CoinCircuit, which launched in December 2025, is a Nigerian startup building payment infrastructure that allows businesses and individuals to accept crypto paymentsCoinCircuit, which launched in December 2025, is a Nigerian startup building payment infrastructure that allows businesses and individuals to accept crypto payments

For businesses tired of saying no to crypto payments, CoinCircuit has an answer

For feedback or concerns regarding this content, please contact us at crypto.news@mexc.com

Chidubem Ogbuefi, the Chief Executive Officer (CEO) and founder of CoinCircuit, a Nigerian crypto payments startup, carries more money in crypto than he does in cash.

For him, paying with digital assets is often simpler than converting to naira, waiting on bank transfers, or dealing with point-of-sale (PoS) withdrawals.

Yet, that ‘crypto convenience’ does not translate to real-world use cases.

In Lagos stores, restaurants, and retail outlets, the answer is usually the same when he asks to pay with crypto: no. It frustrated him.

“That friction is what pushed me to build CoinCircuit,” said Ogbuefi. “Not because people don’t have crypto, but because businesses don’t want to deal with it.”

CoinCircuit, which launched in December 2025, is a Nigerian startup building payment infrastructure that allows businesses and individuals to accept crypto payments without becoming crypto businesses themselves.

The product sits between customers who want to pay with digital assets and merchants who would rather receive naira or stablecoins without worrying about wallets, volatility, or compliance.

Ogbuefi describes it as a Paystack-esque product if the Nigerian payments giant focused entirely on digital assets. Paystack enables businesses to accept payments from customers in different local currencies.

Get The Best African Tech Newsletters In Your Inbox

Select your country Nigeria Ghana Kenya South Africa Egypt Morocco Tunisia Algeria Libya Sudan Ethiopia Somalia Djibouti Eritrea Uganda Tanzania Rwanda Burundi Democratic Republic of the Congo Republic of the Congo Central African Republic Chad Cameroon Gabon Equatorial Guinea São Tomé and Príncipe Angola Zambia Zimbabwe Botswana Namibia Lesotho Eswatini Mozambique Madagascar Mauritius Seychelles Comoros Cape Verde Guinea-Bissau Senegal The Gambia Guinea Sierra Leone Liberia Côte d'Ivoire Burkina Faso Mali Niger Benin Togo Other

Select your gender Male Female Others

Subscribe

Carrying crypto, living in fiat

Ogbuefi’s habit of spending crypto is unusual in Nigeria, where fiat naira still dominates daily transactions.

He does not dispute that reality. What he argues is that the way crypto is used in Nigeria is often misunderstood.

A large volume of crypto activity already exists, but it rarely shows up at supermarket tills or restaurant counters.

Payments happen privately, peer-to-peer, or outside formal merchant environments. When customers want to spend crypto in public spaces, the infrastructure is missing.

“A lot of times, people walk into stores and ask if they can pay with crypto,” said Ogbuefi. “When the answer is no, they just leave. I do that too.”

The problem, from his perspective, is not demand. It is design.

Most existing crypto payment tools either exclude Nigeria altogether or assume merchants want to custody digital assets themselves. Global platforms like CoinPayments or Binance Pay often do not support African countries, or they restrict local currency invoicing.

“You can’t generate invoices in naira or Ghanaian cedis,” he said. “So I wanted to solve everything in one product.”

How CoinCircuit works, without forcing merchants into crypto

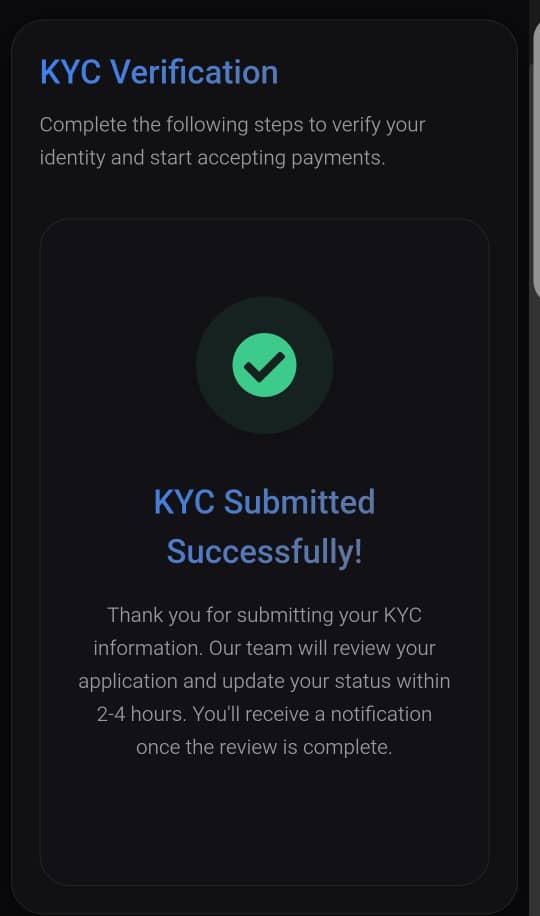

CoinCircuit’s design begins with a compliance-first approach.

