Huobi Growth Academy: Cycles are losing their effectiveness; the new paradigm for the crypto market in 2026 is "Structure is King".

Author: Huobi Growth Academy

summary

Entering 2026, the crypto market is undergoing a profound structural transformation. The long-established and repeatedly validated "four-year bull-bear cycle" is losing its explanatory power for the market, replaced by a structural evolution process characterized by the parallel development of multiple asset logics, the differentiation of capital behavior, and a slower price pace. The market no longer rises and falls in unison around a single narrative, but rather different types of assets are priced independently in their respective phases. The cycle, once the core variable determining direction, has degenerated into a background factor influencing the pace.

I. Cycles are breaking down: Why we should no longer use "bull and bear" to understand the crypto market in 2026

For a considerable period, the crypto market was almost entirely dominated by the single narrative of a "four-year bull-bear cycle." Halving timing, liquidity inflection points, sentiment bubbles, and price collapses were repeatedly validated as effective analytical tools, shaping the cognitive habits of a generation of market participants. However, as the market entered 2025, this once highly effective cyclical model began to show a systematic decline in explanatory power: market movements no longer exhibited sentiment polarization at key junctures, pullbacks were no longer accompanied by widespread liquidity collapses, and so-called "bull market start signals" frequently failed to materialize. Instead, price movements increasingly exhibited a coexistence of range-bound trading, structural differentiation, and slow upward movement. This is not because the market has "become boring," but rather because its operating mechanism is undergoing profound changes.

The essence of cyclical models relies on highly homogeneous capital behavior: similar risk appetite, similar holding periods, and high sensitivity to price itself. However, the crypto market around 2026 is gradually moving away from this premise. With the opening of compliance channels, the maturation of institutional custody and auditing systems, and the inclusion of crypto assets in a broader asset allocation discussion framework, the marginal pricing forces in the market have changed. More and more funds are entering the market not with "market timing" as their core objective, but with long-term allocation, risk hedging, or functional use as their starting point. These funds do not chase extreme volatility; instead, they absorb liquidity during downturns and reduce turnover during upturns. Their very existence weakens the emotional feedback loop upon which traditional bull and bear cycles rely.

More importantly, the increasing complexity of the crypto market's internal structure is undermining the cyclical assumption of "all rising and falling in tandem." The logical differences between Bitcoin, stablecoins, RWA, public chain assets, and application tokens are widening, and their respective sources of funding, use cases, and value anchoring methods can no longer be covered by a single cyclical language. As Bitcoin increasingly resembles a medium- to long-term value store, stablecoins become the infrastructure for cross-border settlements and on-chain finance, and some application assets begin to be priced based on cash flow and real demand, the so-called "bull market" or "bear market" itself loses its meaning as a unified descriptive framework.

Therefore, a more reasonable way to understand the crypto market in 2026 is not "whether the next bull market has begun," but rather "whether the structural stages of different assets have changed." Cycles haven't disappeared, but they are degenerating from a core variable determining direction to a background factor influencing pace. The market no longer resonates rapidly around a single central narrative, but evolves slowly under multiple parallel logics. This means that future risks will no longer be concentrated on a single top collapse, but will be more reflected in structural mismatches and cognitive lags; similarly, opportunities will no longer come from betting on the overall market trend, but from the early identification of long-term trends and role differentiation.

From this perspective, the "failure" of the cycle is not the price of the crypto market maturing, but rather a sign that it is beginning to shed its early speculative nature and move towards a systemic asset stage. The crypto market in 2026 will no longer need to be defined by bull and bear markets, but rather by its structure, function, and time to understand its true operating state.

II. Bitcoin's Transformation: From Highly Volatile Asset to Structured Reserve Instrument

If the cyclical logic is failing, then Bitcoin's own changing role is the most direct and explanatory manifestation of this change. For a long time, Bitcoin has been considered the most volatile asset in the crypto market, with its price fluctuations driven more by sentiment, liquidity, and narratives than by stable usage demand or asset-liability structure. However, since 2025, this perception has been gradually revised: Bitcoin's price volatility has continued to decline, its retracement structure has become smoother, the stability of key support levels has significantly increased, and the market's sensitivity to short-term fluctuations is decreasing. This is not a waning of speculative enthusiasm, but rather Bitcoin is being reintegrated into a pricing framework that is more inclined towards a "reserve asset."

