Snowflake Stock Crashed 56% and Then Nearly Fully Recovered. Here Is What the AI Data Cloud Is Actually Worth.

Key Stats for Snowflake Stock

- 52-Week Range: $118.30 – $284.99

- Current Price: $226.59

- Street Mean Target: ~$292

- TIKR Model Target: ~$657

- Q1 FY2027 Revenue: $1.39B (+33% YoY)

- Q1 FY2027 Product Revenue: $1.33B (+34% YoY)

- Net Revenue Retention: 126%

- Remaining Performance Obligations: $9.21B (+38% YoY)

Most investors never know if a stock is truly undervalued or overpriced. TIKR’s professional-grade valuation tools give you a clear, data-backed answer across 60,000+ stocks for free →

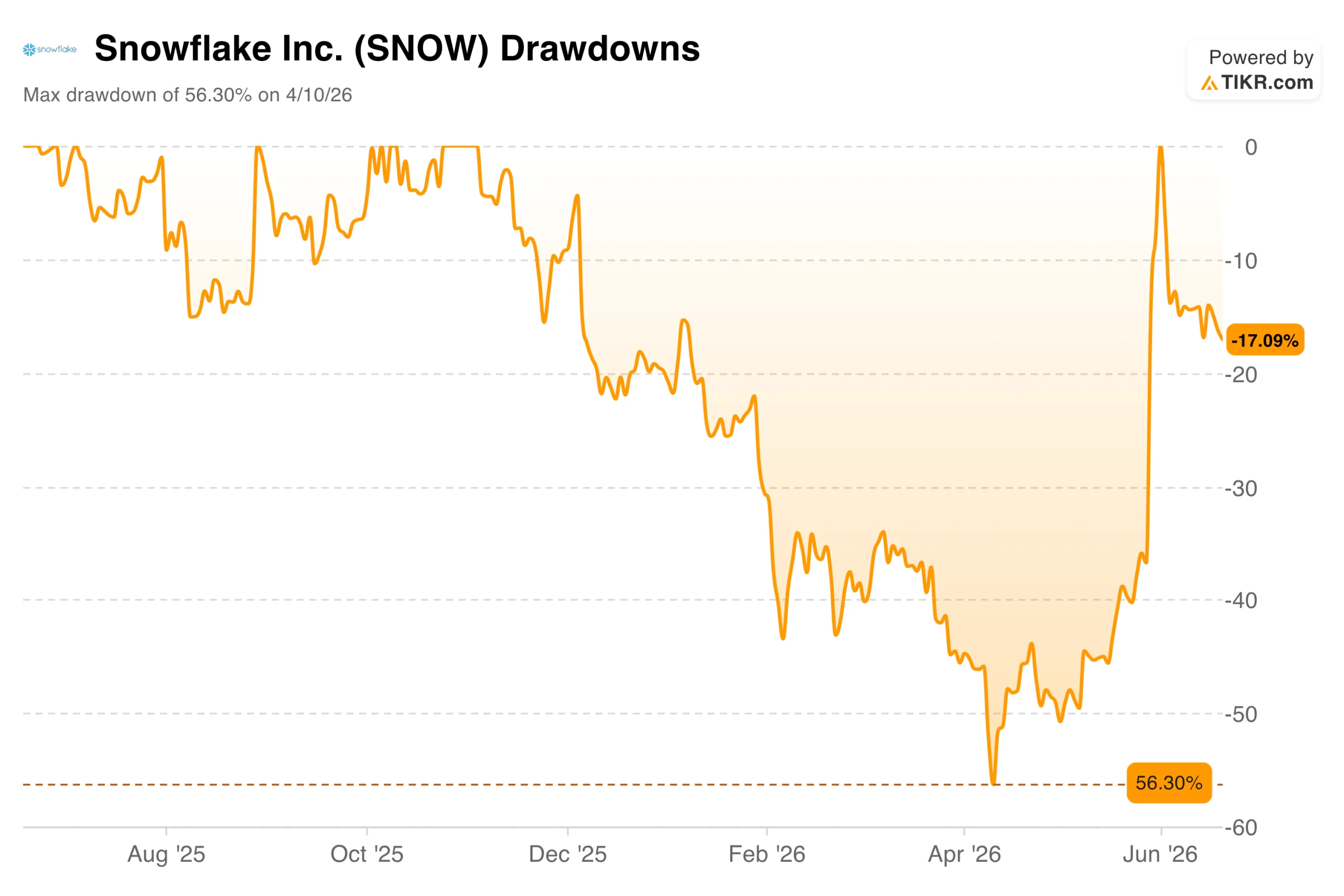

A 56% Drawdown and a Nearly Complete Recovery

Snowflake Inc. (SNOW) hit a 56% drawdown on April 10, falling from a 52-week high of $284.99 to $118.30 as the tariff sell-off swept through high-multiple software names indiscriminately. Then came Q1 fiscal 2027 earnings on May 27, and the stock nearly fully recovered. It now sits at $226.59, still about 17% below its peak but roughly double where it was six weeks earlier.