Once onboarded, users identify themselves either as individuals—such as solopreneurs, freelancers, or content creators—or as registered merchants and businesses.

Business users are required to submit Corporate Affairs Commission (CAC) documents or equivalent regulatory filings. Individuals submit personal identification. All users complete know-your-customer (KYC) checks to allow transaction monitoring.

Once approved, users connect two things: a local fiat bank account and, optionally, a crypto wallet. Then CoinCircuit becomes a layer that sits between customers and merchants, translating one payment preference into another.

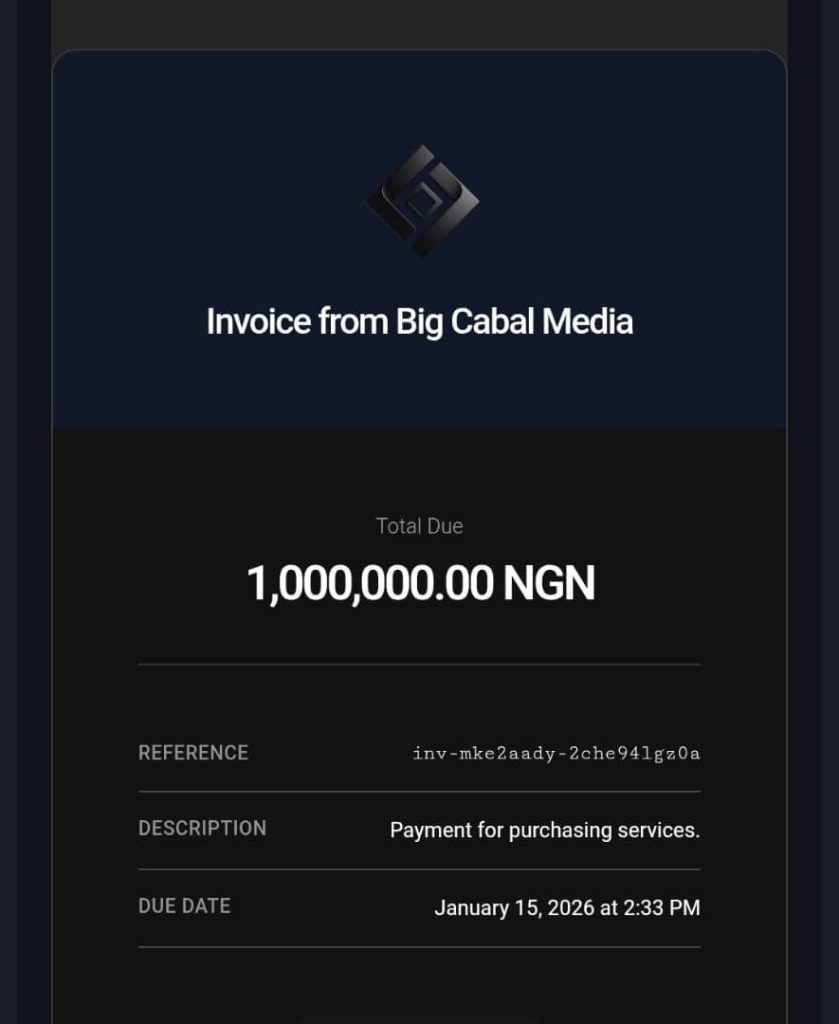

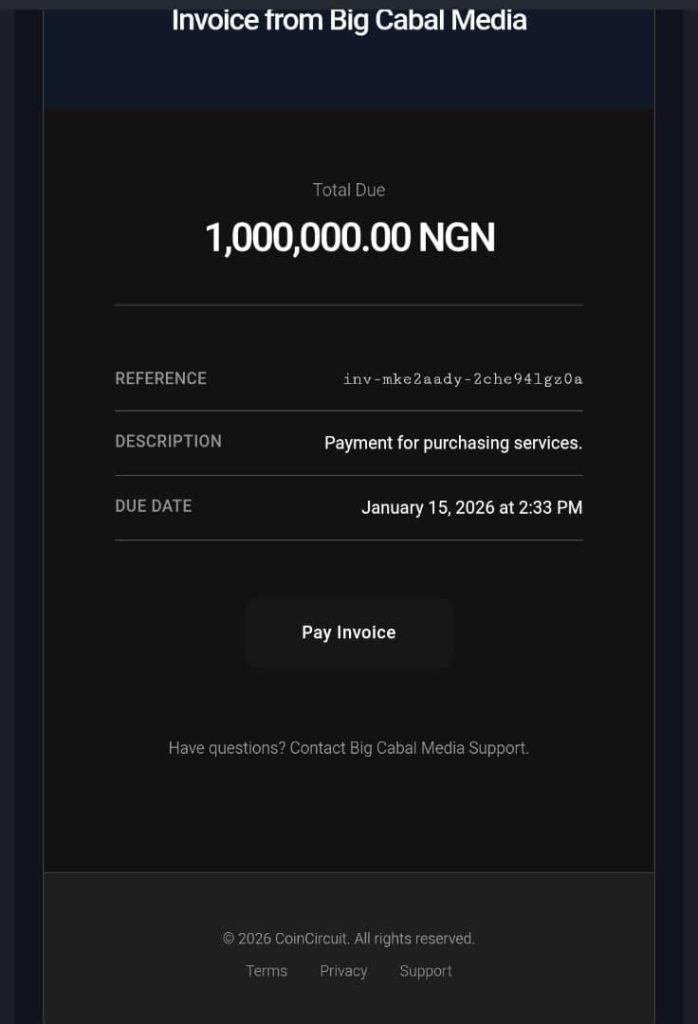

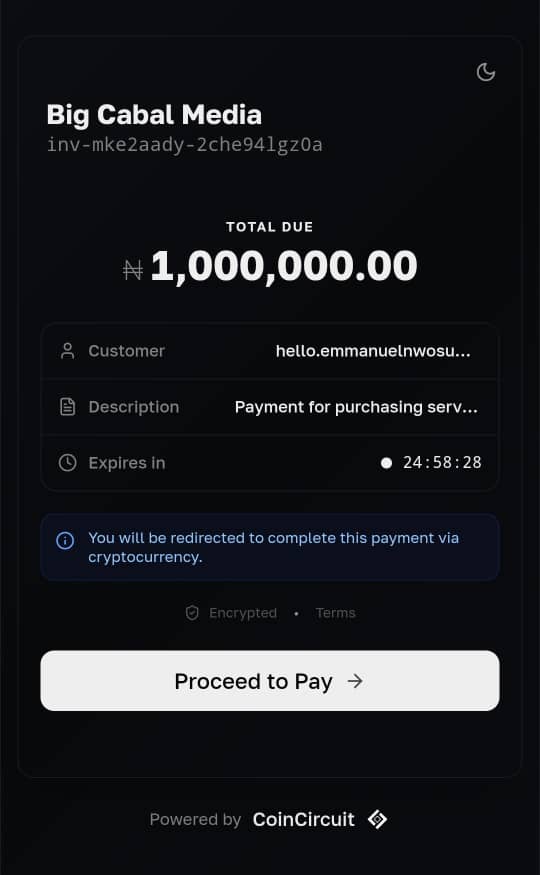

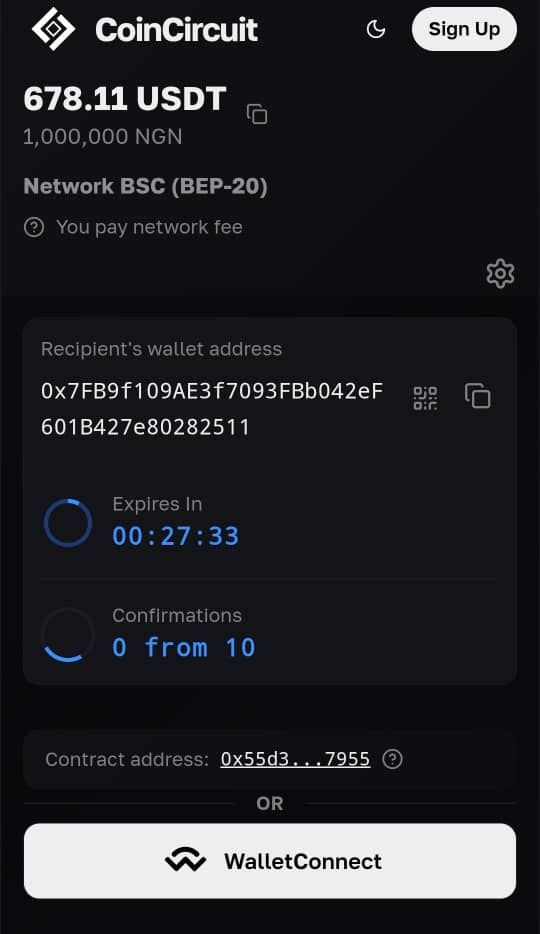

A merchant can create a payment page for use in-store or online. The page is branded with the business name and logo and can be accessed through a link or a printed Quick Response (QR) code. When customers scan the code, they are taken to a checkout page where they enter the amount they want to pay.