The core of this shift lies not in whether Bitcoin is "more expensive," but in "who holds it and for what purpose." As Bitcoin is increasingly incorporated into the balance sheets of listed companies, long-term capital portfolios, and asset allocation discussions among some sovereign or quasi-sovereign entities, its holding logic has shifted from betting on price elasticity to hedging against macroeconomic uncertainty, diversifying fiat currency risk, and acquiring exposure to non-sovereign assets. Unlike the early retail-dominated market, these holders have a higher tolerance for price pullbacks and greater patience, their behavior itself compressing the circulating supply of Bitcoin and reducing the overall market's selling pressure elasticity.

At the same time, Bitcoin's financialization path is undergoing structural changes. Spot ETFs, compliant custody, and a mature derivatives system have, for the first time, provided the infrastructure for Bitcoin to be integrated into the traditional financial system on a large scale. This does not mean that Bitcoin has been completely "domesticated," but rather that its risks are being repriced: price discovery no longer occurs entirely in the most emotionally extreme on-chain or offshore markets, but is gradually shifting to a deeper and more constrained trading environment. In this process, Bitcoin's volatility has not disappeared, but has transformed from disorderly, violent fluctuations into structural fluctuations centered around macroeconomic variables and the rhythm of capital flows.

More importantly, Bitcoin's "reserve asset" does not stem from any external credit backing, but rather from the repeated verification of its supply mechanism, immutability, and decentralized consensus over a long period. Against the backdrop of continuously expanding global debt and increasing fragmentation of geopolitical and financial systems, market demand for "neutral assets" is rising. Bitcoin does not need to assume the traditional functions of currency, yet at the asset level, it is gradually becoming a value carrier that requires no counterparty credit, no policy commitment, and can be transferred across systems. This attribute makes its position in asset allocation closer to a structural reserve tool, rather than a purely high-risk speculative target.

Therefore, in 2026, Bitcoin's value should no longer be measured by how quickly it rises, but rather within a longer-term perspective of allocation and game theory. Its core significance lies not in replacing any existing asset, but in providing a new, decentralized reserve option for the global asset system. It is in this shift in role that Bitcoin's influence on the crypto market has also changed: it is no longer merely an engine of price movements, but is becoming an anchor for the stability of the entire system. As this transformation continues to deepen, Bitcoin's very existence may be more important to the crypto market in 2026 and beyond than its short-term price performance.

III. Stablecoins and RWA: The First Time the Crypto Market Truly Connected to the Real-World Financial Structure

If Bitcoin achieved "self-identification" of assets in the crypto market, then the rise of stablecoins and RWA marks the first time the crypto market has systematically integrated into the real-world financial structure. Unlike past growth driven by narratives, leverage, or token incentives, the core of this shift lies not in emotional expansion, but in the continuous entry of real assets, real cash flows, and real settlement needs into the on-chain system. This propels the crypto market from a relatively closed, self-circulating system to an open structure deeply coupled with real-world finance.

The role of stablecoins extends far beyond that of a "medium of exchange" or a "hedging tool." As their scale expands and their use cases continue to spill over, stablecoins have effectively become an "on-chain mapping" of the global dollar system: with lower settlement costs, higher programmability, and cross-regional accessibility, they undertake functions such as cross-border payments, on-chain clearing, fund management, and liquidity allocation. Especially in emerging markets, foreign trade settlements, and high-frequency cross-border capital flows, stablecoins do not replace the existing financial system but rather fill its structural gaps in efficiency and accessibility. This demand is not dependent on bull and bear cycles but is highly correlated with global trade, capital flows, and upgrades to financial infrastructure; its stability and stickiness far exceed the demands of traditional crypto transactions. Building upon stablecoins, the emergence of RWA further alters the asset composition logic of the crypto market. By mapping real-world assets such as US Treasury bonds, money market instruments, accounts receivable, and precious metals to on-chain tokens, RWA effectively introduces a long-missing element to the crypto market—a sustainable source of returns linked to the real economy. This means that for the first time, the crypto market no longer relies solely on "price increases" to support asset value. Instead, it can build a value anchor closer to traditional finance through interest, rent, or operating cash flow. This change not only improves the transparency of asset pricing but also allows on-chain funds to be reallocated around "risk-return" rather than a single narrative.