Snowflake Drawdowns. (TIKR)

Snowflake Drawdowns. (TIKR)

The earnings report that triggered the reversal was genuinely strong. Revenue of $1.39 billion grew 33% year over year, and product revenue of $1.33 billion grew 34%, which CEO Sridhar Ramaswamy called the strongest sequential dollar growth in the company’s history.

Net revenue retention of 126% confirms existing customers are spending more at an accelerating rate. Remaining performance obligations of $9.21 billion grew 38%, providing clear forward visibility. The company raised its full-year product revenue guidance to $5.84 billion, implying around 31% growth for the fiscal year.

Snowflake’s AI workload growth is moving fast, and the next consumption data point will tell you whether the inflection is holding. Track analyst estimate revisions and price target changes on SNOW in real time with TIKR for free →

Revenue Growing, Losses Narrowing, Cash Flowing

Snowflake’s model is built around consumption rather than subscriptions. Enterprise customers pay for the compute and storage they actually use, so revenue scales directly with the extent to which data and AI workloads are embedded in their operations. That model created explosive growth and early losses. It is now producing both.

Snowflake Total Revenues, Free Cash Flow. (TIKR)

Snowflake Total Revenues, Free Cash Flow. (TIKR)

Revenue grew from $592 million in fiscal 2021 to $4.68 billion in fiscal 2026, nearly eight times in five years. Free cash flow went from negative $80 million to positive $1.12 billion over the same period, a trajectory that answers the central question most bears have raised about the business.

The AI tailwind is accelerating that arc. Snowflake Intelligence, the company’s agentic AI layer that allows enterprises to query and act on their data using natural language, more than doubled its account base quarter over quarter, while Cortex Code, which brings AI-assisted data engineering directly into the platform, is already in use across more than 7,100 accounts. Together, these AI products are now embedded across more than 13,600 accounts on the platform.

The GAAP picture remains deeply negative, with an operating margin of roughly -26%, driven primarily by stock-based compensation. Investors should understand that the cash flow story and the GAAP income statement tell very different stories about the same business.

See historical and forward estimates for Snowflake stock (It’s free!) >>>

What Does the Valuation Model Say?

TIKR’s valuation model targets around $657 for Snowflake Inc. stock, with an approximately 25% annualized return through fiscal 2031, assuming mid-case revenue growth of around 21% and net income margins of around 14%.

That target is more than double the Street mean of around $292, which reflects a meaningfully different time horizon. The Street consensus is anchored to near-term price targets, while the TIKR model compounds over a decade of growth assumptions.

Snowflake Valuation Model. (TIKR)

Snowflake Valuation Model. (TIKR)

The scenario range is wide. The low case lands at around $851, with roughly 16% annualized, while the high case reaches around $1,726, with roughly 26% annualized. Even the low case implies strong returns, which is unusual.

The driver in every scenario is earnings growth, with the P/E compressing only modestly as the business matures. The key assumptions to watch are whether revenue growth can sustain above 20% through fiscal 2028 and whether non-GAAP margins continue expanding toward the mid-teens.

Should You Invest in Snowflake Inc.?

Snowflake is a business where the bear case and the bull case share the same facts and reach opposite conclusions. Bears point to a deeply negative GAAP operating margin, a 109 times forward earnings multiple, and a consumption model exposed to enterprise budget cuts. Bulls point to 34% product revenue growth, 126% net revenue retention, $1.12 billion in annual free cash flow, and an AI platform embedding itself deeper into enterprise operations every quarter.

The drawdown chart captures something real about this stock: it will regularly test your conviction and eventually reward it.

Put up Snowflake Inc. stock and access years of historical financials, what Wall Street analysts expect for revenue and earnings in the quarters ahead, and how the valuation compares to peers at TIKR for free.

See how Snowflake performs against its peers in TIKR (It’s free!) >>>

Looking for New Opportunities?

- See what stocks billionaire investors are buying so you can follow the smart money.

- Analyze stocks in as little as 5 minutes with TIKR’s all-in-one, easy-to-use platform.

- The more rocks you overturn… the more opportunities you’ll uncover. Search 100K+ global stocks, global top investor holdings, and more with TIKR.

Disclaimer:

Please note that the articles on TIKR are not intended to serve as investment or financial advice from TIKR or our content team, nor are they recommendations to buy or sell any stocks. We create our content based on TIKR Terminal’s investment data and analysts’ estimates. Our analysis might not include recent company news or important updates. TIKR has no position in any stocks mentioned. Thank you for reading, and happy investing!

You May Also Like

UK crypto holders brace for FCA’s expanded regulatory reach

Thinking of Buying Bittensor? Watch These TAO Price Correction Levels First

China Nabs Another Huione Group Core Member in Cambodia Extradition