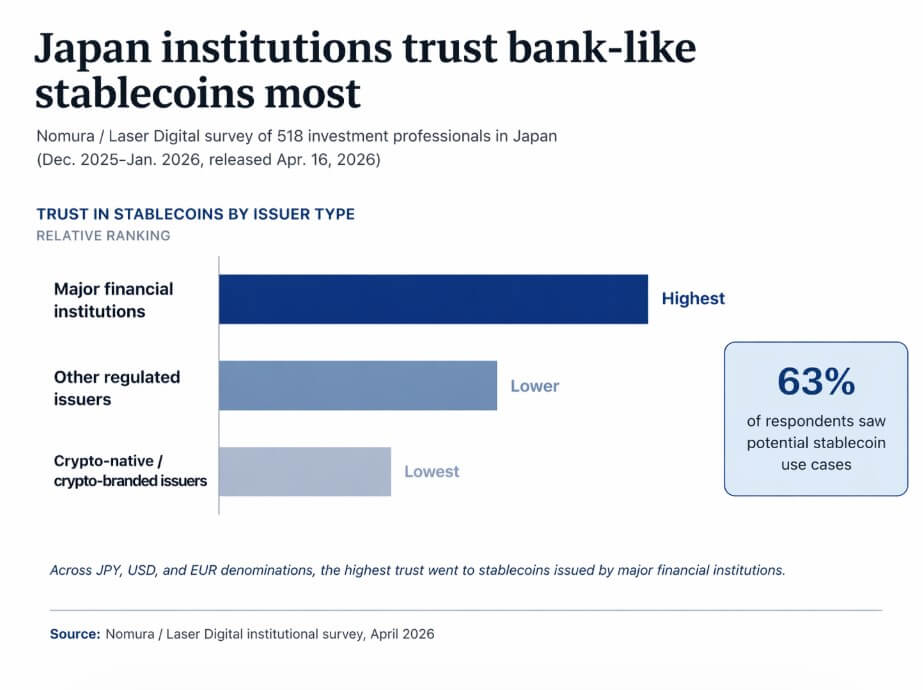

A recent survey of 518 investment professionals in Japan, conducted by Nomura and Laser Digital between December 2025 and January 2026 and released Apr. 16, found that 63% of respondents identified potential uses for stablecoins, spanning treasury management, cross-border payments, crypto investing, and tokenized securities.

Across JPY, USD, and EUR denominations, the stablecoins that drew the highest institutional trust were those issued by major financial institutions.

Japan may be Ripple's friendliest proving ground and precisely where the limits of crypto-branded stablecoins become visible.

A Nomura and Laser Digital survey of 518 Japanese investment professionals found major financial institution-issued stablecoins ranked highest in trust, with crypto-native issuers ranking lowest.

A Nomura and Laser Digital survey of 518 Japanese investment professionals found major financial institution-issued stablecoins ranked highest in trust, with crypto-native issuers ranking lowest.

Why Japan was supposed to be different

Ripple's position in Japan goes beyond standard distribution agreements. SBI Ripple Asia, a joint venture formed from SBI's 2016 investment in Ripple, has operated as part of Ripple's regional infrastructure for nearly a decade.

SBI Remit began using Ripple Payments in 2017 and expanded XRP-based remittance corridors into the Philippines, Vietnam, and Indonesia in September 2023.

SBI VC Trade's own investor materials describe XRP as one of its most popular crypto assets among customers.

That foundation gave Ripple something most stablecoin issuers lack in Japan, which is pre-existing retail familiarity, regulated local partners, and a remittance infrastructure already operating on Ripple rails.

RLUSD entered this market with institutional packaging that Ripple itself describes as enterprise-grade, fully backed by US dollar deposits, US government bonds, and cash equivalents, built around compliance and integrated into Ripple Payments for cross-border and treasury-style flows.