A deeper shift lies in the fact that stablecoins and RWA are reshaping the financial division of labor in the crypto market. Stablecoins provide the underlying settlement and liquidity foundation, while RWA offers exposure to real-world assets that can be split, combined, and reused. Smart contracts, on the other hand, are responsible for automated execution and risk control. Within this framework, the crypto market is no longer merely a "shadow market" of traditional finance, but is beginning to possess the capacity to independently undertake financial activities. This capacity is not formed overnight, but rather through a slow but continuous accumulation as compliance, custody, auditing, and technical standards are gradually improved. Therefore, stablecoins and RWA in 2026 should not be simply understood as a "new track" or "thematic investment," but rather as a key milestone in the structural upgrade of the crypto market. They enable the crypto system to, for the first time, have the possibility of long-term coexistence and mutual penetration with real-world finance, and also cause the growth logic of the crypto market to gradually shift from cycle-driven to demand-driven, and from closed competition to open collaboration. In this process, what truly matters is not the short-term performance of individual projects, but that the crypto market is forming a new form of financial infrastructure, the impact of which will far exceed the price level, profoundly changing the way global finance operates over the next decade.

IV. From Narrative-Driven to Efficiency-Driven: Collective Repricing at the Application Layer

After several cycles of narrative rotation, the application layer of the crypto market is entering a critical inflection point: valuation systems driven solely by grand visions, technological labels, or emotional consensus are systematically failing. The temporary decline of DeFi, NFTs, GameFi, and even some AI narratives does not mean that these directions themselves have no value, but rather that the market's tolerance for "premiums based on future imagination" has significantly decreased. Around 2026, the application layer is transitioning from a pricing system centered on stories to a new pricing logic centered on efficiency, sustainability, and real-world usage intensity.

The essence of this shift lies in the changing structure of participants in the crypto market. With the increased proportion of institutional funding, industrial capital, and hedge funds, the market is no longer solely focused on "whether a sufficiently grand story can be told," but rather on "whether it truly solves a real-world problem, possesses cost or efficiency advantages, and can operate sustainably without subsidies." Under this scrutiny, many previously overvalued applications are being repriced, while a few protocols with advantages in efficiency, user experience, and cost structure are receiving more stable capital support.

The core manifestation of efficiency-driven growth is that the application layer is beginning to compete around "output per unit of capital" and "contribution per unit of user." Whether it's decentralized trading, lending, payments, or basic middleware, the market's focus is shifting from broad metrics like TVL and number of registered users to transaction depth, retention rate, fee revenue, and capital turnover efficiency. This means that applications are no longer just "narrative decorations" for the underlying public blockchain ecosystem, but have become independent economic entities that need to generate their own revenue and have clear business logic. For applications that cannot generate positive cash flow or heavily rely on incentive subsidies, the weight of "future expectations" in their valuations is being rapidly compressed.

Meanwhile, technological advancements are amplifying efficiency differences and accelerating the differentiation of application layers. The maturity of account abstraction, modular architecture, cross-chain communication, and high-performance Layer 2 makes user experience and development costs quantifiable and comparable metrics. In this context, the migration costs for users and developers continue to decline, and applications no longer possess "natural moats." Only products that demonstrate significant advantages in performance, cost, or user experience can retain traffic and funding. This competitive environment is inherently unfavorable to projects that "maintain a premium through narrative," but it provides long-term survival space for truly efficient infrastructure and applications.

More importantly, application-layer repricing does not occur in isolation, but resonates with stablecoins, RWA, and the changing role of Bitcoin. As on-chain activities begin to support more real-world economic activity, the value of applications no longer stems from "circular games within crypto," but from their ability to efficiently handle real cash flows and real demand. This has led to applications serving payments, settlements, asset management, risk hedging, and data coordination gradually replacing purely speculative applications and becoming the core focus of the market. This change does not mean the complete disappearance of market risk appetite, but rather a shift in the way risk premiums are distributed, moving from narrative diffusion to efficiency realization.

Therefore, the application layer's "collective repricing" in 2026 is not a short-term style shift, but a structural revaluation. It signifies that the crypto market is gradually moving away from its heavy reliance on sentiment and narratives, shifting towards efficiency, sustainability, and real-world fit as core evaluation criteria. In this process, the application layer will no longer be the most volatile part of the cycle, but may become a key bridge connecting the crypto market and the real economy, with its long-term value depending more on its genuine integration into the global digital economy's operating system.

V. Conclusion: 2026 is not the starting point of a new bull market, but rather the starting point of the next decade.

If we still try to understand the crypto market in 2026 by asking "when will the next bull market come?", we are essentially standing within an outdated analytical framework. The more significant meaning of 2026 lies not in whether prices will reach new highs, but in the fact that the crypto market has completed a fundamental shift in cognition and structure: it is beginning to move from a peripheral market that heavily relies on cyclical narratives, sentiment diffusion, and liquidity games to a long-term infrastructure system embedded in the real financial system, serving real economic needs, and gradually forming an institutionalized operating logic.

