Moderna (MRNA) Stock: Bernstein Holds Market Perform Rating After Earnings

TLDR

- Moderna posted Q3 revenue of $1.02 billion, beating estimates but down year-over-year, with a $200 million net loss and reduced 2025 guidance.

- The biotech firm ended its CMV vaccine program after efficacy issues, marking a pipeline setback for post-COVID diversification plans.

- Cost cuts in COGS and R&D came in below forecasts, helping Moderna beat EPS estimates at -$0.51 versus expected -$2.05.

- COVID-19 vaccine market share stabilized at 40%, but vaccination rates keep falling as analysts lower revenue projections.

- Bernstein kept its Market Perform rating at $25, noting the difficult path to profitability despite improved cost management.

Moderna delivered a mixed third quarter that highlighted both progress and problems. The company beat earnings expectations while cutting its outlook for the year ahead.

The biotech reported earnings per share of -$0.51. This came in well above the -$2.05 analysts had forecast.

Moderna, Inc., MRNA

Revenue hit $1.02 billion for the quarter. That topped estimates of $909.97 million but fell from last year’s numbers.

The company posted a $200 million net loss. Management also lowered both revenue guidance and R&D expense projections for 2025.

Wall Street noticed the cost discipline. COGS and research spending both landed below consensus forecasts.

Bernstein kept its Market Perform rating and $25 price target on the stock. The firm called these cuts “critical” as Moderna works toward breakeven.

Vaccine Program Cancellation Hits Pipeline

Moderna made a tough call on its vaccine pipeline. The company pulled the plug on its cytomegalovirus vaccine program.

Efficacy data simply didn’t support moving forward. This represents a real blow to diversification efforts beyond COVID products.

The CMV vaccine had been earmarked as a key growth driver. Its cancellation removes a potential revenue source from future projections.

Other respiratory vaccines continue advancing through regulatory processes. Moderna reported progress on these submissions during the earnings call.

Community analyst estimates for fair value range wildly. Projections span from $39.15 to $175 per share across 25 analysts.

COVID Market Share Finds Floor

The company’s COVID-19 vaccine business has stabilized somewhat. Market share now sits at roughly 40%.

This plateau offers predictability after volatile swings. But overall vaccination rates keep sliding downward.

Bernstein adjusted models to reflect lower COVID and RSV vaccine expectations. The firm raised its full-year EPS forecast to -$8.30 from -$9.88.

Profitability remains elusive. Revenue is tracking toward a 56% year-over-year decline.

Cash burn continues at a rapid pace. Negative free cash flow reached $2.65 billion, though the current ratio of 3.93 provides some breathing room.

Analysts project a 41% sales drop for the current year. This reflects sustained pressure in the COVID vaccine market.

The lower R&D spending helped cushion the earnings miss. Cost management is becoming a central focus for the company.

Management’s 2028 narrative projects $3.5 billion in revenue. That requires 4.6% annual growth from current levels.

Earnings would need to swing $3.4 billion from today’s -$2.9 billion loss. Some analysts peg fair value at $40.30, implying 53% upside.

Moderna exceeded Q3 earnings forecasts through cost discipline while navigating revenue headwinds from declining vaccination rates and a major pipeline discontinuation.

The post Moderna (MRNA) Stock: Bernstein Holds Market Perform Rating After Earnings appeared first on Blockonomi.

You May Also Like

Teacher accuses MAGA superintendent of working with Libs of TikTok to destroy his career

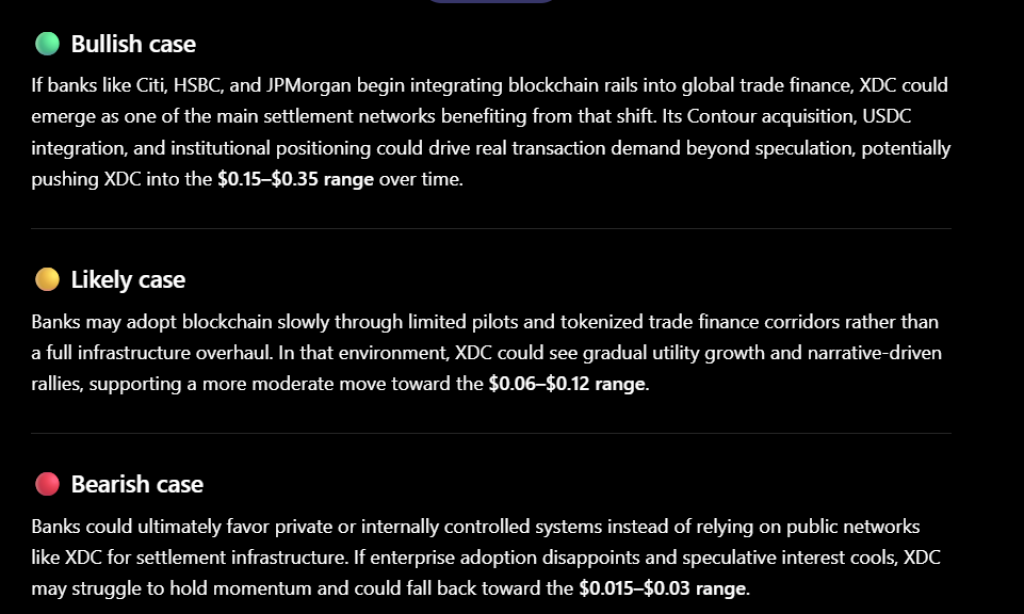

ChatGPT Predicts XDC Network Price if Banks Finally Upgrade the “Plumbing” Behind Global Trade Finance