Nomura's survey complicates the read that puts Ripple in a strong hand. The trust premium that Japanese institutions place on major financial institution issuers reflects a structural bias toward familiar, supervised counterparties.

The FSA's stablecoin framework limits issuance of digital-money-type stablecoins to banks, fund transfer service providers, and trust companies, with redemption and safeguarding requirements attached to each structure.

Bank-issued stablecoins offer protection equivalent to that of conventional bank deposits. Japan's regulatory architecture, by design, concentrates credibility around supervised financial entities. Ripple, regardless of its compliance posture, falls outside that category.

The competition already building

RLUSD's planned distribution through SBI VC Trade, still described in late 2025 SBI investor materials as pending approval, falls within a field that Japan's established financial institutions are actively developing.

In November 2025, MUFG Bank, Mizuho Bank, SMBC, and Mitsubishi UFJ Trust and Progmat announced an FSA-supported proof of concept for joint stablecoin issuance and cross-border settlement.

SBI's own materials show that USDC is already approved in Japan through its relationship with Circle, that RLUSD is planned for listing once approval is cleared, and that a JPY-pegged stablecoin study is underway with SMBC.

That competitive picture reframes what RLUSD is actually competing for in Japan.

| Use case / market lane | Likely trust advantage |

|---|---|

| Cross-border payments | RLUSD / Ripple-linked infrastructure |

| International remittances | RLUSD / Ripple-linked infrastructure |

| Exchange liquidity | RLUSD / crypto-linked issuers |

| Treasury management | Major financial institution issuers |

| Tokenized securities settlement | Major financial institution issuers |

| Domestic corporate payments | Major financial institution issuers |

The open question is which issuer types will capture the highest-trust, highest-value institutional use cases, as Nomura's 63% figure puts adoption itself beyond doubt.

Treasury management, tokenized securities settlement, and domestic corporate payments are the use cases most sensitive to issuer identity. Cross-border payments, exchange liquidity, and international remittances are the use cases where Ripple's existing infrastructure and RLUSD's design are strongest.

Ripple built its position in Japan through payments and remittances, and RLUSD's rollout plan points in the same direction. Nomura's trust data points to institutions reaching out to issuers with balance sheets and deposit protections they already recognize for broader use cases.

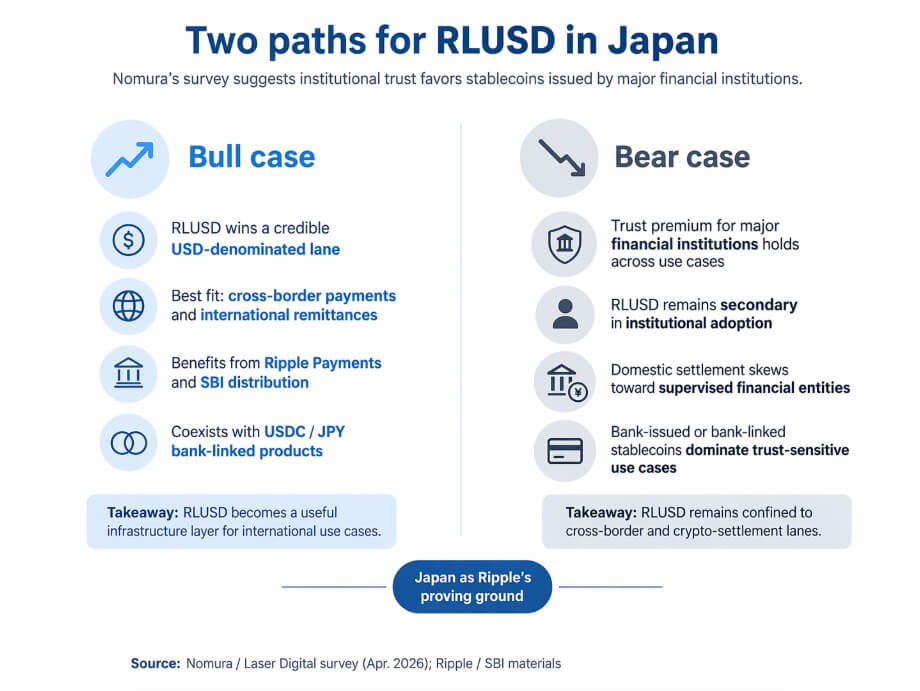

Two paths from here

The bull case for RLUSD in Japan depends on how narrowly institutions actually apply the trust premium captured by Nomura's survey.