What matters is how the amount is quoted. A merchant can choose to quote prices in naira or in United States dollars. If the page is set to naira, the customer sees naira. If it is set to dollars, the customer sees dollars. CoinCircuit handles everything else.

Working with service providers, the startup enables settlement to happen in real-time. If a customer pays using crypto or stablecoins, the merchant can receive naira directly into a bank account or receive stablecoins like Tether (USDT) in a wallet, depending on their preference.

“The logic behind this is that you’re quoting your customers in a currency they understand, while you receive a currency you understand,” said Ogbuefi. “We will be adding more currencies like Ghanaian cedis, Kenyan shillings, and South African rand, to help merchants expand their payment collection to a wider market.”

Beyond local and foreign currency settlement, CoinCircuit supports payments in a range of cryptocurrencies and stablecoins, including Ether (ETH), Solana (SOL), TRON (TRX), Binance Coin (BNB), USD Coin (USDC), and Tether (USDT).

CoinCircuit merchants and even creators can create invoices and send to customers, who can choose to pay in crypto or fiat currencies. Image Source: TechCabal.

These payments run across multiple blockchain networks, including Ethereum, Binance Chain, Solana, and TRON, with transaction fees typically below $1.

Ogbuefi said the startup plans to expand support for additional crypto assets and networks over time, as it adapts the product to the payment preferences of different markets.

This flexibility of the product swings for both sides: Crypto-native merchants who prefer to hold digital assets can quote customers in naira or dollars and still receive cryptocurrencies or stablecoins.

Merchants can accept payments from crypto-paying customers and receive only local currency.

CoinCircuit does not hold customer funds, according to Ogbuefi. When a payment is made, the crypto asset is automatically swapped through a crypto financial service provider that supplies liquidity and regulatory cover. The service provider earns money from exchange spreads, while CoinCircuit charges a 1% take rate from customer transactions.

For example, when a customer completes a $10 transaction, CoinCircuit charges $0.1 in fees.

Ogbuefi said the structure allows CoinCircuit to operate without touching deposits while still offering immediate settlement, a feature he considers essential for trust.

“Business owners should not wait to get their money,” he said. “Once your customer pays with crypto, you get your money instantly.”

This immediacy matters in a market where delays and failed payouts play a big role in scepticism and mistrust from customers.

Get The Best African Tech Newsletters In Your Inbox

Select your country Nigeria Ghana Kenya South Africa Egypt Morocco Tunisia Algeria Libya Sudan Ethiopia Somalia Djibouti Eritrea Uganda Tanzania Rwanda Burundi Democratic Republic of the Congo Republic of the Congo Central African Republic Chad Cameroon Gabon Equatorial Guinea São Tomé and Príncipe Angola Zambia Zimbabwe Botswana Namibia Lesotho Eswatini Mozambique Madagascar Mauritius Seychelles Comoros Cape Verde Guinea-Bissau Senegal The Gambia Guinea Sierra Leone Liberia Côte d'Ivoire Burkina Faso Mali Niger Benin Togo Other

Select your gender Male Female Others

Subscribe

Built lean, built early

CoinCircuit began in 2025 with $2,000 from the founder’s personal savings. Ogbuefi, who began his tech journey as a software and blockchain engineer, leads the company as the sole founder and technical CEO; the startup runs a lean team of five, including engineers and a sole marketer.

Chidubem Ogbuefi, CoinCircuit CEO and founder. Image Source: CoinCircuit.

CoinCircuit’s operating costs remain low, said Ogbuefi, hovering between $100–$200 per month. Still in its early days, Ogbuefi says he currently builds the product out of pocket and isn’t earning from the business yet.

Under the hood, CoinCircuit runs on an event-driven architecture designed to handle multiple currencies and blockchains simultaneously. Temporary payment addresses are generated for each transaction and expire after use, mirroring how traditional payment sessions time out.

It also operates an agentic chatbot, CoinCircuit AI, embedded in the merchant dashboard. Merchants can ask questions about transaction volume, customer behaviour, or business performance, and receive responses about their business health.

