Turkey Advances Crypto Tax Plans in New Era of Fiscal Oversight: Details

Key Insights:

- Turkey proposes a 0.03% transaction tax and 10% quarterly levy on net crypto profits.

- The goal of loss deductions and the FIFO method is to standardize reporting of cryptocurrency gains.

- Bill grants the president authority to adjust rates as crypto enters a formal tax regime.

Turkey is moving to a taxation system of digital assets with new legislation under consideration. Legislative representatives presented the crypto bill that promised a shift towards systematic fiscal control to the Turkish Grand National Assembly. The proposal introduces transaction fees and profit withholding on a single system. This development marks a significant step toward defining the crypto tax landscape in the country.

Turkey Crypto Tax Bill Introduces Dual System

According to Fintables Kripto, the proposal provides a dual-revenue tax system for digital assets. The system combines transaction-based charges with the profit withholding requirement. This proposal incorporates cryptocurrency activity into the current financial processes, minimizing regulatory ambiguity through compliance standards.

SOURCE: X

SOURCE: X

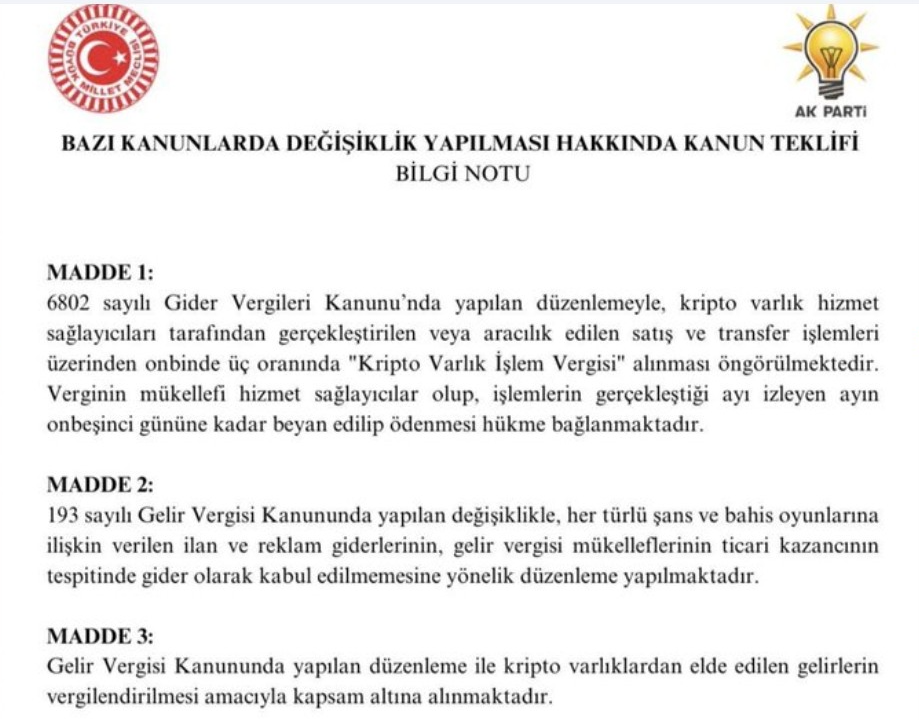

One immediate measure includes a 0.03% transaction levy on crypto sales or transfers. The charge applies at execution and is withheld automatically by exchanges. Although individually small, repeated transactions may create cumulative costs. This mechanism resembles a financial transaction tax rather than capital gains treatment.

Additionally, the draft introduces a 10% quarterly withholding on net trading profits. Gains are calculated using the First In, First Out (FIFO) accounting method. Investors may deduct same-year losses and trading commissions. This structure provides standardized reporting within the emerging crypto tax framework.

The proposal also grants the executive authority to adjust applicable rates depending on policy objectives. Implementation would begin two months after official publication. The crypto bill establishes a flexible but structured fiscal model.

Parliament Advances Crypto Bill Regulatory Scope

Meanwhile, lawmakers are reviewing broader regulatory components linked to digital asset taxation. The proposal will be to officially categorize cryptocurrency income under the national financial law. Trading profits, token swaps, and some yield mechanisms are subject to taxable activity. The framework places the crypto tax law in line with the current income structures.

SOURCE: X

SOURCE: X

In addition, the crypto bill presents compliance requirements to domestic service providers. Trades should be registered with the authorities and transactions should be transparent. Reporting standards are consistent with the anti-money laundering regulations. The provisions aim to bring digital finance closer to the formal economy in Turkey.

The technical definitions in the proposal are still under review by parliamentary committees. Moreover, there is a discussion about how staking rewards and earnings from blockchains should be classified. The legislators want to understand the way to include such income in the current fiscal categories. This is a legislative process that shows a holistic modernization of regulation.

Moreover, the policymakers state that the initiative is a measure of governance alignment and not a restriction on the market. Authorities focus on openness and integration of the financial system. By introducing formalized reporting requirements, the authorities aim to maintain consistent control over digital asset activity.

Economic Context Shapes Turkey Crypto Tax Policy

The policy initiative arises in a broader economic context defined by high involvement in digital assets. During periods of currency volatility, households are more inclined to use cryptocurrencies. Policymakers identified a way to increase financial activity outside the formal tax system. This structural gap is addressed by establishing a dedicated crypto tax system.

Market participants are preparing operational adjustments ahead of potential implementation. Investors may strengthen record-keeping and reporting procedures for realized gains. Compliance obligations could introduce short-term administrative complexity. However, defined rules provide measurable expectations for market actors.

Additionally, the plan incorporates full exemption of value-added tax on the transfer of crypto assets. This clause prevents any double taxation of digital transactions. VAT exclusion by lawmakers brings the crypto treatment in line with financial instruments. The plan supports procedural clarity in the proposed crypto tax structure.

The country’s initiative also reflects a wider international regulatory trend. Digital asset taxing systems have been implemented in jurisdictions in Europe, North America, and Asia. The new crypto bill will position the country within this global regulatory convergence.

The post Turkey Advances Crypto Tax Plans in New Era of Fiscal Oversight: Details appeared first on The Market Periodical.

You May Also Like

The changing face of elder care in Malaysia — Sayed Mohammad Reza Yamani Sayed Umar

Not a loophole: Singapore AI export controls let China tap US AI legally

Exclusive interview with Smokey The Bera, co-founder of Berachain: How the innovative PoL public chain solves the liquidity problem and may be launched in a few months