This shift is first and foremost reflected in the change in market objectives. For the past decade, the core issue for the crypto market has been "how to justify its existence." However, after 2026, this issue is being replaced by "how to operate more efficiently, how to integrate with real-world systems, and how to support larger-scale funds and users." Bitcoin is no longer just a highly volatile risk asset but is beginning to be incorporated into structural reserves and macroeconomic allocation frameworks; stablecoins are evolving from a medium of exchange into key outlets for digital dollars and digital liquidity; and RWA, for the first time, truly connects the crypto system to global debt, commodity, and settlement networks. These changes will not bring about dramatic price surges in the short term, but they will determine the boundaries and ceiling of the crypto market over the next decade.

More importantly, 2026 marks the completion, not the beginning, of a paradigm shift. From cyclical games to structural games, from narrative pricing to efficiency pricing, from closed crypto internal loops to deep integration with the real economy, the crypto market is forming a new value assessment system. In this system, whether an asset possesses long-term allocation value, whether a protocol can continuously generate cash flow, and whether applications truly improve financial and collaborative efficiency are becoming more important than "how attractive the narrative is." This means that future growth will be more differentiated, slower, and more path-dependent, but it also means that the probability of systemic collapse is decreasing.

From a historical perspective, what truly determines the fate of an asset class is never the height of a single bull market, but rather whether it successfully transforms from a speculative asset into infrastructure. The crypto market in 2026 is at such a critical turning point. Prices will still fluctuate, and narratives will still change, but the underlying structure has changed: crypto is no longer just a "replacement fantasy" of traditional finance, but is becoming an extension, supplement, and even reconstruction of it. This transformation determines that the crypto market over the next decade will resemble a slow but continuously expanding main trend, rather than a series of emotionally driven, pulse-like rallies.

Therefore, rather than asking whether 2026 marks the start of a new bull market, it's more accurate to acknowledge it as a "coming-of-age ceremony"—the crypto market, for the first time, redefines its role, boundaries, and mission in a way that more closely resembles the real financial system. The real opportunities may no longer belong to those best at chasing cycles, but to those who can understand structural changes, adapt to the new paradigm in advance, and grow alongside this system in the long run.

You May Also Like

South Korean Gaming Company NXC Decides to Reduce Its Crypto Holdings! Here Are the Details

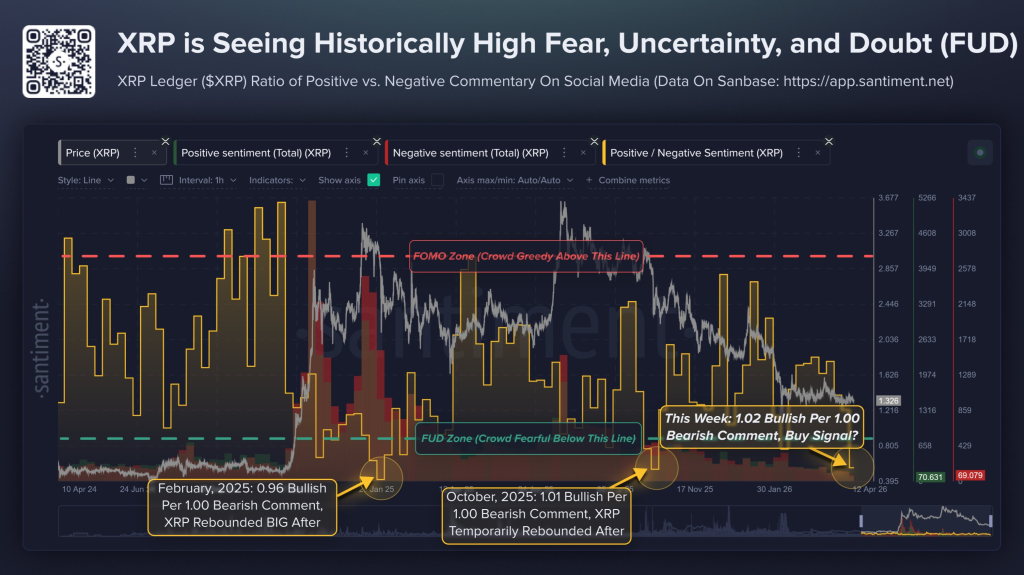

XRP Sentiment Just Flashed a Rare Contrarian Signal – Here’s What Happened the Last Two Times