“We built the AI agent using ChatGPT,” said Ogbuefi. “We didn’t have to build a model of our own. We built a list of tools and gave [ChatGPT] access to everything it could use to train the model, including access to web search functions. Outside of the development cost, it doesn’t cost us anything [to run CoinCircuit], because you’re simply giving capabilities to an existing model to access your tools and workflow.”

The approach reflects the company’s broader philosophy: build narrowly, avoid unnecessary infrastructure, and spend only where it directly improves the product.

“I didn’t want to keep crypto”

Since its launch, CoinCircuit says it has processed over ₦12 million ($8,500) in transactions, driven largely by retail businesses, clothing brands, restaurants, hotels, fast-food outlets, and clearing-and-forwarding businesses.

Most were onboarded through Ogbuefi’s personal connections and other merchants he pitched to, and convinced to adopt the product.

Henry Paris, creative director at Vanityiisland Atelier, a Lagos-based streetwear brand, was one of them. For Paris, CoinCircuit solved a problem he had been avoiding. Customers—mostly young men—kept asking to pay with crypto. He kept saying no.

“I don’t do crypto,” Paris said. “At that point, I didn’t want to keep crypto or worry about selling it.”

After speaking with Ogbuefi, Paris agreed to try CoinCircuit. The setup took minutes. He printed the QR code and placed it in his store.

“Every time they pay with crypto, it drops in my bank account in naira,” he said. “That was what amazed me.”

Paris now uses CoinCircuit regularly for in-store payments. Customers scan the QR code, pay in crypto or stablecoins, and receive naira directly to their local bank account. The system removes the need to manage wallets, price volatility, or go through crypto exchanges to convert crypto back to naira.

Aside from convenience, an unexpected benefit of using CoinCircuit, according to Paris, has been pricing.

“When people pay with crypto, I usually get slightly more than the retail price,” Paris said, pointing to FX spreads when customers convert naira prices into dollar-pegged stablecoins like USDT. “I don’t even pay attention to charges because I always get more.”

Yet, Paris is clear-eyed about CoinCircuit’s role for merchants. While it solves a fringe problem, he says that merchants who operate informal businesses may still struggle to see its real benefit.

“I wouldn’t say it’s mission-critical,” he said. “My business ran on cash, transfers, and PoS before. But it’s nice to have, especially for crypto natives who want to pay, and for merchants who don’t want the stress.”

A product like CoinCircuit, if it achieves scale, can ease crypto spending for natives who prefer to carry digital assets around. It also gives non-knowledgeable business owners and mid-sized corporations a way to tap into a younger, crypto-using demographic, without exposing themselves to crypto-related risks.

Building with bigger incumbents around

Few crypto payment gateways already exist in Nigeria. Ogbuefi said he tried those products and found them lacking in two areas: product value and usability.

“They weren’t giving me what I wanted,” he said. “I wanted something simple that people who don’t understand crypto can set up themselves.”

This focus influences how Ogbuefi and his small team build CoinCircuit: to hide the UX complexities of using crypto and make it simple and intuitive enough for less-sophisticated business owners to get started.

Ogbuefi is also acutely aware of the threats to his business that exist. Several Nigerian fintechs operate fiat payment gateways, such as Paystack. Paystack is owned by Stripe, a global payments company that reintroduced stablecoin payments in 2024. By association, the co-founder theorised that it wouldn’t be out of place for the payments giant to touch digital currencies.

When asked whether Paystack—or Stripe by extension—could eventually threaten CoinCircuit by enabling crypto settlements, Ogbuefi stays pragmatic. CoinCircuit’s primary market is Nigeria, where at least 25 million people use or hold crypto.

“It’s a very low probability because of the regulator [the Central Bank of Nigeria],” he said. “But even if they [Paystack] did, CoinCircuit would still have a business. We’re crypto-focused, and there are things we do that wouldn’t make sense for a generalist.”

CoinCircuit is not trying to replace fiat payments or convert merchants into crypto believers. It is simply adding another rail, so that when customers ask to pay with crypto, merchants no longer have to say no.

Disclaimer: The articles reposted on this site are sourced from public platforms and are provided for informational purposes only. They do not necessarily reflect the views of MEXC. All rights remain with the original authors. If you believe any content infringes on third-party rights, please contact crypto.news@mexc.com for removal. MEXC makes no guarantees regarding the accuracy, completeness, or timeliness of the content and is not responsible for any actions taken based on the information provided. The content does not constitute financial, legal, or other professional advice, nor should it be considered a recommendation or endorsement by MEXC.

Chidubem Ogbuefi, CoinCircuit CEO and founder. Image Source: CoinCircuit.

Chidubem Ogbuefi, CoinCircuit CEO and founder. Image Source: CoinCircuit.