If Japanese institutions draw a practical distinction between issuer identity for domestic yen-denominated settlement and issuer identity for USD-denominated cross-border infrastructure, RLUSD has a credible lane.

Ripple Payments already routes international flows, SBI VC Trade already serves institutional crypto clients, and RLUSD, as a compliant USD stablecoin integrated into an existing cross-border payment network, could occupy the USD settlement role in Japan's institutional stack without needing to win the domestic trust competition outright.

In that scenario, RLUSD becomes a credible infrastructure for international use cases, while SBI's parallel USDC and JPY stablecoins handle domestic demand.

Ripple's enterprise positioning would prove sufficient for the lanes it already occupies, even if it does not expand into the higher-trust domestic settlement business.

The bear case follows directly from Nomura's data and Japan's issuer structure.

If the trust premium for major financial institution issuers proves sticky across all stablecoin use cases, RLUSD will remain secondary in the Japanese institutional market regardless of its compliance credentials.

Banks and trust companies building their own stablecoin products carry the deposit-protection framing and regulatory familiarity that Nomura's respondents appear to prize.

RLUSD, however well-packaged, arrives as a crypto-network product distributed through a local partner. This is a structure that Japanese institutions may still read as crypto-adjacent, outside the supervised financial entity category that Nomura's trust premium rewards.

In that outcome, RLUSD's presence in Japan mirrors its global positioning as useful for Ripple Payments flows and exchange liquidity, with domestic institutional settlement concentrated among supervised financial entities.

That would be a meaningful ceiling even in Ripple's friendliest market.

RLUSD's bull case rests on cross-border payments; the bear case leaves it secondary to bank-linked stablecoins in Japan's institutional market.

RLUSD's bull case rests on cross-border payments; the bear case leaves it secondary to bank-linked stablecoins in Japan's institutional market.

Nomura's wording is “major financial institutions.” That distinction creates some space for non-bank-regulated issuers to compete on trust grounds, particularly fund transfer service providers and trust companies that fall within Japan's issuer-authorization framework.

The 63% use-case figure reflects current institutional thinking among asset managers, family offices, and public interest organizations.

That demand exists now, and it will flow toward products first. The open variable is which products capture the largest share of its trust-sensitive demand.

The broader frame

Ripple's position in Japan gives it an unusually useful vantage point on the stablecoin trust question.

If RLUSD finds a durable institutional foothold in Japan despite the trust premium Nomura's survey documents, that would demonstrate that compliance framing and local distribution can compete with issuer identity even in a bank-centered market.

If RLUSD stays confined to the cross-border and crypto-settlement lanes where Ripple already operates, that would confirm that trust in a payments network and trust in a stablecoin issuer are distinct, and that Japan's institutional market keeps them separate.

The megabank stablecoin buildout proceeding in parallel answers the same question from the other side. MUFG, Mizuho, and SMBC are building stablecoins with the intent of competing in the domestic trust market themselves.

Japan is a preview of what institutional stablecoin markets look like when the financial establishment arrives with its own products, its own issuer credibility, and a regulatory framework designed around its own structure.

The post Ripple’s dollar stablecoin hits a wall in Japan, one of XRP’s friendliest markets, as megabanks earn most of the trust appeared first on CryptoSlate.

You May Also Like

Thomas' 'historically illiterate' speech gets history 'wildly inaccurate': scholar

US Dollar Index Forecast: Critical Battle Below 98.50 as Nine-Day EMA Caps Rally